One week into Monetary Literacy Month, the Private Finance workforce at MarketWatch has ready an abundance of articles protecting varied facets of managing cash.

It begins with this monetary literacy quiz. Likelihood is among the questions shall be straightforward for you — however you’ll in all probability be taught one thing, too, and sharing the quiz with members of the family would possibly spur helpful conversations. There’s even a bonus query!

Discover extra articles on the Monetary Health web page.

And right here’s a lesson about life and enterprise that Apple founder Steve Jobs shared with the iPhone maker’s present CEO, Tim Prepare dinner.

How you can discuss cash

Relationship issues usually spring from cash issues — or from poor communication about monetary issues, no matter wealth degree. Brian Web page, founding father of Fashionable Husbands, shares suggestions and instruments to assist {couples} talk about cash and enhance their help for one another.

Quentin Fottrell has recommendation for a person who’s nervous his sons might not make one of the best choices whereas saving up cash to purchase properties. Right here’s how he can keep their belief whereas sharing life classes about cash.

How to buy a house — and for a mortgage — in a troublesome market

For Monetary Literacy Month, TransUnion’s head of client training, Margaret Poe (left), spoke with MarketWatch’s Aarthi Swaminathan.

Barron’s Dwell

Aarthi Swaminathan interviews a house purchaser with an interesting profession, which is definitely considered one of a number of challenges he confronted in getting a mortgage. Right here’s her recommendation on easy methods to store within the present market and pay as little curiosity as doable.

And right here’s how a lot earnings you could afford a $500,000 dwelling.

On a associated word, don’t assume you recognize the whole lot about credit score reporting, particularly in case you are seeking to borrow cash to buy a house or car. Margaret Poe, who heads client training at TransUnion, shares the commonest mistake individuals make in the case of their credit score rating.

Do you need to retire early?

Getty Photos/iStockphoto

Watch out — you may not be able to retire as early as you anticipated to be, and your monetary adviser is likely to be afraid to provide the dangerous information, as Morey Stettner explains.

Extra on retirement planning:

- What’s the magic quantity for retirement financial savings? Individuals say it’s greater than $1 million, however most will fall wanting that purpose.

- One of the simplest ways to spice up retirement financial savings? Preserve it easy — and computerized.

The place will you reside whenever you retire?

Tims Ford Lake in Winchester, Tenn.

Getty Photos/iStockphoto

MarketWatch’s Retirement Software provides you the ability to make detailed customized searches for doable locations to reside.

This week, Jessica Corridor shares three doable areas to assist a reader who’s seeking to transfer to a distant location just like “a heat, sunny model of Alaska” on a low funds.

What’s going on with financial institution rates of interest?

Take a detailed have a look at the curiosity you’re incomes in your financial savings. You is likely to be leaving cash on the desk.

Getty Photos/iStockphoto

It pays to buy round. One native financial institution is paying 0.02% curiosity on financial savings accounts, whereas some massive banks are providing 3.75% or extra should you use a web based financial savings account.

Pleasure Wiltermuth explains why rates of interest on deposits haven’t been maintaining with the federal-funds charge, for which the Federal Reserve has set a goal vary of 4.75% to five%.

People who find themselves bored with being paid subsequent to nothing on their financial institution deposits have been shifting cash to money-market mutual funds. These funds have steady share costs of a greenback and pay greater rates of interest than most financial institution financial savings accounts. Joseph Adinolfi explains how this large motion of cash may damage the U.S. economic system.

There has additionally been an rising circulate of cash into exchange-traded funds that maintain bonds, as Christine Idzelis studies on this week’s ETF Wrap.

And what’s occurring with the banks?

Financial institution earnings season kicks off on April 14, when JPMorgan Chase

JPM,

Citigroup

C,

and Wells Fargo

WFC,

are scheduled to announce their first-quarter outcomes.

Right here’s a sampling of Steve Gelsi’s ongoing protection of the aftermath of the deposit flight that led to the failures of Silicon Valley Financial institution and Signature Financial institution of New York, in addition to to issues about different banks’ liquidity:

Mark Hulbert: Silicon Valley Financial institution’s failure isn’t the top of the banking disaster. Historical past says it simply is likely to be the beginning.

For bearish and bullish buyers

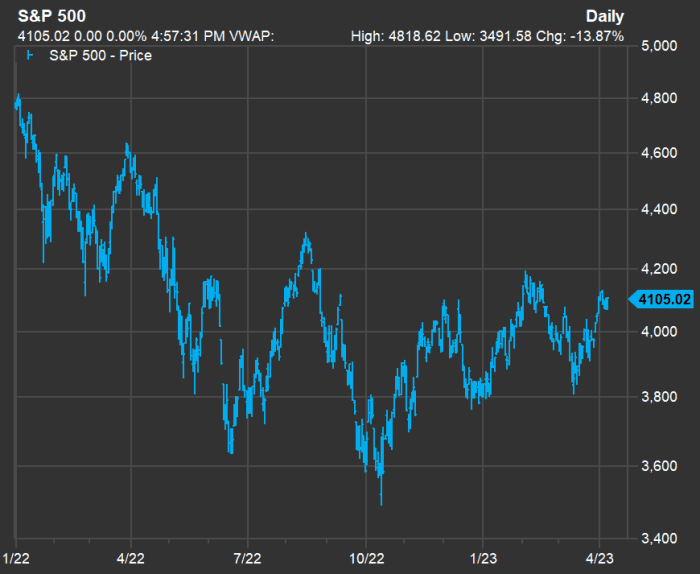

The S&P 500’s restoration from its October backside has been bumpy — and partial.

FactSet

The bear market might not be over for shares, regardless of this 12 months’s 7.4% return for the S&P 500. Listed here are 4 causes buyers could also be in for extra ache over the brief time period.

For extra of the gloomy view: A ‘credit score crunch’ is already below manner, economist warns

Then once more, one investor’s worry is one other investor’s alternative. With so {many professional} cash managers advising a low allocation to shares, analysts at Financial institution of America see clear sign that it’s time to purchase.

How about some inventory screens?

Auto gross sales warmth up — for a stunning purpose

Tesla CEO Elon Musk is likely to be the topic of a shareholder proposal within the electric-vehicle maker’s annual proxy assertion.

Getty Photos

Tesla Inc.’s

TSLA,

annual assembly will happen on Could 15. This 12 months’s proxy assertion features a shareholder proposal that is likely to be particularly fascinating for CEO Elon Musk, as Claudia Assis studies.

Associated: U.S. automotive gross sales bought assist from an surprising nook of the market

Need extra from MarketWatch? Join this and different newsletters to get the newest information, private finance and investing recommendation.