Lopez and Broxel carry monetary alternative to Mexican American group.

getty

Monetary literacy in faculties is usually informally mentioned as important and related to each scholar wishing to succeed after commencement. But, the statistics on these college students receiving classroom curriculum on finance stays extraordinarily low. In keeping with latest knowledge from the nonprofit Subsequent Gen Private Finance, just one out of 5 college students within the U.S. obtain instruction in a private finance class earlier than graduating highschool. Chopping into the low percentages are indicators that minority and low-income college students are even much less more likely to take a course within the topic, in response to Inc.’s article on the perks of monetary literacy coaching.

As reported by The Commonplace’s and Poor’s World Monetary Literacy Survey, a scarcity of monetary literacy in faculties quickly carries over to a world lack of monetary literacy in adults globally. With out the understanding of fundamental monetary ideas, the ill-informed are much less geared up to make monetary administration, saving, borrowing, credit score utilization, and even digital banking selections. For these throughout the states that must ship cash to kinfolk throughout the border to satisfy fundamental wants, monetary understanding and companies achieve much more significance.

Taking the Initiative

Advertisement

The Latin American FinTech firm, Broxel, led by founder Gustavo Gutiérrez has lately taken the monetary initiative, producing a platform that gives financially easy-to-manage remittance funds, integral to the Mexican financial system. Partnering with well-known actor and host Mario Lopez, the message is getting out on the platform that provides free processes with extra cutting-edge functionalities.

Mario Lopez’s expertise is in his potential to characterize a voice for the lots. He does so from a platform steeped in his Mexican American heritage. He is taking the amassed model affinity and making use of it to real-world monetary challenges which have impacted his group for many years.

Flipping traditionally impactful challenges into present-day alternatives, securing monetary independence, and cultural inclusion is on the core of Lopez’s present efforts. His work with Broxel helps the Mexican American group within the U.S. ship cash extra effectively to these south of the border at zero value.

Remittances are important for the Mexican financial system. In the course of the coronary heart of the pandemic, immigrants despatched almost $40 billion to kinfolk in Mexico, with numbers climbing to $51 billion by the top of 2021. Founding father of Broxel, Gustavo Gutiérrez explains, “Know-how is erasing borders. The thought of getting free remittances is an financial disruption for the North American area and a game-changer for thousands and thousands of potential customers. Remittances are used for important wants equivalent to well being care, paying for meals, or having a spot to dwell, and this initiative is the easiest way to thank the epic, each day effort of the Mexican group within the U.S.”

Advertisement

When Broxel approached Mario Lopez to speak the platform, he jumped on the concept of being an lively voice and ambassador. The Latino group is accustomed to paying excessive charges for the cash despatched. “Broxel Pay makes a big impact financially by saving individuals cash by taking away charges,” he says.

Formed by Early Beginnings

Lopez likes how the Broxel Pay app is a borderless answer that’s serving to individuals get monetary savings. His dedication to arduous work and saving cash began on the age of 10 when he broke into the leisure trade out of San Diego.

“I am a toddler of immigrants, my mother and father are from Mexico, they usually instilled a strong work ethic. They have been blue-collar of us, my dad labored for the town, and my mother labored for the cellphone firm. I used to be a border city child in Chula Vista. I used to see Tijuana from my yard, and I cherished it. I would not change a factor. It is like I had a foot in each worlds,” says Lopez.

Advertisement

Mario Lopez and Broxel bringing alternative and monetary independence to thousands and thousands.

Rodney Thurman

He continues, “I think about myself very a lot American. However on the similar time, a part of my tradition may be very Latino. I believe these two worlds can coexist and characterize what America is about. I really like every little thing about America and my tradition, however it does not essentially imply I’ve to hit you over the pinnacle with a tortilla to let you know about it. I believe there is a solution to characterize your group and be a great position mannequin.”

Heritage is interwoven within the relationship between Broxel’s founder Gutiérrez and Lopez. When requested why Mario Lopez is the voice of Broxel, Gutiérrez peered into the digicam tilting his head, saying, “Why not?” Intimating Lopez’s transcending character amongst neighboring cultures.

Entrepreneurism and Branding

Lopez believes that entrepreneurism needs to be based mostly on ardour as a result of it’s going to eat your time and vitality. He feels the youthful era is uniquely positioned to enter entrepreneurial efforts right now greater than ever. Even his 11-year-old daughter has launched an Etsy enterprise, bringing him satisfaction as a father. Creating your individual model is one thing that he realized early in his profession.

Advertisement

“Early on, I labored with Dick Clark, who took me beneath his wing and received me enthusiastic about myself as a model. He mentioned, ‘Mario, you need to focus extra on internet hosting as a result of not solely do you will have the character for it, you are a pure host, and you could possibly be on TV for the subsequent 50 years.’ He talked about how I may parlay my work into endorsements and sponsorships however emphasised the necessity to not stray from my model.”

What’s my model? I am the 5 F’s: household, religion, health, meals, and enjoyable. That is the model’s umbrella, and my tradition is an enormous a part of that too. Being a number, whether or not it is my nationally syndicated radio present, Entry Every day, or Entry Hollywood, locations me I am on TV daily. I attempt to be a pleasant, comfy place for individuals to tune into and never be divisive. I by no means speak politics or faith, although I am a person of religion. I am within the individuals enterprise.”

The monetary sector has notoriously been branded as the nice differentiator between the haves and the have-nots. Nonetheless, with elevated consciousness and monetary literacy inside schooling, the inequities might have a beginning place to shrink the divide.

Along with the efforts in formal studying, people linked to the cultures most in want will stay lynchpins to a treatment. With Lopez, by Gutiérrez and Broxel, there may be now a platform to show the monetary experiences of Mexican Individuals into inclusive alternatives steeped in dignity and group.

Interviews have been edited and condensed for readability.

Block said the issues raised by the regulator were “historical” and did not “reflect the Cash App experience today” [File]

| Photo Credit: REUTERS

The Consumer Financial Protection Bureau (CFPB) on Thursday ordered payments firm Block to pay a penalty citing fraud and weak security protocols on its mobile payment service Cash App.

The regulator said Block, which is led by tech entrepreneur Jack Dorsey, directed Cash App users who experienced fraud-related losses to contact their banks for transaction reversals.

However, when the banks approached Block regarding these claims, Block denied that any fraud had occurred.

Cash App is one of the largest peer-to-peer payment platforms in the U.S. and allows consumers to send and receive electronic money transfers, accept direct deposits and use a prepaid card to make purchases.

Advertisement

“When things went wrong, Cash App flouted its responsibilities and even burdened local banks with problems that the company caused,” said CFPB Director Rohit Chopra.

In response, Block said the issues raised by the regulator were “historical” and did not “reflect the Cash App experience today.”

“While we strongly disagree with the CFPB’s mischaracterizations, we made the decision to settle this matter in the interest of putting it behind us and focusing on what’s best for our customers and our business,” the company said.

The move is one of the final regulatory actions under the Biden administration as Washington awaits the inauguration of President-elect Donald Trump. Billionaire Elon Musk, who is slated to co-head a new government agency to slash government spending, has called for the elimination of the CFPB.

The CFPB’s order includes up to $120 million in redress to consumers and a $55 million penalty to be paid into the CFPB’s victim relief fund.

The regulator also alleged that Block deployed a range of tactics to suppress Cash App users from seeking help in order to reduce its own costs.

Advertisement

Block’s gross profit rose 19% to $2.25 billion in the third quarter ended Sept 30, with Cash App accounting for $1.31 billion of the total income.

On Wednesday, the company also agreed to pay $80 million to a group of 48 state financial regulators after the agencies determined the company had insufficient policies for policing Cash App.

Call Scheduled for 11:30 am ET on Friday, March 14, 2025

NEW YORK, Jan. 16, 2025 (GLOBE NEWSWIRE) — Logan Ridge Finance Corporation (Nasdaq: LRFC) (“LRFC,” “Logan Ridge” or the “Company”) to release its financial results for the fourth quarter and full year ended December 31, 2024, on Thursday, March 13, 2025, after market close. The Company will host a conference call on Friday, March 14, 2025, at 11:30 a.m. ET to discuss these results.

By Phone: To access the call, please dial (646) 968-2525 approximately 10 minutes prior to the start of the conference call and use the conference ID 1779602.

A replay of this conference call will be available shortly after the live call through March 21, 2025.

By Webcast: A live audio webcast of the conference call can be accessed via the Internet, on a listen-only basis at https://edge.media-server.com/mmc/p/h9fj5e3y. The online archive of the webcast will be available on the Company’s website shortly after the call at www.loganridgefinance.com in the Investor Resources section under Events and Presentations.

Advertisement

About Logan Ridge Finance Corporation

Logan Ridge Finance Corporation (Nasdaq: LRFC) is a publicly traded, externally managed investment company that has elected to be regulated as a business development company under the Investment Company Act of 1940. Logan Ridge invests primarily in first lien loans and, to a lesser extent, second lien loans and equity securities issued by lower middle market companies. Logan Ridge Finance Corporation is externally managed by Mount Logan Management, LLC, a wholly owned subsidiary of Mount Logan Capital Inc. Both Mount Logan Management, LLC and Mount Logan Capital Inc. are affiliates of BC Partners Advisors L.P.

Logan Ridge’s filings with the Securities and Exchange Commission (the “SEC”), earnings releases, press releases and other financial, operational and governance information are available on the Company’s website at loganridgefinance.com.

Contacts: Logan Ridge Finance Corporation 650 Madison Avenue, 3rd floor New York, NY 10022

Don Cardinal of Financial Data Exchange (FDX) explores how Open Finance extends beyond Open Banking, revolutionising financial data sharing.

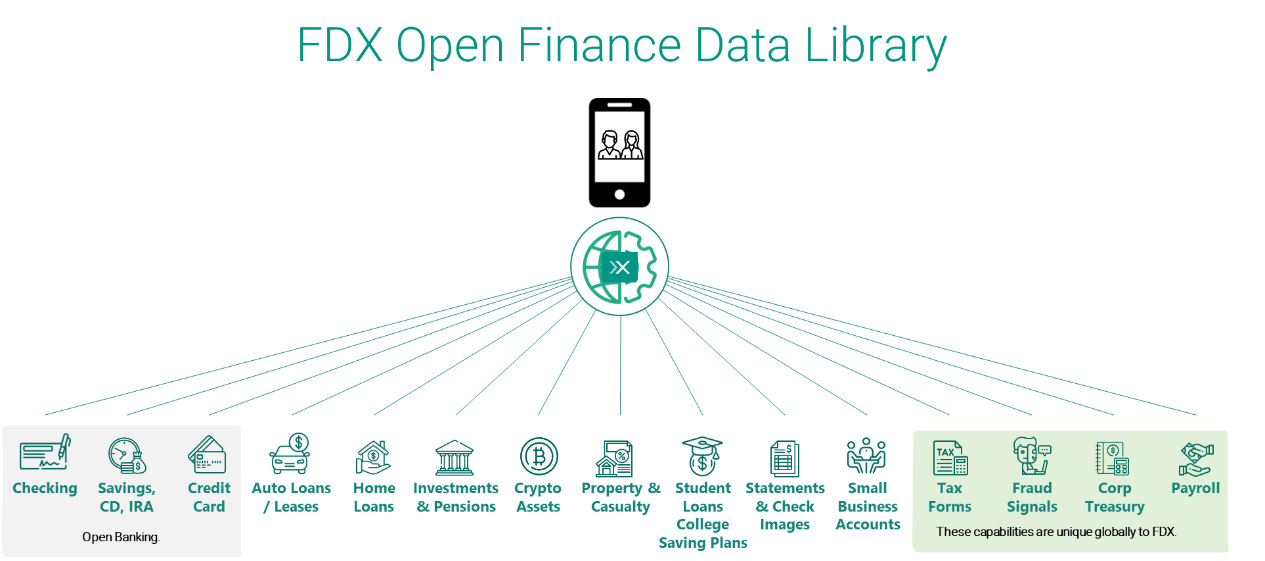

Much ink has been spilt on the topic of Open Banking, but I wanted to take a step today into a larger world of Open Finance. Whereas Open Banking is most commonly associated with current accounts (checking, savings, credit cards), Open Finance is concerned with the totality of your financial world.

While current accounts are important in the personal financial management use case, when you look at more sophisticated needs, liability accounts like auto loans, home loans, and student loans are required to help give context to a personal balance sheet. Finally, the addition of investment and retirement accounts gives the wealth management user a full 360-degree view of the consumer’s financial health.

Advertisement

Additional use cases – such as account and balance verification, bill payment, and payroll needs like verification of income/employment and pay stub retrieval – along with the ability to retrieve tax forms like W2, 1098, 1099, and capital gain statements for tax preparation, round out the most common consumer demands for linking accounts.

These are all important use cases for consumers and small businesses, but it is also important to address why data providers like banks, brokers, and others would benefit from data sharing.

We know that one in three digitally-enabled consumers has shared access to their financial data in the last year and similar polls of financial institutions tell us that at least one-third (if not more) of their online banking traffic was credential-based access (screen scraping) to power these use cases.

Imagine if a data provider could reduce one-third of its entire load on its online infrastructure in favour of a portal 100 times more efficient than screen scraping. The introduction of secure APIs does just that. Lowering costs of hardware overall.

One of the other uses by data providers is data-in, to pre-fill new account applications as well as provide strong signals for Know Your Customer (KYC), including account tenure at a predecessor institution. Better data means faster, more accurate decisions leading to fewer abandons or declines, meaning more revenue for the institution.

Advertisement

As a banker for a number of years, one of the biggest questions we had was ‘What was our share of a given customer’s wallet?’ We often had to try to infer based on monies in and out, but with Open Finance, you can link to other institutions and know in real time what your share of wallet is. This allows you to be almost surgical in your marketing and product offering.

All this is made possible by secure, permissioned data sharing via a common API standard.

Looking forward

Avoid FUD (fear, uncertainty, and doubt). Many jurisdictions have implemented Open Banking (the UK, EU, Australia, Brazil, among others) and there has yet to be a mass exodus of consumers in any of these nations. Why? If you are confident in your product, your pricing, and your service, making data available via an API does nothing to incent consumers to leave, rather the opposite. The largest credit union in Brazil said at the FDX Spring 2024 Summit that they saw a net increase in digital engagement and accounts per customer after Open Banking was introduced.

A last bit of advice: APIs are a net new channel and will be the third leg in the digital stool. Online, Mobile, and API will be the troika. APIs are much more efficient and can deliver data that cannot be displayed visually. As you make your plans for 2025 and 2026 for your digital roadmap, you would be remiss in not including Open Finance APIs in your product mix. Your competitors are.

This editorial piece was first published in The Paypers’ Open Finance Report 2024, the latest comprehensive market overview and analysis focusing on the key players and products within the Open Banking and Open Finance ecosystem. Download the full report to discover more insightful content.

Advertisement

About Don Cardinal

Don Cardinal is Managing Director of Financial Data Exchange (FDX) and has led it since its inception. Previously, he spent over 20 years with Bank of America, serving as head of digital for its Military Bank, VP of Digital Banking & Senior VP of Information Security. Don holds 18 US patents and CPA, CISA, CISM certificates.

About FDX

The Financial Data Exchange (FDX) is dedicated to unifying the financial industry around a common, interoperable, royalty-free standard for the secure and convenient access of permissioned consumer and business financial data: the FDX Application Programming Interface (FDX API). FDX is a global 501(c)(6) nonprofit organisation with no commercial interests operating in the US and Canada.

Don Cardinal is Managing Director of Financial Data Exchange (FDX) and has led it since its inception. Previously, he spent over 20 years with Bank of America, serving as head of digital for its Military Bank, VP of Digital Banking & Senior VP of Information Security. Don holds 18 US patents and CPA, CISA, CISM certificates.

Don Cardinal is Managing Director of Financial Data Exchange (FDX) and has led it since its inception. Previously, he spent over 20 years with Bank of America, serving as head of digital for its Military Bank, VP of Digital Banking & Senior VP of Information Security. Don holds 18 US patents and CPA, CISA, CISM certificates.

/cdn.vox-cdn.com/uploads/chorus_asset/file/25822586/STK169_ZUCKERBERG_MAGA_STKS491_CVIRGINIA_A.jpg "Meta is highlighting a splintering global approach to online speech")

/cdn.vox-cdn.com/uploads/chorus_asset/file/25821992/videoframe_720397.png "Las Vegas police release ChatGPT logs from the suspect in the Cybertruck explosion")

/cdn.vox-cdn.com/uploads/chorus_asset/file/23935558/acastro_STK103__01.jpg "Amazon Prime will shut down its clothing try-on program")