Finance

PODCAST | Adapting to change: The future of factoring and supply chain finance

Estimated reading time: 5 minutes

Listen to this podcast on Spotify, Apple Podcasts, Podbean, Podtail, ListenNotes, TuneIn

The volatility of the geopolitical and macroeconomic environment in recent years has caused some problems in the trade, treasury, and payments industries.

However, industry actors have adapted and are working together to build resilience and make international trade even stronger.

To hear about developments in the factoring and supply chain finance world, Trade Finance Global (TFG) spoke with Çağatay Baydar, Chairman at FCI and Irina Tyan, Principal Banker, TFP at the European Bank for Reconstruction and Development (EBRD).

Challenges and growth in the factoring industry

The factoring industry has demonstrated impressive growth since the turn of the century despite facing significant challenges, particularly in emerging markets.

Baydar said, “The growth rate in 2023 was 3.3% globally in the volume of the world factoring and in 2022 it was 18%. Over the last 20 years, the average growth rate has been 8% which shows that factoring is becoming a mainstream financial product globally, which is very good indeed.”

The sector, which revolves around the purchase of receivables from businesses to provide them with immediate liquidity, has become an essential component of global trade finance, but it also faces challenges. One of the primary challenges is the bureaucratic and infrastructural limitations inherent in the current system.

Factoring, being an invoice-based product, requires a significant amount of paperwork and documentation, which can be cumbersome and traditionally relies on a paper-based system that only adds to the administrative burden for businesses.

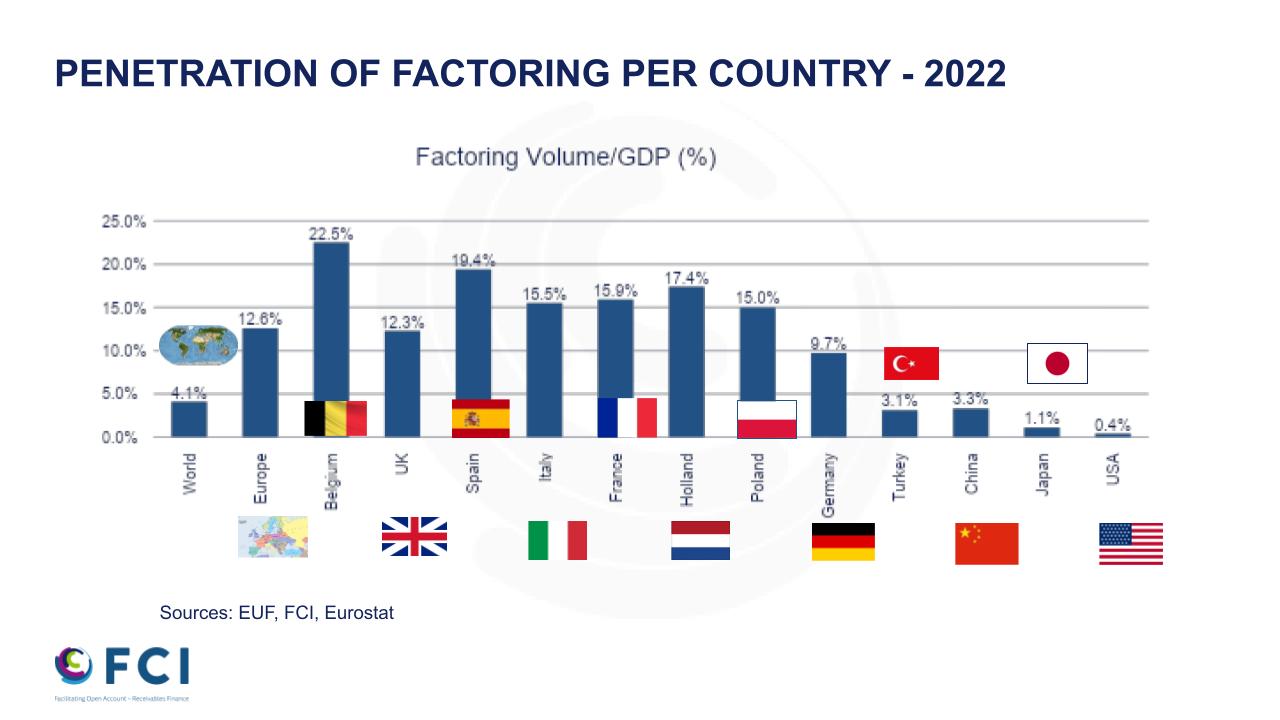

In developed regions like Europe, factoring’s penetration rate – a measure of the amount of trade volume that uses factoring – is around 15%, reflecting a more mature understanding and use of this financial product. By contrast, in emerging markets, the penetration rate is significantly lower, with countries like Turkey and Georgia showing rates as low as 3%.

This discrepancy highlights the knowledge gap and infrastructural deficiencies in these regions. Businesses in these markets often lack the necessary awareness and understanding of factoring, which limits their ability to leverage this financial tool to its full potential.

However, factoring usage in some emerging markets is growing.

Tyan said, “We see the progress in the countries where we started five to seven years ago, like Georgia. We recently had a workshop in Jordan, where we also see a more adapted market, more ready to look into this type of product.”

Further collaboration and efforts to promote regulatory reforms and technological advancements may be what is needed to drive factoring growth in these underutilised regions.

Regulatory reforms and technological integration

Regulatory reforms are crucial for the sustained growth and development of the factoring industry, and legal clarity is particularly important in emerging markets, where the absence of a well-defined regulatory environment can pose significant barriers to factoring’s growth.

One of the key areas that require attention is the standardisation of data exchange formats.

Creating common data standards for supply chain transactions can facilitate smoother integration between different platforms and financial institutions, improving efficiency, reducing administrative burdens, and enhancing the overall effectiveness of the factoring process.

Another important aspect of regulatory reform is cybersecurity.

Tyan said, “As this product heavily relies on platforms, clear regulation on data security and cybersecurity is crucial to build trust among the participants.”

Ensuring the integrity and security of transactions protects sensitive financial information from potential cyber threats and is vital for the long-term sustainability and credibility of the industry.

Digitalising to draw clients and talent to factor

The factoring industry has been significantly transformed by the integration of digital technologies that have made the process faster, more efficient, and more accessible, especially for small and medium-sized enterprises (SMEs).

Traditionally, the paperwork involved in factoring, particularly for international transactions, slowed down the process and added to its complexity but digital platforms are allowing for quicker access to funds and improving the overall client experience.

Baydar said, “Today, with digitalisation and the platforms, we are making our business much faster, quicker, and more effective. This really helps SMEs to touch the money very soon, very quickly. This makes our clients happier than before because they can experience a very fast, very effective, seamless transaction.”

This shift not only speeds up transactions but also minimises the risk of errors and fraud associated with manual paperwork and can help attract more young professionals to the industry.

Baydar said, “Young people prefer to work with new technology and high-level startup businesses rather than traditional models.”

The new generation of workers is drawn to innovation and technologically advanced sectors. By embracing digital advancements, the factoring industry can position itself as a forward-thinking and dynamic field, appealing to young talent looking for exciting career opportunities. This influx of new talent is essential for sustaining the industry’s growth and development in the long term.

Organisations that fail to embrace digitalisation risk being left behind in a rapidly evolving market, meaning that investing in digital solutions is not just an option but a necessity for the future of the factoring industry.

What if the global financial system could move at the speed of the internet unlocking trillions in value while expanding access to capital worldwide?

Developed in collaboration with Dante Disparte, Chief Strategy Officer and Head of Global Policy & Operations at Circle; Fred Thiel, Chairman and Chief Executive Officer of MARA, Inc.; and Ryan Hayward, Head of Digital Assets and Strategic Investments at Barclays, this report on digital assets and tokenized finance reveals how a rapidly emerging $16–30 trillion market is transforming traditional finance into a real-time, programmable, and borderless ecosystem.

It explores how the tokenization of real-world assets, the explosive growth of stablecoins processing over $30 trillion annually, and instant (T+0) settlement are redefining liquidity, reducing cross-border costs, and reshaping global investment flows. The report also highlights the critical role of financial inclusion, addressing a $330 billion SME financing gap alongside the rise of AI-driven transactions, energy-powered infrastructure, and evolving regulation that will ultimately determine who leads and who benefits in the next era of finance.

Brent crude (BZ=F) and West Texas Intermediate (CL=F) futures contracts marched higher on Tuesday morning, having plummeted more than 10% at one point in Monday’s trading session. Questions continue to swirl around the potential reopening of the Strait of Hormuz and an end to the conflict between Iran and the US and Israel.

Brent crude (BZ=F) gained 1.7% after the opening bell in London, to around the $97.50 per barrel mark. West Texas Intermediate (CL=F) also rose 1.7% to $89.55 per barrel.

The moves come amid conflicting reports about talks between Iran and the US to end fighting. On Monday, president Donald Trump delayed strikes on Iranian power plants, having given Iran a deadline to restore trade through the Strait of Hormuz, saying Washington had productive conversations with Tehran.

But Tehran has since denied that it has been in touch with US negotiators, accusing Washington of price manipulation.

On Sunday night, Trump and prime minister Keir Starmer held a 20-minute phone call about the situation.

“They agreed that reopening the Strait of Hormuz was essential to ensure stability in the global energy market,” a Downing Street spokesperson said.

On Saturday, Trump gave Iran a 48-hour deadline to reopen the Strait — a measure set to expire shortly before midnight UK time on Monday.

In a Truth Social post, Trump wrote: “If Iran doesn’t FULLY OPEN, WITHOUT THREAT, the Strait of Hormuz, within 48 hours from this exact point in time, the United States of America will hit and obliterate their various POWER PLANTS, STARTING WITH THE BIGGEST ONE FIRST!”

Yesterday, Iran’s defence council said in a statement that the “only way for non-hostile countries” to pass through Strait of Hormuz is “coordination with Iran”.

Finance

Iran issues its largest-ever currency denomination as accelerating inflation ravages a financial sector deemed a ‘Ponzi scheme’ even before the war | Fortune

Iran’s economy was already crashing before the U.S. and Israel launched a war against the Islamic republic three weeks ago, and the relentless bombing since then has wreaked even more havoc.

In fact, high inflation triggered mass protests in December and January, prompting the regime to massacre tens of thousands of its own citizens. President Donald Trump warned Tehran against further violence and began a military build-up that led to the current conflict.

Inflation has worsened and apparently is so bad now the government issued its largest-ever currency denomination: the 10 million rial note (equivalent to about $7).

The new currency went into circulation last week, according to the Financial Times, and comes just a month after the prior record holder, the 5 million rial, came out.

As prices continue to spiral higher while the war boosts demand for cash, long lines formed to withdraw the fresh banknotes, and supplies quickly ran out.

Iran’s central bank said electronic payments are still the main methods for transactions, though the 10 million rial bill will “ensure public access to cash,” the FT reported.

But doubts about the viability of electronic payments have grown during the war as the U.S. and Israel target the regime’s levers of control.

In addition to bombing Islamic Revolutionary Guard Corps and Basij paramilitary forces, a data center for Bank Sepah was also hit on March 11. Sepah is the country’s largest bank and is responsible for paying salaries to the military and IRGC.

“Iran is already in the middle of a severe cash liquidity crisis,” Miad Maleki, a senior advisor at the Foundation for Defense of Democracies and a former Treasury Department official, said on X earlier this month. “As of Jan 2026, banks were running out of physical banknotes daily, with informal withdrawal caps of just $18–$30/day. Cash in circulation surged 49% YoY due to panic hoarding. The regime simply cannot pivot to cash payments, there isn’t enough physical currency in the system.”

Meanwhile, a currency collapse that began after last year’s U.S.-Israeli bombardment has fueled crippling inflation. The rial lost 60% of its value in the months after the 12-day war, and food inflation soared to 64% by October. It accelerated further to 105% by February, vaulting overall inflation to 47.5%.

The exchange rate fell as low as 1.66 million rials per $1 last month, though it strengthened to about 1.5 million rials as the U.S. temporarily lifted sanctions on Iranian oil.

Heightened demand for cash further stresses a financial system that was considered dubious even before the current war started three weeks ago.

The failure of Ayandeh Bank late last year forced the regime to fold it into a state-run lender, underscoring how fragile the sector was as bad loans piled up to politically connected cronies.

“This was largely theater. In reality, Iran’s entire banking system is insolvent, its balance sheets sustained by fiction rather than assets,” Siamak Namazi, who was a U.S. hostage in Iran from 2015 to 2023, wrote in a report for the Middle East Institute in January.

During his captivity, he learned from imprisoned former officials and business elites that politically connected borrowers bribed assessors to inflate the value of properties, which were used to obtain massive loans.

Instead of repaying the loans, borrowers just gave their properties to the bank, which sold them to other banks at a paper profit, according to Namazi. Those banks knew the properties were overvalued “garbage,” but played along in the scheme by dumping their own toxic assets in exchange and booking fictitious gains.

“The result is a closed-loop Ponzi scheme, sustained by mutual deception and regulatory complicity,” he added. “This practice has metastasized over the past 15 years and is far more extensive than this simplified description suggests. And this is only the banking system. Much of the rest of Iran’s economy is afflicted by similarly entrenched corruption and mismanagement.”

US military sends drones, alongside 200 troops, to Nigeria amid fears of renewed Boko Haram insurgency

Chicago alderwoman apologizes for ‘wrong place at the wrong time’ comment on slain student

Greater weight loss promised by higher-dose Wegovy shot, now approved by FDA

Rams star Puka Nacua accused of biting woman, making antisemitic remarks: report

If someone gets into your email, they own every account you have. These 3 moves lock them out for good

Florida High School Football Rankings: Top 25 teams – Oct. 21

How old is Bo Nix? What to know about Oregon quarterback ahead of 2024 NFL Draft

Cleary's 21 help Le Moyne down Central Connecticut State 69-64 in OT

99th annual Pony Swim held in Virginia

Indiana Members Credit Union announced as new anchor tenant at Bottleworks District

Chicago alderwoman apologizes for ‘wrong place at the wrong time’ comment on slain student

Fake Euronews website targets Hungary election with false claims

An air traffic controller was juggling extra roles during the LaGuardia plane crash

Iran War: Pentagon set to send thousands of elite 82nd Airborne troops to region | BBC News

Video: Passengers Wait in Long Security Lines at LaGuardia After Deadly Crash

-

Detroit, MI6 days ago

Detroit, MI6 days agoDrummer Brian Pastoria, longtime Detroit music advocate, dies at 68

-

Georgia1 week ago

Georgia1 week agoHow ICE plans for a detention warehouse pushed a Georgia town to fight back | CNN Politics

-

Movie Reviews6 days ago

Movie Reviews6 days ago‘Youth’ Twitter review: Ken Karunaas impresses audiences; Suraj Venjaramoodu adds charm; music wins praise | – The Times of India

-

Alaska1 week ago

Alaska1 week agoPolice looking for man considered ‘armed and dangerous’

-

Education1 week ago

Education1 week agoVideo: Turning Point USA Clubs Expand to High Schools Across America

-

Sports4 days ago

Sports4 days agoIOC addresses execution of 19-year-old Iranian wrestler Saleh Mohammadi

-

Science1 week ago

Science1 week agoIndustrial chemicals have reached the middle of the oceans, new study shows

-

New Mexico2 days ago

New Mexico2 days agoClovis shooting leaves one dead, four injured