Business

Armed with venture capital, Skims and Kim Kardashian write their 'second chapter'

Kim Kardashian was already a successful celebrity businesswoman when she launched Skims five years ago.

But more often than not, she simply had attached her name to a string of existing companies: QuickTrim supplements, Carl’s Jr. salads, Skechers Shape-Ups, Sugar Factory confections, Midori liqueur, Silly Bandz bracelets, Beach Bunny swimwear, and so on.

“We did every product that you could imagine — from cupcake endorsements to a diet pill at the same time, to sneakers or things that I didn’t know enough about for them to be super-authentic to me,” the reality television star told The Times in 2019. “Like it all made sense a little bit, but it wasn’t my own brand.”

Skims, Kardashian’s homegrown apparel company built upon her famous curves and her love of body-cinching shapewear, was on brand — and, finally, her brand.

Kim Kardashian at a Skims pop-up at the Grove in 2021. The company pulled in nearly $1 billion in net sales last year and will open its first physical stores soon.

(Skims)

Its first years were marked by explosive growth. The start-up is now a retail juggernaut with around $1 billion in net sales and Kardashian has become a savvy entrepreneur with an eye for spotting and setting trends. Skims has made a huge dent in the shapewear market previously dominated by Spanx while adding several new categories to its merchandise mix.

This year Skims is aggressively moving into its next phase, one that will see the Hollywood company enter the competitive bricks-and-mortar space for the first time.

Underscoring Skims’ growth is the heightened interest the retailer is drawing from investors. Last year it raised $330 million in venture capital funding, ranking it second among companies in the greater L.A. area and the only retail brand in the top 10, according to a recent analysis by CB Insights.

That influx of cash was particularly notable given the tough investment climate locally: The region saw a steep decline in venture capital funding from 2021 to 2023, when the amount of investment dollars fell 74%, the analytics firm said.

Co-founded by Karadashian, who is chief creative officer, and Jens Grede, the company’s chief executive, Skims pulled in nearly $1 billion in net sales last year, according to Bloomberg, roughly double its 2022 total.

Kim Kardashian, center, in a Skims ad campaign starring Candice Swanepoel, Tyra Banks, Heidi Klum and Alessandra Ambrosio.

(Courtesy of Skims)

The company is reportedly eyeing an initial public offering this year. Kardashian and Grede declined to comment.

What began as a collection of undergarments designed to give women a more flattering, contoured silhouette has swelled into a comprehensive apparel giant: There’s underwear, bras, swimwear, dresses, tees and tanks, loungewear and pajamas. Inclusive sexy-meets-cozy clothing is the hook, with merchandise available in a wide range of sizes and skin tones.

In October, Skims launched a menswear line and became the official underwear partner of the NBA, WNBA and USA Basketball. It sells some accessories and clothing for kids, and this year will open bricks-and-mortar stores in several cities including a flagship location in Los Angeles.

“Skims has evolved into becoming a brand that can provide comfort for all audiences, not just for women,” Kardashian, 43, said when announcing the menswear line.

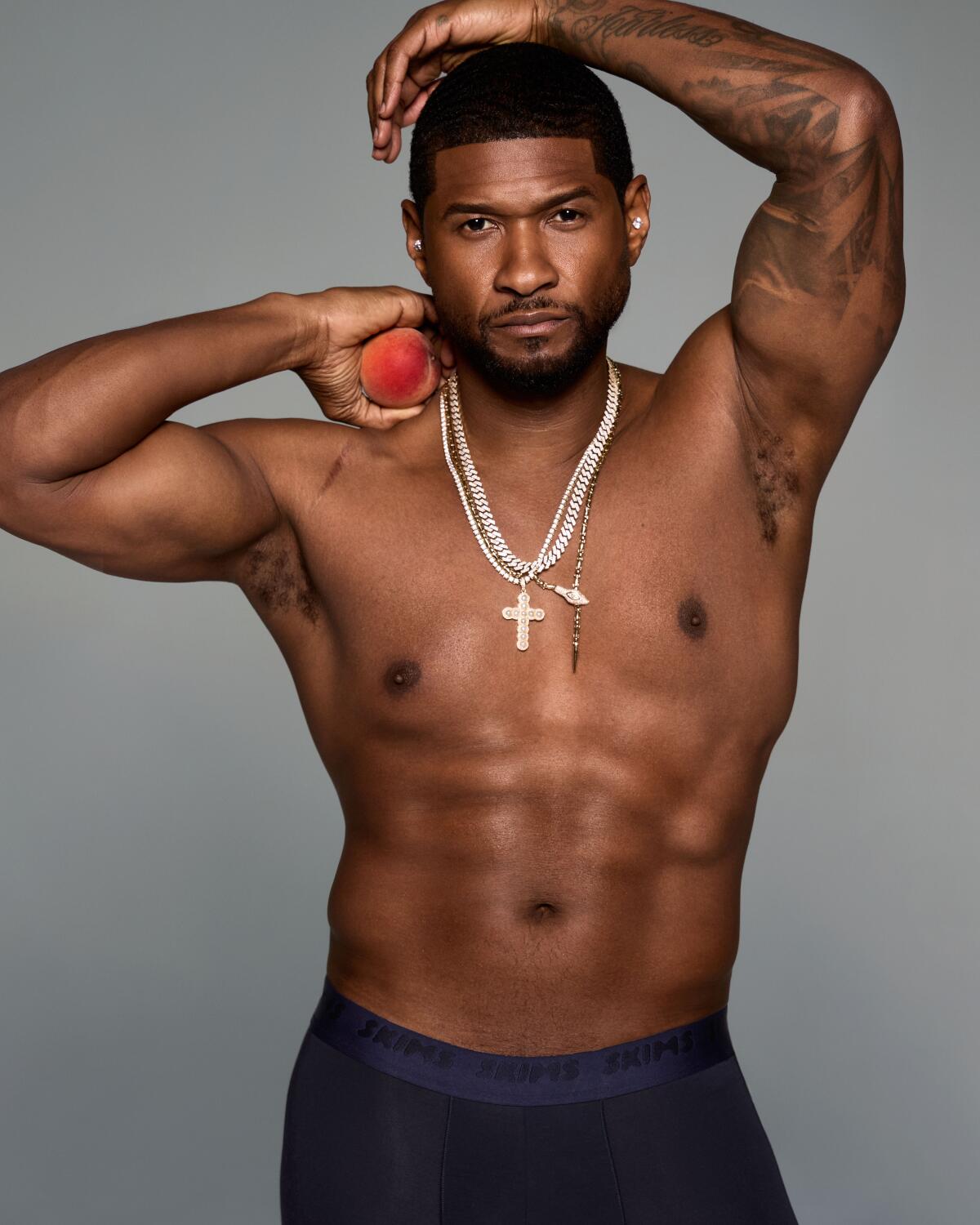

Usher in Skims. The brand launched menswear in October.

(Courtesy of Skims)

The company’s swift rise was undoubtedly fueled in part by Kardashian’s name and marketing prowess. She models the latest collections herself, posting glossy professional photos and casual at-home closet videos to her millions of social media followers, and has tapped her A-list friends to star in Skims ad campaigns including Lana Del Rey, Kate Moss, SZA, Cardi B, Sabrina Carpenter, Usher and Patrick Mahomes.

“Kim Kardashian’s visibility, I think, gives them a big leg up on marketing,” said Alex Lee, research editor at CB Insights, which compiled its data by analyzing companies in Los Angeles, Orange, Ventura, San Bernardino and Riverside counties.

But more than that, Lee said, Skims “is a really interesting example of the confluence of celebrity with technology and consumer trends.”

The rise of athleisure — stylish athletic clothing that can be worn at the gym or as everyday wear — was a game-changer in retail, said Simeon Siegel, managing director at BMO Capital Markets, who follows companies including Victoria’s Secret and Lululemon.

“That notion of comfort stretched to every possible category of apparel,” he said. “What we saw was a race among companies to figure out how to apply what Lulu revolutionized. Shapewear was a very logical category to go after with the new advancements in technology,” which includes improved fabrics and better fits.

Skims at first sold its products online only through its website before expanding to retailers including Nordstrom and Saks Fifth Avenue and hosting occasional pop-ups. Its foray into physical stores “marks the second chapter” for the company, Grede said in an interview with Bloomberg last year, and its ambitions are high.

Kim and I can envision a future where years from today there’s a Skims store anywhere in the world you’d find an Apple store or a Nike store.

— Jens Grede, Skims co-founder and CEO

In the fourth quarter, Skims is scheduled to open a 5,000-square-foot store on the Sunset Strip in West Hollywood. The company also plans to open stores in other U.S. cities and then target major international markets.

“Kim and I can envision a future where years from today there’s a Skims store anywhere in the world you’d find an Apple store or a Nike store,” Grede said.

Skims was most recently valued at $4 billion after a funding round last summer, a valuation that propelled Kardashian to sixth on Forbes’ list of the World’s Celebrity Billionaires 2024 with an estimated net worth of $1.7 billion.

“No one has cashed in on reality star fame more than Kim Kardashian, who has become a billionaire from her beauty and clothing brands,” the magazine said.

Disneyland Resort in Anaheim will offer $59 tickets for select evening admission to either theme park as part of a new promotion.

The one-day, one-park evening ticket offer will allow attendees to enter Disney California Adventure at 5 p.m. or Disneyland at 7 p.m. Park reservations are still required, as has been the case since the COVID-19 pandemic.

The offer only applies for admission from July 12 through Aug. 5 on Sundays to Wednesdays.

Disneyland Resort is commemorating its 70th anniversary through Aug. 9, and has introduced new shows and additions to rides as part of the occasion.

Walt Disney Co.’s theme parks and experiences business are a crucial boost to its finances, making up about 56% of the company’s operating income last fiscal year.

During the Burbank-based company’s most recent earnings call in May, Disney executives said attendance at its U.S.-based parks was down 1% compared with the prior year, a shift they attributed to “continued softness” in international visitations. However, the company said at the time that it was starting to move past those issues.

Disney’s experiences division reported $9.5 billion in revenue in that fiscal second quarter, up 7% compared with the same period a year ago, something executives said was due to higher guest spending domestically and more capacity on its cruise line.

An aging downtown office complex will be converted into apartments as part of an ambitious plan by local real estate companies to create 4,000 affordable housing units in Los Angeles.

The first project will be a $200-million makeover of the L.A. World Trade Center, a sprawling white elephant of an office complex on Figueroa Street built in the 1970s that will be turned into 512 apartments in one of the largest affordable housing conversions to date downtown.

Future projects being planned in the central city for delivery over the next five years will include other office-to-apartment conversions and new housing built from the ground up.

The 10-story World Trade Center, right, at Figueroa and Fourth streets in downtown Los Angeles, was built in the mid-1970s.

(Myung J. Chun / Los Angeles Times)

Behind the building campaign unveiled Monday are two of the region’s largest real estate companies, Jamison and Kennedy Wilson. Jamison is the city’s most prolific converter of offices to market-rate apartments and currently has a major makeover of a downtown office skyscraper underway for tenants who can pay top rents.

Kennedy Wilson, a real estate investment company based in Beverly Hills, owns Vintage Housing, which builds and operates affordable housing using tax credits and other state and federal financing to help fund it.

Vintage Housing and Jamison’s new affordable housing division, Arden Residential, will take on the campaign to build the housing where qualified tenants will pay rents below market rates.

Rents in the World Trade Center — which will be renamed Sky Castle when it opens in early 2028 — are expected to start at $937 for a one-bedroom unit. Some two- and three-bedroom units would rent for $1,100 and $1,300 per month, respectively, developers said.

Sky Castle will have shared amenities found in more expensive modern apartments, the developers said, such as a fitness center, resident lounge and co-working space. It already has six tennis courts on the roof, which may be converted to pickleball courts, Jamison Chief Executive Garrett Lee said.

The goal is to build higher quality affordable housing by using efficient construction methods Jamison has learned through building more than 8,000 market-rate apartments in the past, Lee said. The makeover of the World Trade Center will mark Jamison’s 15th conversion of an office building to housing.

The plan to redevelop the L.A. World Trade Center, bottom left, is one of the largest affordable housing conversions to date downtown.

(Myung J. Chun / Los Angeles Times)

The 10-story World Trade Center was built in the mid-1970s to fanfare saying it would be home to international companies. In 1976, The Times described the center as a place to prepare for an overseas trip where visitors could get passports and visas, as well as exchange dollars for francs, marks, rubles and other currency. There was a language school and branches of U.S., Swiss and Japanese banks.

By the mid-1980s, the 400,000-square-foot office complex covering a city block at Figueroa and Fourth streets had lost its international flavor and was falling out of favor with corporate tenants who were moving into glossy new skyscrapers on Bunker Hill and in other locations.

The building has been cleared of remaining office tenants to allow work to begin in August, Lee said.

Kennedy Wilson is a nationwide operator of market-rate apartments that has also moved into building affordable housing in the last decade, said Nicholas Bridges, global head of capital markets at the company.

Building affordable, workforce housing “in almost all cases requires public subsidies,” Bridges said, and Kennedy Wilson has developed expertise in assembling “a cocktail of public financing sources” that includes low-income housing tax credits and tax-exempt bonds.

In the past, many housing developers have shied away from building affordable housing because assembling the subsidies needed to make construction profitable is challenging.

An artist’s rendering shows what the L.A. World Trade Center could look like after being redeveloped into affordable housing. The new complex is to be called Sky Castle.

(Ian Camarillo)

“It’s complicated,” Bridges said, “and not for the faint of heart.”

Eligible tenants must earn between 30% and 80% of the median income in the area where the housing is built.

Jamison and Kennedy Wilson will develop about 15 affordable housing projects between downtown and the 405 Freeway, Bridges said, many of them in aging office buildings such as the World Trade Center that are already owned by Jamison and are close to public transit.

Substantial potential for affordable housing lies in L.A.’s underused office buildings, he said.

“In this post-COVID world, the way people are utilizing office buildings, particularly older office buildings, has just fundamentally changed,” he said.

It makes sense for developers of conventional multifamily housing to move to building affordable housing, Lee said, because the government supports it through subsidies, zoning reform and the fast-tracking of construction permits. The city of Los Angeles also recently streamlined its adaptive reuse rules to make it easier to convert office buildings to housing.

“There are a lot of incentives pushing us in this direction,” Lee said.

Comcast is spinning off its NBCUniversal entertainment and news media businesses into a separate publicly traded company, a move that would unwind an audacious play the cable giant made for the storied Hollywood assets 15 years ago.

The plan would put broadcast networks NBC and Telemundo, NBC News, cable network Bravo, streaming service Peacock, the Los Angeles-based Universal film and television studios, Universal theme parks and British TV service Sky in a new stand-alone company.

Philadelphia-based Comcast would remain in its core business of distributing pay-TV channels, broadband internet and wireless services.

The spinoff would be the second such move by Comcast in two years. Late last year, the Brian L. Roberts-controlled company cast off most of its cable portfolio, including CNBC, USA Network, MS NOW and Golf Channel to form a new entity called Versant.

But the maneuver failed to budge Comcast’s listless stock, which has languished for years as its primary business lost thousands of broadband customers.

Comcast executives needed to make a bolder move to mollify frustrated investors.

Comcast stock peaked at nearly $26 per share Monday before closing at $24.22, up roughly 4.5% from Friday. Still, the stock remains below its 52-week high of $34.34.

The plan announced Monday would unravel Comcast’s bold decision to acquire NBCUniversal from General Electric Co. in 2011. At the time, Comcast saw tremendous value in marrying NBC’s entertainment operations, including its then-lucrative cable channels, with its cable TV distribution service that Roberts’ late father, Ralph, launched in Tupelo, Miss., in 1963.

“They were two distinct businesses,” longtime cable analyst Craig Moffett wrote in a Monday note to investors. “Having them under the same roof didn’t make either better.”

Consumers shifted to streaming, and Comcast’s attempt to build a top-tier digital service, Peacock, has fallen well short of its goal. Peacock lags behind rivals despite billions of dollars in investment from Comcast.

The concept of unwinding its NBCUniversal operation began in earnest in the fall, when Comcast joined the bidding for Warner Bros. Discovery. Comcast executives knew they could ill afford to spend billions to buy a rival; Wall Street would have pummeled the company.

So Comcast offered to spin off NBCUniversal and pair it with Warner Bros., turning two original Hollywood studios into a new media colossus.

But 43-year-old billionaire David Ellison prevailed in the bidding, agreeing to pay $111 billion to capture Warner Bros. Discovery. Losing the auction forced Comcast to find a different path forward.

On a call with investors, Roberts said the separation would bolster the two firms as they navigate increasing competitive challenges while technology companies continue to transform entertainment.

“We asked ourselves three basic questions,” Roberts said. “One, can these businesses stand alone and have the heft to stand alone in separate companies? Two, do they have a clear, viable capital allocation path to invest? And three, is now the right time? And the answer we came back with was yes to all counts.”

A free-standing NBCUniversal, home of the “Minions” and “Jurassic Park” franchises, probably would be an acquisition target, as media companies have been consolidating in an effort to get more content and mass distribution for their streaming services. Ellison’s Paramount is on track to close its Warner Bros. purchase, which would combine such media assets as HBO Max, CBS, CNN, Paramount Pictures and Warner Bros. studios.

With its Sky business, NBCUniversal has a toehold in Britain and Europe at a time when Amazon and Netflix are flexing their global distribution muscles.

Comcast would be positioned to combine with another cable and internet provider, such as Connecticut-based Charter, which owns the Spectrum television service. Charter is in the process of buying the smaller Cox cable service, which also has operations in Southern California.

Comcast is expected to complete the spinoff next year and will retain an 19% stake in the new entity.

The timetable could put NBCUniversal up for grabs by 2028 — when the company is set to broadcast the Summer Olympics, which will be held in Los Angeles.

Comcast acquired NBCUniversal in 2011. The industry-reshaping deal combined the largest distributor of TV channels with a provider of top-rated TV channels and a movie studio. But the streaming revolution has decimated the cable television business. Traditional TV viewing has been in a steady decline over the last decade. NBC has relied heavily on NFL broadcasts, and more recently, NBA and Major League Baseball games to remain relevant.

NBCUniversal has invested heavily in its streaming service, Peacock, but has been unable to reach the scale necessary for profitability. Comcast‘s stock price has struggled as a result.

Roberts, chairman and chief executive of Comcast, will continue to be involved in the leadership of Comcast and NBCUniversal, working in partnership with the CEOs of both companies.

Mike Cavanagh will remain as CEO of NBCUniversal, and Comcast’s former chief financial officer, Michael Angelakis, will return to run Comcast after the spinoff.

“Perhaps the best part of today’s welcome announcement … is that Mike Angelakis is coming back,” Moffett, the analyst, wrote. “He will now helm the cable business, [which] is unequivocally good news. With Mike Angelakis’s return, Comcast has come full circle.”

Moffett added that, despite Monday’s announcement, the 2011 combination was not a complete bust.

“The deal to acquire NBCU from GE was financially brilliant,” he said. “It was structured so that Comcast paid for just half of the acquisition and then let NBCU’s own cash flow pay for the rest.”

Over the years, Comcast has raked in billions in profit from its media holdings.

Comcast executives on the analyst call played down the notion that the two companies were being positioned for another deal.

“Absolutely not,” Roberts said. “This is the right move to put each company in the strongest position to create value, fully monetize its assets and aggressively pursue its own organic growth strategies.”

Cavanaugh, who has been running the combined company for three years, sounded more like a buyer than a seller.

“Our plan for NBCUniversal and Sky is to build and invest for growth,” he said. “We have the freedom now to explore adjacent businesses where we have the right to play, and that’s thanks to the stability of our company and management team.”

The spinoff announcement comes a week after Fox Corp. announced its deal to purchase the streaming platform Roku for $22 billion. The deal is aimed at ensuring that Fox has a means to get its portfolio of sports, news and entertainment channels into viewers’ homes as the traditional pay-TV business continues to erode.

-

Nebraska5 minutes ago

Nebraska5 minutes agoErstad joins Nebraska golf program

-

Nevada8 minutes ago

Nevada8 minutes ago‘Arrive Alive’ initiative with Nevada Department of Public Safety, FOX5

-

New Hampshire13 minutes ago

New Hampshire13 minutes agoThis NH Short Film Festival Returns in July, and Every Film Clocks in at 15 Minutes or Less

-

New Jersey20 minutes ago

New Jersey20 minutes agoNew Jersey’s $60.7 billion budget signed into law by Gov. Mikie Sherrill • The Jersey Vindicator

-

New Mexico23 minutes ago

New Mexico23 minutes agoCommunity Champions: New Mexico’s Flo Valdez inducted into NFHS

-

North Carolina28 minutes ago

North Carolina28 minutes agoNorth Carolina mail carrier kidnapped and killed while on her route, authorities say

-

North Dakota35 minutes ago

North Dakota35 minutes agoJune ND severe weather recap: 5 tornadoes, damaging winds impact numerous towns

-

Ohio38 minutes ago

Ohio38 minutes ago‘Pure evil’: Adults arrested after 16 children found in deplorable conditions in Ohio home