Finance

Financial Nihilism & The Trap Young Investors Are Walking Into

The article from the Wall Street Journal titled “Why My Generation Is Turning to Financial Nihilism” by Kyla Scanlon argues that Gen Z is embracing high-risk financial behavior out of despair and detachment. Of course, it is essential to recognize that Kyla, although well-intentioned, is a young twenty-something influencer with limited real-life experience, and sees things for “her generation” through a very narrow lens of “recency bias.”

Let’s start with understanding that “Financial Nihilism” is a term used to describe an attitude where people believe financial decisions are meaningless because the system is rigged, the future is hopeless, or traditional paths to wealth are broken. The term “Financial Nihilism” was first coined in 2020 by Demetri Kofinas, a podcaster, who used it to describe his belief that speculative assets lack intrinsic value, driven by a loss of faith in traditional economic systems.

However, while this phrase has gained popularity in recent years, particularly following the GameStop short squeeze, crypto mania, and the rise of meme trading, it disappeared when all of that collapsed in 2022. However, after three years of unprecedented market gains in every asset class, from stocks to cryptocurrencies to precious metals, “Financial Nihilism” has resurfaced to rationalize “speculative excess” and justify abandoning long-term investment strategies that have withstood the “sands of time.”

While Kyla produced a bombastic article to gain social media exposure by suggesting that Gen Z and Millennials no longer believe in saving, investing, or following traditional financial paths, the data shows something very different.

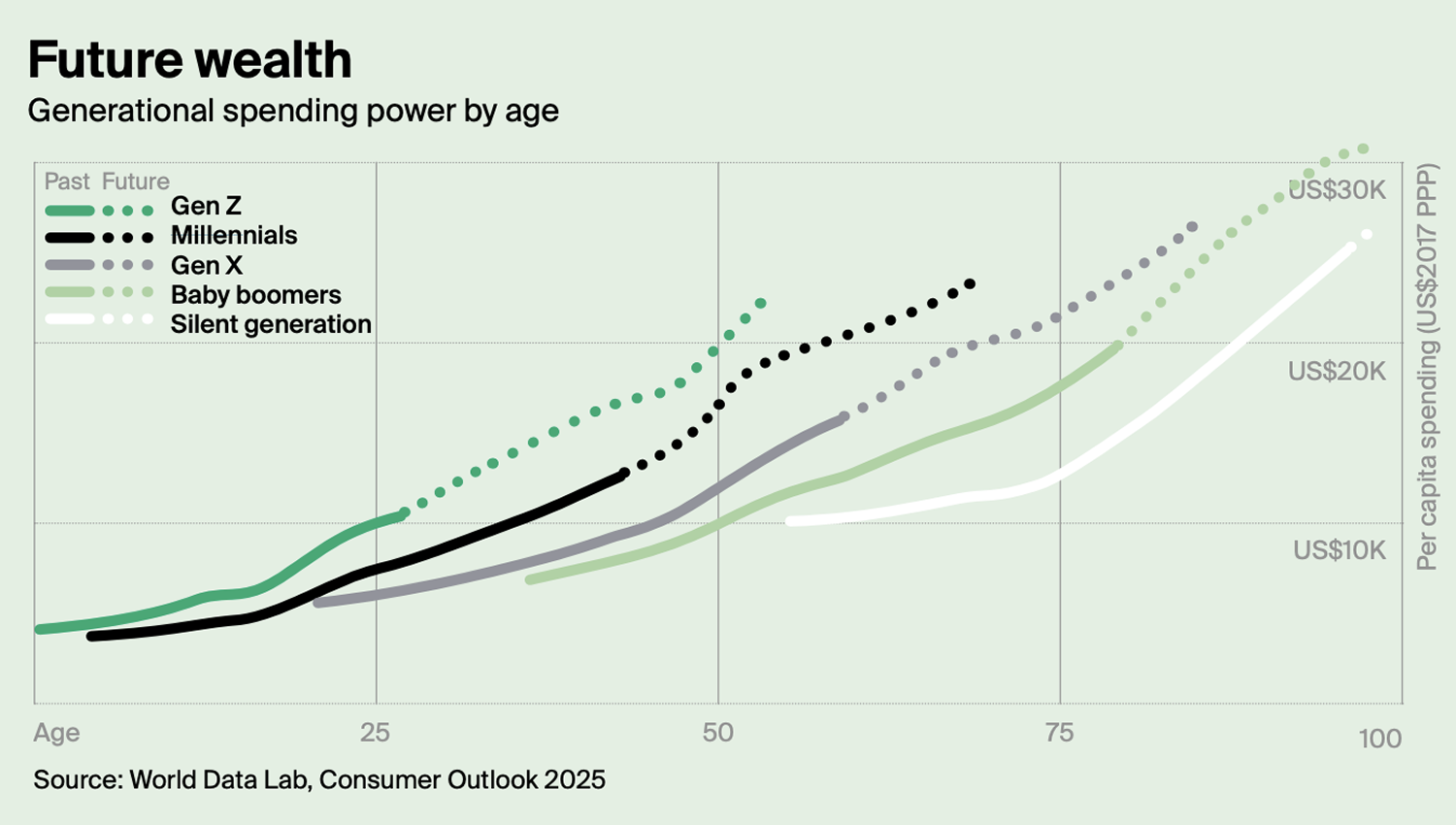

- Over half of Gen Z holds investments in traditional financial products, according to FINRA and the CFA Institute.

- A 2023 Vanguard report showed Gen Z participants in retirement plans were increasing contributions, not fleeing traditional investing.

- Charles Schwab’s Modern Investor Study found Gen Z prefers low-cost ETFs and index funds, strategies built around long-term returns.

- Pew Research data shows that Gen Z and Millennials are investing at earlier ages than previous generations.

None of these behaviors is nihilistic. They are practical and reflect economic constraints, not philosophical despair.

Yes, there is undoubtedly a pool of young investors throwing “caution to the wind” and aggressively investing in speculative assets to “get rich quick.” But even my children, at the ripe old age of 22, think they are unique and different and that no one understands their challenges. We parents, of course, have “no idea” about their situation. Of course, this is the problem with our youth who have no real-world experience or a sense of history. We, the “old people,” were the ones speculating on Dot.com investments in the late 90s, just before it all went bust. As I wrote in“Retail Investors Flood The Market,”

“Is it 1999 or 2007? Retail investors flood the market as speculation grows rampant with a palpable exuberance and belief of no downside risk. What could go wrong?

Do you remember this commercial?

That commercial aired just 2 months shy of the beginning of the “Dot.com” bust. We “youngsters” at the time thought Warren Buffett was an idiot for avoiding technology stocks because “he didn’t get it.”

Turns out he was right.

But that wasn’t the first time that we youngsters had to learn the risks of chasing “hot investments,” and why “this time is NEVER different.” The following E*Trade commercial aired during Super Bowl XLI in 2007. The following year, the financial crisis set in, markets plunged, and once again, investors lost 50% or more of their wealth by refusing to listen to the warnings.

Why this trip down memory lane? (Other than the fact that the commercials are hilarious to watch.) Because what is happening today is NOT “Financial Nihilism,” it is the typical outcome of exuberance seen during strongly trending bull market cycles.

While young people, like Kyla, may think that “this time is different,” they lack the historical experience to support such a conclusion. Ask anyone who has lived through two “real” bear markets, and the imagery of people trying to “daytrade” their way to riches is all too familiar. The recent surge in speculative excess, leverage, and greed is not a new phenomenon.

With that said, let’s examine the issues with Kyla’s article and why “Financial Nihilism” is a myth.

“Meme Stocks and Crypto Aren’t Jokes Anymore. They’re Cries for Help.”

I loved this line from her diatribe as it suggests that Gen Z uses risky financial products as an emotional outlet. She implies that young people are not seeking returns but rather relief from feelings of hopelessness. While that framing sells well, it doesn’t hold up under scrutiny. While speculative assets like cryptocurrency and meme stocks attract younger buyers, that’s not proof of despair. Instead, it reflects broader exposure to digital markets, higher risk tolerance, easy access to trading (via platforms like Robinhood), leverage, and the rise of a gambling mentality.

But this is a newer development.

“Historically, access to capital markets was highly mediated, available only to institutions or individuals who had the time, money and resources to manage their assets with the help of brokers and financial advisors. Today, market data is readily accessible online and new technologies have significantly reduced the cost of trading and other barriers to entry. This means that more people can trade, at any time, from anywhere.” – World Economic Forum

Since 2016, the volume recorded at platforms that match orders from brokerages, a proxy for retail activity, has posted its third consecutive annual increase, rising by 15%. Meanwhile, the average daily volume of US-listed stocks has been ~12.0 billion shares since 2019, which is ~75% above the levels seen over the prior six years. Most notably, just over the last 12 months, daily volume has averaged a massive 16.7 billion shares.

Yes, retail investors are piling into the market. But why wouldn’t they after watching 15 years of market returns that are 50% above historical norms, and seeming “no risk” for speculative activities?

However, there is a difference between risk appetite and recklessness. As noted above, the data indicate that Gen Z is starting to engage with investing at a younger age than previous generations, and many hold investments for the long term while utilizing digital tools to experiment with their investments. That may include crypto or options, but it’s not a binary between discipline and nihilism.

Emotional narratives about “cries for help” obfuscate the data. Investors in their 20s often take more risk because they have longer time horizons. But where they are going wrong is through the amount of speculative risk and gambling behaviors they have adopted without financial guidance and education.

As noted above, “youngsters” gambling with investments is not new. Every generation throughout history has speculated on risk assets through every bull market cycle. But, unfortunately, regardless of age, speculative bubbles all ended the same way.

Gen Z didn’t “reinvent” the market; they are just entering a market that incentivizes risk-taking. Until it doesn’t.

“People My Age Don’t Think the System Works, So Why Follow Its Rules?”

Scanlon asserts that Gen Z has lost faith in traditional finance and institutions, and assumes systemic distrust is translating into a rejection of personal responsibility.

That isn’t an argument. It’s an excuse for “victimization.”In other words, my personal financial situation is not a result of my personal behaviors, spending habits, work ethic, or savings process, but it’s the “system’s fault.” Yet there is vast data to the contrary, showing that successful young individuals who follow the tried-and-true process of financial pathways succeed. Do they have as much wealth as their parents? Of course, they don’t, because they haven’t had the time to accumulate it. However, they are early on the path to success, which will likely outpace their peers.

Furthermore, this argument falsely equates skepticism with nihilism. Many young investors distrust centralized finance due to real-world events, including the 2008 crash, rising debt burdens, and stagnant wages. But rejecting blind trust in institutions is not the same as rejecting financial logic. Despite disillusionment, Gen Z invests at higher rates than Millennials did at the same age, according to Pew and the WEF. They also save a larger share of their income, using digital apps and platforms to automate their financial behavior.

Yes, Gen Z tends to distrust the government and financial media, but do you blame them, given the garbage that is produced daily on social media and YouTube by people with an agenda to promote? While skepticism fuels caution, it is not chaos. Gen Z is more likely to question fees, demand transparency, and seek passive investment tools, and that’s a smart move. Traditional rules of finance, such as saving consistently, spending less than you earn, and investing for the long term, are still followed; they just don’t generate “media-grabbing headlines.”

Calling this behavior “Financial Nihilism” misses the point. Gen Z is engaging with markets on its own terms, and while not all methods are necessarily healthy, it represents adaptation, not rejection.

“If the Future Feels Doomed, Why Not YOLO Trade Into It?”

Lastly, Kyla suggests that existential dread leads young people to treat the market like a casino. The idea is that if nothing matters, risk doesn’t either. This is the article’s weakest argument. While social and economic pressures are real, they are not driving widespread self-destruction. They are driving innovation in how people build and manage their wealth.

The idea behind this line is that young people, facing what feels like a bleak financial future, are throwing caution to the wind to gamble on crypto, options, and meme stocks to build wealth fast, rather than creating “lasting wealth.” This is where the term “YOLO trading” comes in, making aggressive bets with the mindset that there’s nothing to lose. However, as noted above, there is certain logic to that mindset, given that over the last 15 years, every market downturn has been met by either fiscal or monetary interventions. Repeated bailouts of bad investment decisions have created a “moral hazard” in the marketplace.

There’s truth here, but only part of it.

Yes, a subset of young investors is engaging in reckless speculation. They take on excessive risk, invest in volatile assets, and often trade on hype rather than fundamentals. Many borrow money to do it. This group exists, and their outcomes won’t be good. Some will lose money, and likely most will wipe themselves out entirely. The market is unforgiving when paired with leverage, inexperience, and emotional trading.

Here is a great example of the “YOLO” trading fallacy. Since the end of the “Meme Stock” craze in 2021, retail investors on Robinhood have made no money, even after accounting for the $4-5 billion wipeout in the January rout. That’s 5 years of their investing time horizon gone, whereas just investing in the S&P 500 index would have produced far superior results.

But this behavior doesn’t define the generation. It represents the tail end of the distribution—the loudest, not the largest.

What’s left out of Kyla’s article is what happens after the eventual realization that “trading” is a losing exercise over the long term. Early losses are the price of financial education, and, hopefully, if they survive financially, they will change their approach and revert to more traditional principles that have endured over the decades. In other words, they grow up and learn from the experience just as every great investor in history has.

The future is not doomed. But it is fragile for those who ignore risk. Financial outcomes depend on staying in the game long enough to benefit from compounding. If you blow yourself up in your 20s, you lose that opportunity.

The lesson is simple. Speculation is fun while you are winning, but that is not “Financial Nihilism.” It is simply greed masquerading as investing. However, the people who win in the long term are not gamblers. They’re grinders. They keep costs low, automate savings, and make decisions that allow them to survive market cycles. That’s not as flashy as YOLO trading, but that is how wealth is built.

What Gen Z Should Do: Build Survivability, Not Sensation

Despite the bad headlines, most young people are serious about their money. But seriousness alone doesn’t build wealth. The key is survivability, the ability to stay in the game long enough to benefit from compounding returns.

Do yourself and your financial future a favor: turn off bombastic, emotionally charged headlines and focus on what matters for building long-term wealth. Crucially, whether you agree with the current financial and economic system or not, learn to take advantage of it.

The only thing YOU can change is YOUR future. So stop worrying about things you can not control.

To get there, start here.

- Turn off the social media, influencers, and other financial goblins and focus on your goals and behaviors.

- Keep fixed expenses low

- Build cash reserves that cover 6 months of spending

- Use retirement accounts like Roth IRAs early

- Allocate most of their portfolio to index funds or ETFs

- Limit risky bets to no more than 5% of their total assets

- Learn through action, not theory, and track everything

- Avoid the leverage period.

The goal is not to outperform every year or get rich quickly. The goal is to stay solvent long enough for your savings to generate a return.

Financial nihilism is a myth. What’s real is volatility, income pressure, and distrust. The response shouldn’t be disengagement, but rather financial discipline. Long-run wealth isn’t about hope; it’s about repeatable behaviors that work consistently through market cycles.

The biggest problem for most young investors is the lack of research on the stocks they buy. They are only buying them “because they were going up.”

However, when the “season does change,” the “fundamentals” will matter, and they matter a lot.

Such is something most won’t learn from “social media” influencers.

As Ray Dalio once quipped:

“The biggest mistake investors make is to believe that what happened in the recent past is likely to persist. They assume that something that was a good investment in the recent past is still a good investment. Typically, high past returns simply imply that an asset has become more expensive and is a poorer, not better, investment.”

Investing is a game of “risk.”

It is often stated that the more “risk” you take, the more money you can make. However, the actual definition of risk is “how much you will lose when something goes wrong.”

Following the “Dot.com crash,” many individuals learned the perils of “risk” and “leverage.”

Unfortunately, for Gen-Z’ers, such is a lesson that is still waiting to be learned.

The Monetary Authority of Singapore (MAS), the city state’s central bank and financial regulator, has joined forces with major financial institutions and FinTechs to release a white paper aimed at keeping AI agents in finance operating within safe limits.

The paper, called Safeguards for Agentic Finance at Runtime (SAFR), lays out an industry-built framework designed to let AI agents perform financial tasks in a manner that is safe, secure and dependable. It has been produced under BuildFin.ai, the MAS programme that backs the responsible creation and rollout of AI tools across the financial sector.

The push comes as AI agents take on more autonomous work at a pace that makes hands-on human oversight impractical. In response, firms require real-time controls that keep agent behaviour inside the mandates, policies and risk limits they have defined. SAFR answers this with a series of governance checkpoints that check and log each action an agent proposes before that task is carried out.

The framework extends the AI Risk Management toolkit created through MAS’ Project Mindforge, concentrating on how protections can be put into practice at the moment an agent acts. The white paper maps out how measures such as policy bound execution, real time validation, auditability and interoperability can be woven into system operations, giving institutions the confidence to deploy agents consistently.

Industry participants have already tested SAFR in several settings. These include agent-assisted payments and treasury work, where agents handle routine transactions inside set mandates to cut friction and lift efficiency; wealth management and advisory processes, where agents examine documents and produce structured assessments within tightly defined task limits to speed up compliance reviews; and client engagement, where agents create insights and draft materials within approved content boundaries so staff can serve clients more productively.

Stay ahead of the regulatory curve. Subscribe to FinTech Global’s newsletter today, and read the daily FinTech news for the strategic intelligence and early insight industry leaders rely on.

Copyright © 2026 FinTech Global

Investors

The following investor(s) were tagged in this article.

Talking about finances can be stressful, but it’s even more stressful if you’re not sure what advice is good and what advice might put you in a worse position than you started in.

Recently, a Reddit user who goes by market_vision1 asked, “What is the worst financial advice people still repeat?” I took out a little pen and paper while I was reading through these, like, “Lemme write that down. And that. Oh! And that, too!” I’m curious what you think, though. Are all of these things we should avoid financially?

1. “One of the more damaging ideas out there is ‘Oh, you’re young, don’t worry about money, just go have fun and worry about it when you are older.’ Of course, the number one regret I hear from clients nearing retirement is that they wish they had just started saving when they were younger.”

—u/hems86

2. “The ‘tax bracket’ myth should be illegal. My uncle turned down a $10K raise because he thought he’d ‘lose money.’ He literally paid $10,000 to avoid $2,200 in taxes. That’s not a tax strategy. That’s a $7,800 donation to the Dumba— Fund, and he’s the chair.”

—u/Serious_Cress5040

Related: “31 Things Only Super Wealthy People Can Buy That You Probably Don’t Even Know Exist”

3. “People living outside of their means and not realizing it. They say things like, ‘You deserve X, don’t settle for less.’ Most of the people I see who are broke are not 100% victims of the system. The majority of people waste their money on dumb stuff that they can’t afford. They’ll tell me they’ve cut out all unnecessary spending, but when I look at their actual expenses, I see otherwise. Spending $800 a month on DoorDash, financing a new car with a $900 monthly payment, going on international vacations, spending 70% of their income on rent in a fancier apartment when there are options for cheaper living.”

—u/hems86

4. “I’m a financial planner, and some of the worst advice I’ve ever heard is ‘Don’t pay off your credit cards in full. Carrying a balance on your credit card builds your credit; paying it off every month hurts your score.’ People say this to me all the time when I ask why they carry a balance on their card with 25% interest when they have more than enough to pay it off.”

—u/hems86

5. “It’s not so much advice as it is a financial choice. I know people who are taking out 96-month loans on cars they never should’ve considered in the first place, just because they can make the car note when it’s stretched over eight years. They never considered the interest on the loan plus the rate cars depreciate and are befuddled when they can’t afford to trade it in.”

Finance

I’m a 25-year-old grad student on a budget. I’ve struggled to accept financial help from my Boomer and Gen X friends.

In August, I quit my steady job as a New York City public high school teacher to start a full-time graduate program in Manhattan. I worried about the choice not only because I loved my work with the kids, but also because I had traded a consistent paycheck and affordable health insurance for tens of thousands of dollars in tuition.

When I was teaching, I prepared for the cost by scrimping to save every cent I could. But my account balance still wouldn’t fully cover two years of school and living expenses.

Throughout my savings journey, I learned a lot of lessons, especially from my older friends.

I jumped into major money-saving mode

As a result, I redoubled my frugal efforts. I made a rule that I wouldn’t eat out or order takeout unless it was someone’s birthday. I asked to meet people in parks rather than restaurants and suggested $5 happy-hour spots from a meticulously crafted list on my phone.

On rare occasions when I dined out, I looked at the prices before deciding what to order and pored over the bill with a calculator.

It worked. While it was still difficult to watch my savings dwindle — buoyed occasionally by small deposits from part-time jobs — I kept my costs (relatively) low for a 20-something in the city. Most friends understood my restrictions or were in similar situations.

I worried when my older friends routinely paid for me

But this approach didn’t work as well with my five older friends from my intergenerational writer’s group. We’d been meeting weekly on Zoom for several years when we started visiting each other in our home states across the country. As women in their 40s and 60s in dual-income households with established careers, they understandably gravitated toward nicer places where the cheapest cocktail cost $20. My dive bars with weirdly stained walls weren’t going to cut it.

When I visited two of these friends in Chicago, I anticipated that we’d go to swanky spots and saved up for weeks, cutting out anything nonessential from my grocery list — chocolate-covered pretzels, bananas, frozen fried rice.

But when I offered to chip in for our multi-course dinners or luxury spa day, they brushed me off.

I was grateful for their generosity, yet overcome with guilt. They had contributed so much to our time together. I didn’t want to be a freeloader, the friend who couldn’t hold up her end of the deal. How could I pay them back and show my appreciation?

At the end of the trip, my friend Andrea, 46, and I ate lunch in a diner in the Gold Coast. I made one last offer to Zelle her. In response, she said something that stuck with me.

“When I was in my 20s, people helped me,” she told me with an easy smile. “When you’re 40, just pay it forward by buying a younger woman dinner.”

Her wisdom helped me slowly release my anxiety

I mulled over her words on the plane home. I was surprised that her view of the situation differed so much from mine, and relieved she didn’t see me as taking advantage of her. Yet it was still hard to fully let go of the weight in my chest — the feeling of being indebted to someone’s kindness, of accepting a gift while knowing you can’t reciprocate.

Months later, my 64-year-old friend from my writer’s group visited from Florida. We went out for coffee, and I thought to myself, Okay, now this I can afford. But when I offered to cover or at least split it, she waved me off, saying, “My treat.”

I thought of Andrea’s words and told myself, She’s being nice. Don’t worry about it.

“Thank you,” I said, and meant it.

A while later, when another friend visited from Washington, she paid most of our checks at the bars and restaurants we visited. Though I felt a twinge of the usual panic at first, by our second day together, I was able to let it go. As we wandered through the Upper West Side, the tightness in my chest lifted, leaving only gratitude that she was here.

I do plan on paying it forward

Andrea was right, I realized. Helping each other was what friends did, and they clearly weren’t bothered by it. Sure, I wasn’t paying for lavish things or hosting people, but I shouldn’t let my own hangups affect our time together, which always produces some of my favorite memories.

Eventually, I’ll be able to do what they’ve done for me for another woman, who can then help someone else.

Instead of worrying, now I let my friends’ kindness bring us together and smile, knowing that every time I pay for a 20-something woman in the future, I’ll think of them.

-

Washington, D.C2 minutes ago

Washington, D.C2 minutes agoWhite supremacist group demonstrates on Capitol Hill ahead of America 250 celebrations

-

Cleveland, OH9 minutes ago

Cleveland, OH9 minutes agoRittman police officer among 4 dead in Wayne County

-

Austin, TX12 minutes ago

Austin, TX12 minutes agoDinosaur Day Returns to Austin with Fossil Identifications, T. rex and Family Fun

-

Alabama17 minutes ago

Alabama17 minutes agoThe 5 most important position battles facing Kalen DeBoer, Alabama ahead of fall camp

-

Alaska24 minutes ago

Alaska24 minutes agoA sympathetic shooter and botched prosecution: How did Lovely Lois get away with murder in 1960s Anchorage?

-

Arizona25 minutes ago

Arizona25 minutes agoWhere to watch Arizona Diamondbacks vs San Diego Padres: TV channel, start time, streaming for July 6

-

Arkansas32 minutes ago

Arkansas32 minutes agoArkansas Storm Team Forecast: Thunderstorms will start to pop around 2:00 this aftenoon

-

Colorado42 minutes ago

Colorado42 minutes agoStartups move to Colorado amid concerns state losing its luster for tech companies