Finance

Is The Bitcoin Price Still Correlated With Financial Markets?

That is an opinion editorial by Mike Ermolaev, head of public relations and content material at Kikimora Labs.

Setting The Context: World Financial system Fundamentals

The financial system remains to be recovering from the COVID-19 outbreak as new issues come up. We at the moment are in a time of rampant inflation with central banks making an attempt to treatment that by elevating rates of interest.

The U.S. CPI knowledge (shopper value index), launched on October 13, got here in larger than anticipated (8.2% year-over-year), negatively impacting the bitcoin value. However inflation isn’t the one concern, the worldwide financial system can also be battling the power disaster, affecting Europe greater than the U.S., as a result of its robust dependency on Russian pure fuel and uncooked materials.

On the jap aspect, the battle in Ukraine with ensuing sanctions on Russia, add additional geopolitical instability and financial uncertainty. Additionally, China’s zero-COVID coverage is disrupting the availability chain worldwide, and the Evergrande default undermines one of many world’s largest economies.

If we take a look at the primary currencies, the greenback index seems robust, in comparison with others. The Federal Reserve raised rates of interest by 75 foundation factors in November, and the Financial institution of England raised rates of interest by the identical quantity. This coverage of quantitative tightening goals to cut back the cash provide and mitigate value strain. It’s prone to proceed into subsequent yr and past. Nonetheless, a worldwide recession and danger of stagflation remains to be very robust, so no nation could really feel protected from central financial institution financial coverage.

Bitcoin Correlation With The Financial system

Bitcoin has proven to not be immune from this international turmoil. Though the worth in its early stage was unbiased of conventional finance, correlation started to point out in 2016.

The concept of bitcoin as a “digital gold” grew to become fashionable as a result of each shared the shortage and issue of extraction (mining), in addition to fulfilled the function of being a retailer of worth. Since many view bitcoin as a danger asset, its correlation with the S&P 500 and Nasdaq-100 grew to become seen — no completely different than conventional shares.

On the time of writing, bitcoin’s 40-day value correlation with gold reached 0.50 (after being round zero in August). Based on Alkesh Shah and Andrew Moss, strategists from Financial institution of America:

“A decelerating constructive correlation with SPX/QQQ and a quickly rising correlation with XAU point out that traders could view bitcoin as a relative protected haven as macro uncertainty continues and a market backside stays to be seen.”

Damaging Occasions

There are some macroeconomic elements within the bigger cryptocurrency ecosystem that contributed to a bearish market: the Terra/LUNA collapse, compelled liquidation of Three Arrows Capital and the chapter of Celsius being the primary ones.

The incoming bitcoin mining laws by the EU and the present profitability disaster of bitcoin mining should be additionally considered.

Bitcoin: Current And Future

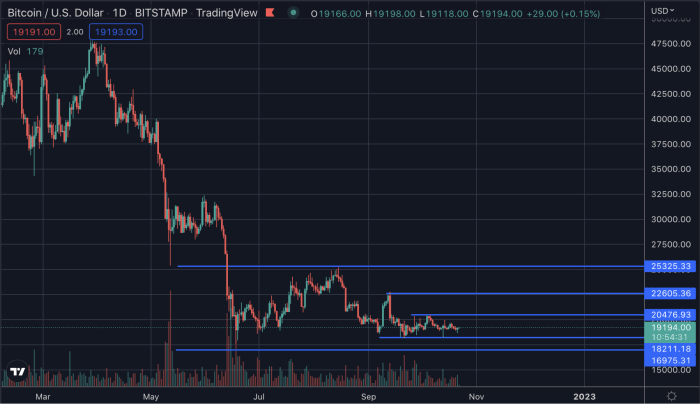

Regardless of all of the above hostile occasions, bitcoin was capable of one way or the other hold its value within the $19,000-$20,000 vary, with record-low volatility. Presently, we’re observing uncommon stability within the bitcoin value, not too long ago even matching volatility of the British pound.

Quite the opposite, shares have skilled excessive volatility and whipsaw value motion, additionally following speculations in regards to the Fed’s future choices. Based on Bloomberg’s Chief Commodity Strategist Mike McGlone, that’s why bitcoin could rise after a steep low cost and ultimately beat the S&P 500. He believes that bitcoin’s finite provide and deflationary strategy could assist it recuperate its earlier value ranges.

Because the final flash crash in mid-June, the worth has been fairly regular, however we all know it not often sits nonetheless for too lengthy. Which means that the likelihood of a sudden (bullish or bearish) breakout will increase over time. The longer the worth stays idle, the stronger the breakout goes to be.

Bitcoin value consolidation

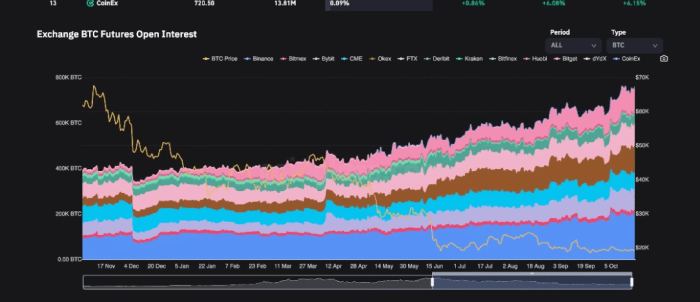

Moreover, the BTC futures open curiosity is larger than ever, with liquidations reaching all-time low. Quite a lot of liquidity is accumulating right here, that means that there will likely be an excellent stronger impulse when the worth begins to maneuver once more.

(Source)

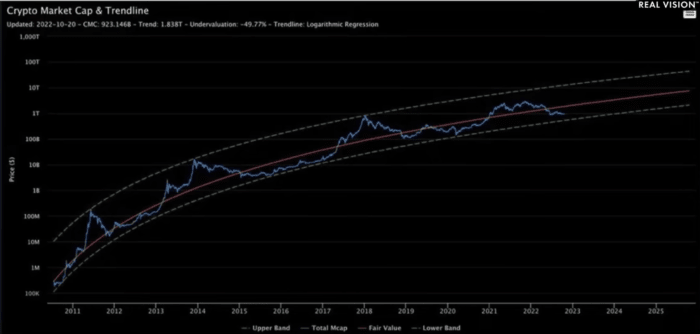

Based on the strategist Benjamin Cowen, bitcoin is predicted to rise to “truthful worth,” after falling an extra 15%. “Proper now, the info would recommend that we’re about 50% undervalued in comparison with the place the truthful worth is.” Cowen thinks we might have to attend till early 2024 to see this rise occur.

(Source)

Goldman Sachs strategist Kamakshya Trivedi has a distinct view, claiming that the U.S. greenback index, exhibiting report values since 2002, could also be unhealthy information for the at present bearish bitcoin.

A Bearish Situation: Might The 2018 Drop Occur Once more?

Some analysts have been questioning if the 2018 state of affairs (low volatility, then large value drop) could occur once more right this moment as a result of the market circumstances look fairly comparable. Now we have the identical 10% buying and selling vary and we all know one thing goes to occur quickly.

Comparability between 2022 BTC value (prime) versus 2018 (backside) utilizing eight-hour candles. (Source)

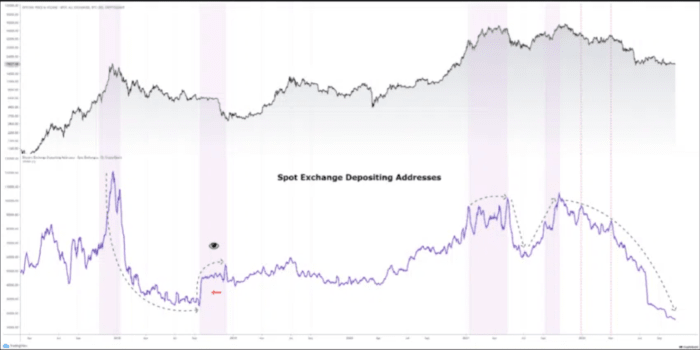

A exceptional distinction between the 2 cycles is that in 2018 there was a rise in addresses despatched to identify exchanges, whereas in our present cycle we’re observing liquidity transferring away from exchanges and never many new addresses being created. Based on a CryptoQuant analyst, this could imply that we received’t witness an analogous state of affairs to 2018.

A 2018/2022 comparability of spot change depositing addresses. (Source)

What About Uptober and Moonvember?

Traditionally, This fall is a superb time for bitcoin, with bullish tendencies beginning in October and growing in November. So the months of October and November have been colloquially renamed “Uptober” and “Moonvember” — no less than, that is what occurred again in 2021.

Can we nonetheless count on such a bullish This fall in 2022? It’s exhausting to say, however the hostile macroeconomic state of affairs and geopolitical points make it tougher to think about the identical rally we noticed final yr. In any case, the bitcoin market has been down for 10 consecutive months and we don’t see any specific signal of restoration in the meanwhile.

We should additionally remember the fact that, regardless of the detrimental international state of affairs, the “protected haven” function of bitcoin could contribute to giving the worth some further energy, particularly in these troubled instances.

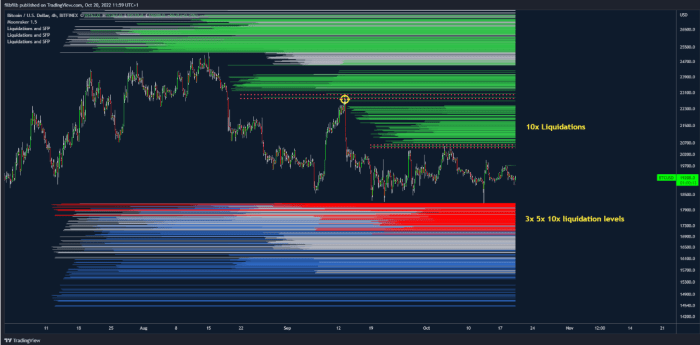

Alternate Knowledge Evaluation

Liquidation knowledge on the Bitfinex change was analyzed by filbfilb. He concluded that an upward breakout would have much less momentum than a downward one. In truth, liquidity above $20,500 is usually 10x, whereas liquidity beneath $18,000 is predominantly 10x, 5x and 3x, which signifies that a bullish breakout could be “much less brutal” than a bearish one.

Bitfinex liquidation chart. (Source)

Conclusions

We’re at present witnessing a interval of stasis within the bitcoin market. The bitcoin value wants to start out transferring once more after two months of consolidation. The general financial state of affairs doesn’t look shiny in any respect, and bitcoin is correlated to occasions in the true world, however traders can nonetheless acknowledge the digital gold, safe-haven function of the most well-liked cryptocurrency. A robust bitcoin value breakout is predicted, with new volatility incoming.

The attainable eventualities could also be: a fast dump after which a bullish restoration (V-shaped bounce) or an extended and deeper value collapse, after the break of the $19,000 resistance stage.

No matter occurs, bitcoin will hold being probably the most modern know-how of the final decade, permitting monetary freedom and direct management over one’s personal wealth. Bitcoin has traditionally witnessed quite a few robust bearish instances and has at all times recovered from them.

This can be a visitor put up by Mike Ermolaev. Opinions expressed are completely their very own and don’t essentially replicate these of BTC Inc. or Bitcoin Journal.

Computer glitches in the U.S. Department of Education’s recently overhauled financial aid system have left many students unable to commit to a school.

Jojo Henderson, a senior from Pittsburg, Texas, was stuck in limbo for months while waiting to learn what sort of financial aid he might get.

“I’m frustrated because it’s just like, you do everything that you’re supposed to do and then you have to wait on the government to catch up,” Henderson told CBS News.

Henderson filled out the free application for federal student aid, known as FAFSA, almost five months ago. With just weeks to go before graduation, he finally received his financial information last week — after some college deadlines had already passed.

Typically, the Department of Education releases the forms on Oct. 1 and sends the students’ data to colleges within one to three days of a submission. This year, the application forms came out three months late. It’s estimated that more than 25% of colleges have still not sent aid packages, according to a report last week from the National Association of Student Financial Aid Administrators.

New Jersey senior Jailen James finally received her aid package close to the decision deadline. She told CBS News that before it arrived, she considered giving up and not going to college.

“I was just so tired of waiting,” she said.

As the FAFSA fiasco continues, Sara Urquidez, who oversees college counseling for thousands of public school students in the Dallas area, said those who are stuck waiting should follow up as much as possible.

“Ask for extensions. Ask if deposits for housing are refundable. Ask for anything they possibly can to help make [a?] decision,” she told CBS News.

Financial services firm Shriram Finance will sell its housing finance arm to private equity major Warburg Pincus for Rs 4,630 crore. This is reportedly Warburg Pincus’ single-biggest deal in India in over two decades.

Warburg will invest another Rs 1,000 crore in the 2011-incorporated Shriram Housing Finance (SHF) after the closure of the deal, which is expected by the end of fiscal in March 2025, Shriram’s executive vice chairman Umesh Revankar said. SHF has grown at a compounded annual rate of over 50 per cent and the Shriram group wishes to focus on its mainstay of small business and vehicle lending rather than pumping capital into the company, Revankar added.

He said Shriram Finance has made an internal rate of return of 22 per cent on the capital deployed in SHF.

Shriram Finance owns 83.8 per cent of SHF while 14.8 per cent is with PE player Valiant, which is also divesting its stake in full, and the remaining 1.4 per cent is with employees. Under the deal, SHF would be acquired by Warburg Pincus through its affiliate Mango Crest Investment Ltd from all the sellers.

“The proposed transaction is valued at Rs 4,630 crore for equity and convertible instruments of SHFL,” Shriram Finance said in a regulatory filing.

The deal needs go-ahead from National Housing Bank, Competition Commission of India and Reserve Bank, he said. Shriram Finance is one of India’s leading NBFCs, serving over 84 lakh customers across India offering commercial vehicle loans, two-wheeler loans, and MSME financing.

SHF has a total employee base of 3,000 people. Following the conclusion of this transaction, it said,SHF will operate as a standalone entity, continuing to enhance value for its stakeholders as it preserves its heritage and mission to provide housing finance solutions to the under-served population of the country.

Shriram Finance MD & CEO Y S Chakravarti said, “We believe that this transaction is in the best interest of SHFL shareholders towards greater value generation and comes at an opportune time for us as well.”.

Shriram Finance Limited will continue to focus on growth led by the short to medium-tenor consumer finance business while Shriram Housing Finance will now chart out its differentiated path, he said. Narendra Ostawal, Head of India Private Equity, Warburg Pincus said, “We remain excited about the affordable housing finance segment in India…their strong team, consistent improvement in financial metrics, geographically diversified presence, customer-first approach, and robust processes are aspects that stand out.” The Shriram Finance scrip closed 1.91 per cent down at Rs 2,300.90 a piece on the BSE as against a 0.15 per cent gain on the benchmark.

Could consumer-facing tech behemoths (such as Alphabet, Apple or Meta) disintermediate financial … [+]

The rise of generative AI has led to much hand-wringing and discussion about the potential for the technology to disrupt industries and eliminate broad swathes of human jobs. But the impact of the technology will vary from industry to industry, so it’s important to look beyond the high-level talk around disruption and to think through exactly how it will change the financial services sector.

In the case of financial services, the impact of generative AI can be simplified into three possible future scenarios: 1) non-financial tech firms develop a dominant generative AI-based personal assistant and disintermediate financial firms, 2) no disintermediation, but the technology further entrenches the dominance of the largest global banks, and 3) no firms manage to establish dominant generative AI assistants, and the technology becomes commonplace without drastically altering market share.

While we can’t predict the future, it’s essential that financial services organizations think through the three possible outcomes to develop long-term plans for how their business would react to each of these scenarios.

Before diving into this topic, a caveat. The goal of this article is to to make the subject approachable for someone who is not familiar with the nuances of generative AI. This article will not discuss the technical developments that would drive these outcomes – e.g., whether it becomes cheaper and easier to build a proprietary large language model (LLM). This article will guide non-technical individuals through how generative AI will impact the financial services industry.

Scenario one: non-financial tech player(s) take a dominant position

One possible outcome for generative AI technology is that the consumer-facing tech behemoths (such as Alphabet, Apple or Meta) and/or a breakthrough tech startup develop consumers’ go-to personal assistant for a very wide range of life tasks, including personal finance. Consumer behavior changes, and the average person looks to the leading generative AI-based virtual assistant(s) with dominant market share to help them with questions and concerns.

This outcome sees generative AI technology evolve in such a way that tech firms are able to develop a superior personal assistant that is so advanced it incentivizes consumers to almost exclusively use their personal assistant. This assistant would monitor consumers’ affairs (via linked outside accounts) and would provide advice when asked questions like “how can I improve my financial situation?” or “could my savings be earning more?” This development would disintermediate financial services firms and the assistant would be able to influence consumers’ financial decisions and behaviors.

An advanced AI-based general personal assistant with dominant market share would disintermediate … [+]

If this scenario becomes reality, the response of financial services firms to this disintermediation partly depends on how regulation shakes out and whether AI assistants can earn referral fees. Beyond the referral question, in the long-term this outcome would likely make the financial services industry much more cutthroat.

In this scenario, financial services firms would need to become far more innovative and would need to develop compelling and unique products and services. Financial services firms would need to incentivize clients to actually log into their website and app and not just rely on their personal assistant. A generic product lineup and a generic client experience would gradually lose market share in a world driven by tech firms’ high-performing virtual assistants.

According to Remco Janssen, Founder and CEO of European tech news media company Silicon Canals, “in past tech hype cycles, the established tech giants were often slow to react. When it comes to generative AI technology, however, the largest firms have acted quickly. Tech behemoths like Apple, Google and Amazon

Amazon

Scenario two: the largest financial firms use gen AI to further entrench their dominance

In this scenario, generative AI technology develops in such a way that tech companies do not disintermediate financial services firms, but the costs and complexity of advanced AI technology allows the largest global banks to gain a competitive edge over relatively smaller rivals in the industry. For an example of the gulf between the top financial services firms and the next tier of financial institutions, as of May 10th, the market capitalization of JPMorgan Chase ($570.80 billion) and Bank of America ($300.69 billion) both exceed the combined market capitalization of US Bancorp, PNC, Capital One and Truist. The combined market capitalization of those four institutions is “only” approximately $235 billion.

The largest banks can dedicate far more resources generative AI. The CEOs of Wells Fargo, Bank of … [+]

It may turn out that the largest financial firms–those which can afford expensive engineering talent and cloud computing resources–can develop meaningfully more powerful generative AI-based financial assistants than the average financial services firm and the industry’s third-party vendors. If the largest global banks can offer a superior generative AI-based financial assistant, they will use this offering to further entrench their dominance of the industry and to win market share from relatively smaller firms.

Scenario three: no dominant gen AI assistants emerge

The final scenario sees generative AI technology become somewhat of a commodity and no firm develops a meaningfully superior generative AI assistant. Generative AI-based assistants become a standard feature of financial services websites and apps without fundamentally disrupting the industry and changing market share dynamics. Financial services firms may even end up relying on multiple third-party generative models simultaneously, calling upon different models depending on the user’s needs.

In this scenario, financial services firms would need to be thoughtful about how they optimize their generative AI assistant to minimize costs and maximize revenue. Financial services firms would work to continually improve their generative AI’s ability to handle customer service questions (preventing more expensive queries to the customer service call center) and to drive desirable actions (e.g., establishing direct deposit, opening a new account, etc.). While this third scenario presents less of a threat to the average financial services firm, developing a high-quality generative AI assistant still represents a large and complex undertaking.

If no dominant generative AI assistants emerge, firms would look outperform peers via superior user … [+]

According to Dr Andreas Rung, CEO and Founder of Ergomania, “banks and financial institutions have a tendency to keep big tech initiatives in the experimental/ideation phase for too long. Time is of the essence when it comes to generative AI. Your organization needs to move quickly to deploy a generative AI assistant to your customer base. In order to keep pace with the competition, your generative AI assistant must also become a seamless part of the UX and customer experience.”

Gen AI has the potential to upend financial services, and firms must start planning for future scenarios now

Only time will tell how generative AI technology develops and which of these three scenarios becomes reality. But your organization should start to think through these outcomes and how to react in each situation. Could your organization restructure and make a massive investment in developing a cutting-edge generative AI assistant if that becomes necessary? If your firm uses a third-party AI vendor, what are the “switching costs” if your firm “backs the wrong horse” and must make a change in order to keep pace with the leading firms? In each of these scenarios, how would your firm adjust the human workforce? It is better to start planning now than to be reactive and scrambling to catch up to changing market dynamics.

According to Milan De Reede, Founder and CEO of Nano GPT, “I see our customers’ preferences shift in real time as new generative AI models and updates are released. There’s no clear “winner” as of May 2024. Our customers seem to prefer different generative AI models for different tasks. At some point in the future, your firm may need to change your generative AI infrastructure and approach relatively quickly depending on which of these three scenarios becomes reality.”

Idaho doctor, accomplished outdoorsman, dies in avalanche while skiing Lost River Range – East Idaho News

Dolton, Illinois, officials approve mayor pro tem

Indiana Forest Alliance rallies to protect urban forests

Iowa women's basketball coach Lisa Bluder announces her retirement

Kansas City Chiefs kicker Harrison Butker slams Biden’s ‘delusional’ stance on abortion in commencement speech

See it: Tesla crashes into Columbus convention center at 70 mph

Colorado Rockies game no. 116 thread: Zac Gallen vs José Ureña

Fox News Politics: Georgia the whole day through

Death of missing Oregon girl found in stream ruled homicide

At least 2 dead as tornadoes hit Alabama, damage homes across Southeast

Reports of Biden White House keeping 'sensitive' Hamas intel from Israel draws outrage

Lawrence Wong set to take centre stage as Singapore’s new prime minister

Pasadena reels from Tesla crash that left 3 dead, 3 injured

Jill Biden tells Arizona college graduates 'community colleges should be free in America'

Germany's Weber supports Macron’s call for European nuclear deterrent

-

Politics1 week ago

Politics1 week agoAustralian lawmakers send letter urging Biden to drop case against Julian Assange on World Press Freedom Day

-

World1 week ago

World1 week agoBrussels, my love? Champage cracked open to celebrate the Big Bang

-

News1 week ago

A group of Republicans has united to defend the legitimacy of US elections and those who run them

-

Politics1 week ago

Politics1 week agoHouse Dems seeking re-election seemingly reverse course, call on Biden to 'bring order to the southern border'

-

World1 week ago

World1 week ago‘It’s going to be worse’: Brazil braces for more pain amid record flooding

-

Politics1 week ago

Politics1 week ago'Stop the invasion': Migrant flights in battleground state ignite bipartisan backlash from lawmakers

-

World1 week ago

World1 week agoGerman socialist candidate attacked before EU elections

-

World1 week ago

World1 week agoSpain and Argentina trade jibes in row before visit by President Milei