Finance

The Ascendancy Of AI In Asia’s Financial Services Industry

Synthetic intelligence has the potential to utterly revolutionize the monetary business in … [+]

The rising ubiquity of smartphones along with broader digital transformation within the enterprise world are catalyzing the adoption of synthetic intelligence (AI) within the monetary providers sector. As AI matures and turns into extra broadly built-in into enterprise operations, this pattern is about to speed up.

On the similar time, each the monetary business and regulators know that there are challenges and dangers related to AI that should be addressed.

Certainly, AI is now at an inflection level the place it’s primed to take a leap ahead. The monetary establishments which have the fitting infrastructure, tradition, and mindset that permit them to make full use of the know-how will achieve vital aggressive benefits in an more and more digitized market atmosphere.

The State of AI in Asia’s Monetary Companies Sector

There are a selection of areas the place AI is being utilized by the monetary business within the APAC area. One of the vital is customer support. AI chatbots and digital assistants can mechanically reply primary questions on checking account balances or reserving department appointments. The aim of those AI instruments thought is to reduce friction for purchasers and prices for banks.

Most banks throughout Asia have already got a model of their very own chatbot, both white-labelled or constructed in-house. Malaysian financial institution CIMB, for instance, launched the primary conversational type and real-time chatbot for business banking which was the primary in-market chatbot on the time of launch.

In the meantime, AI-powered robo-advisors more and more present customized funding recommendation to retail traders. Many conventional monetary establishments have launched robo-advisory platforms, and there has additionally been a proliferation of fintech robo-advisors throughout Asia. The latter embrace startups resembling Endowus, Syfe, Stashaway, and Robowealth. This pattern is more likely to proceed as extra traders search low-cost, digital choices.

AI-based programs may crunch huge information troves to evaluate creditworthiness and make lending selections, enhancing the effectivity of the lending course of whereas lowering default dangers. AI can seize insights from different sources of information which then makes it attainable to increase loans to people who should not have any credit score historical past. That is particularly pertinent in Southeast Asia, the place 60% of MSMEs surveyed by Tech for Good Institute in 2021 have been unable to get a mortgage once they wanted financing. UnionBank within the Philippines, for instance, has utilized AI- powered credit score scoring fashions to generate credit score scores for the unbanked via using such different information.

Moreover, AI-powered programs can detect patterns of fraudulent exercise and cash laundering that may be tough for people to identify. That is particularly vital as monetary crime continues to evolve and change into extra refined. For its half, Singapore’s DBS

DBS

Distinguishing Actuality from Hype

To a sure extent, the AI hype bubble has had a detrimental impact on the know-how’s real-world functions. AI traders, founders of AI startups and a few consultants have a vested curiosity in exaggerating the know-how’s significance for monetary causes. What number of occasions have we heard that AI is coming for our jobs? Or that it’ll save corporations mammoth sums? Or that it’ll change all the pieces?

But whereas we anticipated conversational AI to scale back reliance on name facilities, chatbots are nonetheless not capable of perform full conversations and in some instances are nonetheless state of affairs primarily based, solely capable of return a pre-determined set of replies to a restricted set of situations. If queries from clients are outdoors of the set, clients might be directed to a name/chat middle.

As well as, monetary providers are closely regulated. Corporations within the business should adjust to a variety of rules, which may make it tough to implement new applied sciences like AI. Monetary establishments should have a powerful understanding of how they use AI to make sure buyer satisfaction, optimum enterprise efficiency and regulatory compliance.

Monetary corporations ought to perceive algorithms powering AI instruments that fight cash laundering, particularly when it considerations using buyer information. There are considerations in regards to the potential moral implications of utilizing AI in monetary decision-making, resembling bias and discrimination.

Singapore has, on account of such considerations, launched the world’s first AI Governance Testing Framework and Toolkit. A.I. Confirm goals to advertise transparency and moral use of AI between corporations and their stakeholders via a mixture of technical checks and course of checks.

Regular Adoption

We are able to count on extra international locations in Asia to comply with Singapore’s lead. Monetary establishments should show the trustworthiness and transparency of AI programs to each regulators and clients. As an alternative of simply deploying AI, banks will more and more must allocate extra assets to hiring the fitting expertise to make sure buyer information is dealt with and saved correctly.

That stated, total, AI is already having a big influence on the monetary providers business, and this pattern is predicted to proceed because the know-how matures and turns into extra broadly obtainable. AI utilization in monetary providers is turning into the rule, not the exception.

The incorporation of AI in monetary providers will carry many advantages resembling price discount, improved effectivity, higher customer support and extra correct decision-making. On the similar time, the monetary business can be conscious that there are challenges and dangers related to AI, resembling information privateness, safety, job displacement, and moral considerations, that should be addressed.

Within the years forward, AI adoption in finance will steadily speed up in a variety of functions, from fraud detection and threat administration to non-public finance and monetary recommendation.

The monetary establishments that maximize AI’s potential might be those that efficiently stability enterprise advantages towards regulatory complexity and the necessity to preserve clients’ belief.

Mahindra Finance reported a total income of ₹3,706 crores, marking a 21 per cent increase year-over-year (YoY), for the quarter ending March 31, 2024, on May 4. However, the Profit After Tax (PAT) experienced a slight downturn by 10 per cent YoY, settling at ₹619 crores, attributed to a 14% increase in Net Interest Income (NII) which stood at ₹1,971 crores. The Net Interest Margin (NIM) remained fairly stable at 7.1%. The reported disbursements for the quarter saw an 11% rise, totalling ₹15,292 crores, and the Gross Loan Book grew by an impressive 24% YoY to ₹1,02,597 crores.

Also Read | Pakistan coach Gary Kirstein gets brutally trolled after meeting with team online, ‘Is this cricket or…?’

The company also showed marked improvement in asset quality, with a significant reduction in Stage 3 assets to 3.4%, down from 4.0% in December 2023. Credit costs for the year were maintained within the targeted range of 1.5% – 1.7%, indicative of effective risk management strategies.

Also Read | Justin Trudeau says ‘rule-of-law’ after 3 arrested for Nijjar killing, Jaishankar says ‘internal politics’

In its consolidated results, the company posted a total income of ₹4,333 crores for the fourth quarter, up by 23% YoY, and a marginal decrease in PAT by 1%, amounting to ₹671 crores. The consolidated disbursements also noted an increase of 11% YoY, reaching ₹16,174 crores.

Also Read | No Dunki route to London anymore: Why is Rishi Sunak deporting UK’s illegal immigrants to Rwanda? An explainer

The company’s strategic initiatives included bolstering its presence in vehicle finance, particularly in pre-owned vehicle finance, which grew by 18% during FY24. Moreover, Mahindra Finance announced plans to enhance its services in the non-vehicle finance segment, aiming to expand its Asset Under Management (AUM) to 15% over the medium term. This includes increasing investments in sectors such as Small and Medium Enterprises (SME) lending, Lease and Purchase (LAP), and leasing through its Quiklyz platform.

Unlock a world of Benefits! From insightful newsletters to real-time stock tracking, breaking news and a personalized newsfeed – it’s all here, just a click away! Login Now!

Download The Mint News App to get Daily Market Updates & Live Business News.

More

Less

Published: 05 May 2024, 09:46 AM IST

Transwarranty Finance Q4 Results Live : Transwarranty Finance declared their Q4 results on 02 May, 2024. The topline increased by 166.66% & the profit came at ₹2.73cr.

It is noteworthy that Transwarranty Finance had declared a loss of ₹6cr in the previous fiscal year in the same period.

As compared to the previous quarter, the revenue grew by 68.98%.

The Selling, general & administrative expenses rose by 12.53% q-o-q & increased by 13.69% Y-o-Y.

The operating income was up by 7726.27% q-o-q & increased by 154.53% Y-o-Y.

The EPS is ₹0.98 for Q4, which increased by 148.87% Y-o-Y.

Transwarranty Finance has delivered 0% return in the last 1 week, 24.19% return in the last 6 months, and -6.85% YTD return.

Currently, Transwarranty Finance has a market cap of ₹56.46 Cr and 52wk high/low of ₹15.5 & ₹8.25 respectively.

| Period | Q4 | Q3 | Q-o-Q Growth | Q4 | Y-o-Y Growth |

|---|---|---|---|---|---|

| Total Revenue | 5.12 | 3.03 | +68.98% | 1.92 | +166.66% |

| Selling/ General/ Admin Expenses Total | 1.16 | 1.03 | +12.53% | 1.02 | +13.69% |

| Depreciation/ Amortization | 0.13 | 0.12 | +9.2% | 0.12 | +1.13% |

| Total Operating Expense | 2.42 | 3.07 | -21% | 6.87 | -64.74% |

| Operating Income | 2.7 | -0.04 | +7726.27% | -4.95 | +154.53% |

| Net Income Before Taxes | 2.73 | -0.36 | +862.66% | -6.01 | +145.33% |

| Net Income | 2.73 | -0.36 | +863.53% | -6 | +145.44% |

| Diluted Normalized EPS | 0.98 | -0.07 | +1500% | -2.01 | +148.87% |

FAQs

Question : What is the Q4 profit/Loss as per company?

Ans : ₹2.73Cr

Question : What is Q4 revenue?

Ans : ₹5.12Cr

Stay updated on quarterly results with our results calendar

Unlock a world of Benefits! From insightful newsletters to real-time stock tracking, breaking news and a personalized newsfeed – it’s all here, just a click away! Login Now!

Download The Mint News App to get Daily Market Updates & Live Business News.

More

Less

Published: 05 May 2024, 02:36 AM IST

Finance

New Interim Finance Director Deal in the Works | South Pasadena Finance Dept. Pushing Through | The South Pasadenan | South Pasadena News

Scott Miller, a retired municipal finance official with four decades in the field, is being considered to serve as South Pasadena’s new finance director on an interim basis, the South Pasadenan News has learned.

Although an agreement has not been signed or finalized, “we are working on it,” said Luis Frausto, Acting Deputy City Manager.

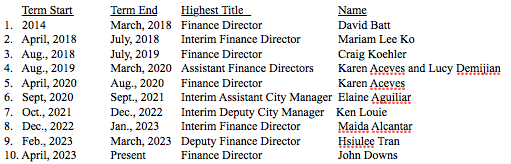

Miller would become the tenth person to manage the city’s volatile finance department since the departure of David Batt in March of 2018.

CITY OF SOUTH PASADENA FINANCE DEPARTMENT PAST DIRECTORS

The news comes shortly after the city confirmed outgoing Finance Director John Downs, who told the city last month he would retire May 2, has been persuaded to stay on “in a limited term capacity to assist with finalizing the fiscal year 2024-2025 budget,” Frausto said. Downs’ “role will transition from managing daily finance operations to focusing on specific projects, with the budget being his primary responsibility. We expect his contributions to extend at least through June.”

The city is currently scheduled to adopt the new budget June 5—a target that is looking increasingly less certain.

According to press reports, Miller was chief financial officer at the city of Beverly Hills for seven years through 2015, where he was credited with helping secure high ratings for the city from the three major credit rating agencies.

Miller then worked briefly as chief finance officer for Broward County, Florida and then with Urban Futures Inc., a local government service agency in California. In March 2016, he became interim chief financial officer for the city of Riverside, initially under a short term contract. Although he became a Riverside employee in early 2017, he left several months later. At the time, a Riverside city spokesman told a local publication he could not say if Miller’s departure from Riverside was a mutual decision.

Prior to joining Beverly Hills, Miller was employed by the city of Palm Desert, the city and county of San Francisco, the University of California–Berkeley and Turner Broadcasting System. He graduated from San Diego State University with a BA in psychology and minor in business administration and he holds a PhD in public administration from Arizona State University.

In 'The Fall Guy,' stunts finally get the spotlight

/cdn.vox-cdn.com/uploads/chorus_asset/file/25432052/installer.png)

The best new browser for Windows

Fourth body found in search for US and Australian surfers who mysteriously vanished in Mexico

Republicans believe college campus chaos works in their favor

Mystik Dan wins 150th Kentucky Derby in photo finish

See it: Tesla crashes into Columbus convention center at 70 mph

Colorado Rockies game no. 116 thread: Zac Gallen vs José Ureña

Fox News Politics: Georgia the whole day through

Death of missing Oregon girl found in stream ruled homicide

At least 2 dead as tornadoes hit Alabama, damage homes across Southeast

Republicans believe college campus chaos works in their favor

German socialist candidate attacked before EU elections

Driver dies after crashing into White House perimeter gate, Secret Service says

Conservative beer brand plans 'Frat Boy Summer' event celebrating college students who defended American flag

Spain and Argentina trade jibes in row before visit by President Milei

-

News1 week ago

News1 week agoFirst cargo ship passes through new channel since Baltimore bridge collapse

-

World1 week ago

World1 week agoHaiti Prime Minister Ariel Henry resigns, transitional council takes power

-

Movie Reviews1 week ago

Movie Reviews1 week agoAbigail Movie Review: When pirouettes turn perilous

-

World1 week ago

World1 week agoEU Parliament leaders recall term's highs and lows at last sitting

-

Politics1 week ago

Politics1 week ago911 call transcript details Democratic Minnesota state senator’s alleged burglary at stepmother's home

-

Politics1 week ago

Politics1 week agoGOP lawmakers demand major donors pull funding from Columbia over 'antisemitic incidents'

-

Science1 week ago

Science1 week agoOpinion: America's 'big glass' dominance hangs on the fate of two powerful new telescopes

-

World1 week ago

World1 week agoHamas ‘serious’ about captives’ release but not without Gaza ceasefire