Finance

Public Debt Is At An 80-Year High. How Can Finance Ministers Tame It?

Given the severity of the current debt situation, we can’t expect easy solutions or quick … [+]

By Jordi Gual (IESE Business School)

The ratio of public debt to GDP in advanced economies was 112% this year, up from 104% in 2019, before the pandemic’s toll on economic activity brought on a dramatic spike. That peacetime figure is, remarkably, among the highest since way back in 1946, in the immediate wake of World War II.

A widespread issue

What’s more, the ratio for emerging economies hit an unprecedented 69% this year. All told, global public debt tripled between the mid-1970s and 2022, when it reached 92% of GDP.

How big a problem is the current debt level, which by all accounts is high by historic standards? And which measures might economic ministers put in place to alleviate it?

While the planet has been spared a military conflict on the scale of WWII, the current debt peak came about because governments gave huge amounts of money away during a global pandemic as they essentially provided insurance for an uninsurable event. And even though most governments have ended pandemic-related fiscal supports, their responses to food and energy price hikes have made the issue persist.

All of this coincides with debts that surged after the financial crisis (due to support for the population and private debts being made public) as well as the fact that democratic governments (in profligate countries, but also in the US and UK) have a hard time controlling spending and raising taxes, resulting in a tendency to be in deficit.

The potential consequences of high indebtedness are interwoven, and depend on responses by government leaders. Broadly speaking, though, as debt service gets more and more expensive, policies to restrict it result in increased taxation. Decreased spending is another consequence of restrictive policies, and can come about alongside or independent of higher taxes.

What’s worrisome about the current scenario is the gradual, sustained increase in public debt underpinning it. This could lead to a dangerous spiral of increased debt and costs that lands the economy in a full-blown crisis.

The situation is distinct from the 2008 financial crisis, which involved private debtors. Still, certain patterns are repeating themselves. For instance, the public debt challenge in the eurozone is compounded by having a single currency and 20 treasuries. And the moral hazard remains of profligate countries in the zone piggybacking on frugal ones.

Time-tested responses

In the past, central banks often relied on growth to rein in debt. The problem is that the burden of debt makes it hard to grow through consumption. Austerity measures are another response, but as the past 15 years have proven, even well-intentioned measures to achieve budgets in primary surplus can ignite fierce citizen backlash and entire populist movements.

Financial repression is a debt-taming action, undertaken by several governments after WWII, of controlling interest rates administratively. This cannot be done nowadays in free markets, but an alternative is leaving rates alone and buying government bonds via unorthodox monetary policy, thereby reducing government funding costs. Advanced economies are unlikely to resort to the restructuring and default option that Argentine has pursued. Finally, a too-tepid response to inflation spurred in part by debt invites in a cancerous threat to economic health.

Given the severity of the current debt situation, we can’t expect easy solutions or quick improvements. I foresee that to pay back debts governments will play the following game: central banks will keep inflation around 3 or 4%, a level at which the real value of debt diminishes. The banks will maintain interest rates at just around the same levels, resulting in a real interest rate around zero.

Whittling away at today’s unsustainable debt levels will take significantly longer than anyone would like. But keeping interest rates moderately high, spending cuts and tax increases that don’t cripple consumer spending and, hopefully, a steady cooling of inflation would be reason for cautious optimism among those taking the long view.

Jordi Gual is a professor of economics at IESE Business School.

Don Cardinal of Financial Data Exchange (FDX) explores how Open Finance extends beyond Open Banking, revolutionising financial data sharing.

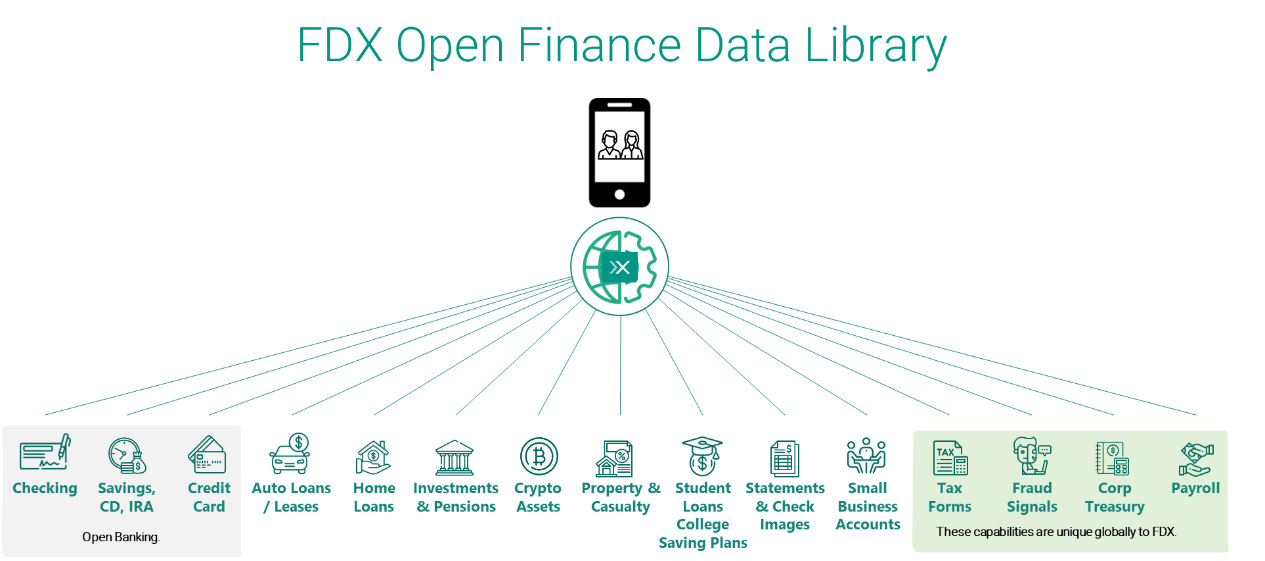

Much ink has been spilt on the topic of Open Banking, but I wanted to take a step today into a larger world of Open Finance. Whereas Open Banking is most commonly associated with current accounts (checking, savings, credit cards), Open Finance is concerned with the totality of your financial world.

While current accounts are important in the personal financial management use case, when you look at more sophisticated needs, liability accounts like auto loans, home loans, and student loans are required to help give context to a personal balance sheet. Finally, the addition of investment and retirement accounts gives the wealth management user a full 360-degree view of the consumer’s financial health.

Additional use cases – such as account and balance verification, bill payment, and payroll needs like verification of income/employment and pay stub retrieval – along with the ability to retrieve tax forms like W2, 1098, 1099, and capital gain statements for tax preparation, round out the most common consumer demands for linking accounts.

These are all important use cases for consumers and small businesses, but it is also important to address why data providers like banks, brokers, and others would benefit from data sharing.

We know that one in three digitally-enabled consumers has shared access to their financial data in the last year and similar polls of financial institutions tell us that at least one-third (if not more) of their online banking traffic was credential-based access (screen scraping) to power these use cases.

Imagine if a data provider could reduce one-third of its entire load on its online infrastructure in favour of a portal 100 times more efficient than screen scraping. The introduction of secure APIs does just that. Lowering costs of hardware overall.

One of the other uses by data providers is data-in, to pre-fill new account applications as well as provide strong signals for Know Your Customer (KYC), including account tenure at a predecessor institution. Better data means faster, more accurate decisions leading to fewer abandons or declines, meaning more revenue for the institution.

As a banker for a number of years, one of the biggest questions we had was ‘What was our share of a given customer’s wallet?’ We often had to try to infer based on monies in and out, but with Open Finance, you can link to other institutions and know in real time what your share of wallet is. This allows you to be almost surgical in your marketing and product offering.

All this is made possible by secure, permissioned data sharing via a common API standard.

Looking forward

Avoid FUD (fear, uncertainty, and doubt). Many jurisdictions have implemented Open Banking (the UK, EU, Australia, Brazil, among others) and there has yet to be a mass exodus of consumers in any of these nations. Why? If you are confident in your product, your pricing, and your service, making data available via an API does nothing to incent consumers to leave, rather the opposite. The largest credit union in Brazil said at the FDX Spring 2024 Summit that they saw a net increase in digital engagement and accounts per customer after Open Banking was introduced.

A last bit of advice: APIs are a net new channel and will be the third leg in the digital stool. Online, Mobile, and API will be the troika. APIs are much more efficient and can deliver data that cannot be displayed visually. As you make your plans for 2025 and 2026 for your digital roadmap, you would be remiss in not including Open Finance APIs in your product mix. Your competitors are.

This editorial piece was first published in The Paypers’ Open Finance Report 2024, the latest comprehensive market overview and analysis focusing on the key players and products within the Open Banking and Open Finance ecosystem. Download the full report to discover more insightful content.

About Don Cardinal

Don Cardinal is Managing Director of Financial Data Exchange (FDX) and has led it since its inception. Previously, he spent over 20 years with Bank of America, serving as head of digital for its Military Bank, VP of Digital Banking & Senior VP of Information Security. Don holds 18 US patents and CPA, CISA, CISM certificates.

Don Cardinal is Managing Director of Financial Data Exchange (FDX) and has led it since its inception. Previously, he spent over 20 years with Bank of America, serving as head of digital for its Military Bank, VP of Digital Banking & Senior VP of Information Security. Don holds 18 US patents and CPA, CISA, CISM certificates.

About FDX

![]() The Financial Data Exchange (FDX) is dedicated to unifying the financial industry around a common, interoperable, royalty-free standard for the secure and convenient access of permissioned consumer and business financial data: the FDX Application Programming Interface (FDX API). FDX is a global 501(c)(6) nonprofit organisation with no commercial interests operating in the US and Canada.

The Financial Data Exchange (FDX) is dedicated to unifying the financial industry around a common, interoperable, royalty-free standard for the secure and convenient access of permissioned consumer and business financial data: the FDX Application Programming Interface (FDX API). FDX is a global 501(c)(6) nonprofit organisation with no commercial interests operating in the US and Canada.

Boost your finances: Experts share top 2025 money resolutions

With holiday credit card bills starting to roll in, you might want to shift your New Years resolution from your waistline to your wallet.

CHICAGO – With holiday credit card bills starting to roll in, you might want to shift your New Year’s resolution from your waistline to your wallet.

In a Fox 32 money saver special report, we asked the experts for a little help on how to boost your finances in 2025.

SMART MONEY MOVES

Why you should care:

“Some of the resolutions, some of the tips we would recommend for your New Year resolutions, financially, is to plan for retirement,” said Chip Lupo, a writer and analyst at WalletHub.

Lupo said it’s critically important that you begin to build an emergency fund to avoid relying on high-interest credit cards during life’s unexpected moments.

“We’re in a situation now where, because of the inflationary economy, people are now relying on credit cards for everyday expenses when the primary objective of a credit card for most people is to have basically an emergency fund,” Lupo said.

Lupo said that wages aren’t keeping up with the rate of inflation, and people are turning to credit cards for the essentials such as food and gas, which leads to significant debt by the end of the year.

“I think a big area that lot of consumers can agree on was the rising living costs,” said consumer finance expert Andrea Woroch. “Inflation impacting how much they’re spending on housing, transportation, groceries as well as even health care.”

MAKE A GAME PLAN

What you can do:

Woroch said you need to get back to the basics – set a budget this year and follow it.

“A lot of people think of a budget as being really restrictive and while it does cap you on spending in certain areas, a budget allows you to see where you are potentially wasting money on things you don’t need,” Woroch said.

If you think setting up a budget can be overwhelming, Woroch said going into debt and having no money in savings can be even worse.

Not to mention, there are digital tools and apps to help you set a budget, like the “You Need a Budget” app, or YNAB.

“Saying you are going to pay off debt is not enough. You have to be specific with how much debt you are going to pay off and set a realistic goal,” Woroch said.

When you take on this financial resolution, Woroch said it’s important to have a plan in place. Use a balance transfer credit card or pay off the smallest balance first.

If you don’t have a plan, Woroch said you will likely just continue your cycle of debt.

Another tip from our experts, they both recommended taking advantage of the high interest rates being offered with online bank accounts or CD’s.

The Source: For this story, the Fox 32 Chicago Special Projects team spoke with leading personal finance experts Chip Lupo from WalletHub and Andrea Woroch.

A pair of voting advocacy groups founded by failed Democrat Georgia gubernatorial candidate Stacey Abrams were hit with a historic fine by the Georgia Ethics Commission for violating campaign finance laws to bolster Abram’s 2018 election.

“Today the State Ethics Commission entered into a consent agreement with the New Georgia Project and the New Georgia Project Action Fund for a total of $300,000,” the Georgia State Ethics Commission posted in a statement on Wednesday. “This certainly represents the largest fine imposed in the history of Georgia’s Ethics Commission, but it also appears to be the largest ethics fine ever imposed by any state ethics commission in the country related to an election and campaign finance case.”

Abrams founded the New Georgia Project in 2013 as part of an effort to register more minority voters and young voters. The organization was founded as a charity that can accept tax-deductible donations, while the New Georgia Project Action Fund worked as the organization’s fundraising arm.

The groups admitted to failing to disclose about $4.2 million in contributions and $3.2 million in expenditures that were used during Abram’s election efforts in 2018, according to the commission’s consent order. The groups were hit with a total of 16 violations, including failing to register as a political committee and failure to disclose millions of dollars in political contributions.

STACEY ABRAMS SAYS TRUMP RE-ELECTION WAS NOT A ‘SEISMIC SHIFT’ OR ‘LANDSLIDE’

Stacey Abrams (Elijah Nouvelage/Getty Images/File)

The groups were accused of carrying out similar activity in 2019, when they reportedly failed to disclose $646,000 in contributions and $174,000 while advocating for a ballot initiative.

STACEY ABRAMS ACCUSES CNN HOST OF ‘REPEATING DISINFORMATION’ ABOUT HER CASTING DOUBT ON 2018 ELECTION RESULTS

“This represents the largest and most significant instance of an organization illegally influencing our statewide elections in Georgia that we have ever discovered, and I believe this sends a clear message to both the public and potential bad actors moving forward that we will hold you accountable,” the ethics commission continued in its statement Wednesday.

STACEY ABRAMS PRAISED ON ‘THE VIEW’ FOR NOT CONCEDING ELECTION, DEFENDS SAYING SHE ‘WON’ GEORGIA RACE IN 2018

Abrams stepped down from the group in 2017, with Sen. Raphael Warnock taking the reins as the New Georgia Project’s CEO from 2017 to 2019, the Associated Press reported. Warnock was elected as a U.S. senator from Georgia in 2020.

Democrat Georgia Sen. Raphael Warnock, who also serves as the head pastor at Ebenezer Baptist Church in Atlanta, speaks from the pulpit. (Paras Griffin/Getty Images/File)

A spokesperson for Warnock’s Senate office told the AP that he was working “as a longtime champion for voting rights” and that he was not aware of campaign violations. The spokesperson added that “compliance decisions were not a part of that work.” Fox Digital also reached out to Warnock’s office for additional comment but did not immediately receive a reply.

Abrams ran for governor of Georgia in 2018 and 2022, but lost to Republican Gov. Brian Kemp in both races. Abrams drew national attention after the 2018 race when she refused to concede to the Republican despite losing by 60,000 votes.

STACEY ABRAMS ON NOT CONCEDING GEORGIA LOSS: WE SHOULD BE ALLOWED TO ‘LEGITIMATELY QUESTION’ SYSTEMS

Amid the 2018 race, she touted the New Georgia Project on her X account, which was called Twitter at the time.

“When Abrams sees a problem, she doesn’t wait for someone else to step up – she does it herself. So when she saw that 800,000 people of color in Georgia weren’t registered to vote, Abrams immediately set out to fix the problem & founded The New GA Project,” she tweeted.

The New Georgia Project said in a comment provided to Fox News Digital that they are “glad to finally put this matter behind us” so the group can “fully devote its time and attention to its efforts to civically engage and register black, brown, and young voters in Georgia.”

CLICK HERE TO GET THE FOX NEWS APP

“While we remain disappointed that the federal court ruling on the constitutionality of the Georgia Government Transparency and Campaign Finance Act was overturned on entirely procedural grounds, we accept this outcome and are eager to turn the page on activities that took place more than five years ago,” the group continued.

Insulin Prices Dropped. But Some Poor Patients Are Paying More.

Footballers’ shin pads – the piece of equipment some pros prefer not to wear

Neko Case Has Sung Hard Truths. Now She’s Telling Hers in a Memoir.

A Bastion of Los Angeles Hippie Culture Survived the Flames

What Happened to Enrollment at Top Colleges After Affirmative Action Ended

Colorado Rockies game no. 116 thread: Zac Gallen vs José Ureña

Why Marjorie Taylor Greene was ‘kicked out’ of the Freedom Caucus according to Rep. Buck

See it: Tesla crashes into Columbus convention center at 70 mph

Fox News Politics: Georgia the whole day through

Death of missing Oregon girl found in stream ruled homicide

ICE says it will needs massive funding hike, tens of thousands more beds to implement Laken Riley Act

Romania sets May date for new presidential election

‘Criminal, you belong to ICJ’: Antony Blinken heckled by journalists on Gaza policy during his last conference

As Governor, Burgum Promised to Manage Conflicts. They Still Cropped Up.

House Dems push Garland to drop charges, release second part of Jack Smith report

-

/cdn.vox-cdn.com/uploads/chorus_asset/file/25822586/STK169_ZUCKERBERG_MAGA_STKS491_CVIRGINIA_A.jpg "Meta is highlighting a splintering global approach to online speech") Technology1 week ago

Technology1 week agoMeta is highlighting a splintering global approach to online speech

-

Science5 days ago

Science5 days agoMetro will offer free rides in L.A. through Sunday due to fires

-

/cdn.vox-cdn.com/uploads/chorus_asset/file/25821992/videoframe_720397.png "Las Vegas police release ChatGPT logs from the suspect in the Cybertruck explosion") Technology1 week ago

Technology1 week agoLas Vegas police release ChatGPT logs from the suspect in the Cybertruck explosion

-

Movie Reviews1 week ago

Movie Reviews1 week ago‘How to Make Millions Before Grandma Dies’ Review: Thai Oscar Entry Is a Disarmingly Sentimental Tear-Jerker

-

Health1 week ago

Health1 week agoMichael J. Fox honored with Presidential Medal of Freedom for Parkinson’s research efforts

-

Movie Reviews1 week ago

Movie Reviews1 week agoMovie Review: Millennials try to buy-in or opt-out of the “American Meltdown”

-

News1 week ago

News1 week agoPhotos: Pacific Palisades Wildfire Engulfs Homes in an L.A. Neighborhood

-

Business1 week ago

Business1 week agoMeta Drops Rules Protecting LGBTQ Community as Part of Content Moderation Overhaul