Finance

PODCAST | Adapting to change: The future of factoring and supply chain finance

Estimated reading time: 5 minutes

Listen to this podcast on Spotify, Apple Podcasts, Podbean, Podtail, ListenNotes, TuneIn

The volatility of the geopolitical and macroeconomic environment in recent years has caused some problems in the trade, treasury, and payments industries.

However, industry actors have adapted and are working together to build resilience and make international trade even stronger.

To hear about developments in the factoring and supply chain finance world, Trade Finance Global (TFG) spoke with Çağatay Baydar, Chairman at FCI and Irina Tyan, Principal Banker, TFP at the European Bank for Reconstruction and Development (EBRD).

Challenges and growth in the factoring industry

The factoring industry has demonstrated impressive growth since the turn of the century despite facing significant challenges, particularly in emerging markets.

Baydar said, “The growth rate in 2023 was 3.3% globally in the volume of the world factoring and in 2022 it was 18%. Over the last 20 years, the average growth rate has been 8% which shows that factoring is becoming a mainstream financial product globally, which is very good indeed.”

The sector, which revolves around the purchase of receivables from businesses to provide them with immediate liquidity, has become an essential component of global trade finance, but it also faces challenges. One of the primary challenges is the bureaucratic and infrastructural limitations inherent in the current system.

Factoring, being an invoice-based product, requires a significant amount of paperwork and documentation, which can be cumbersome and traditionally relies on a paper-based system that only adds to the administrative burden for businesses.

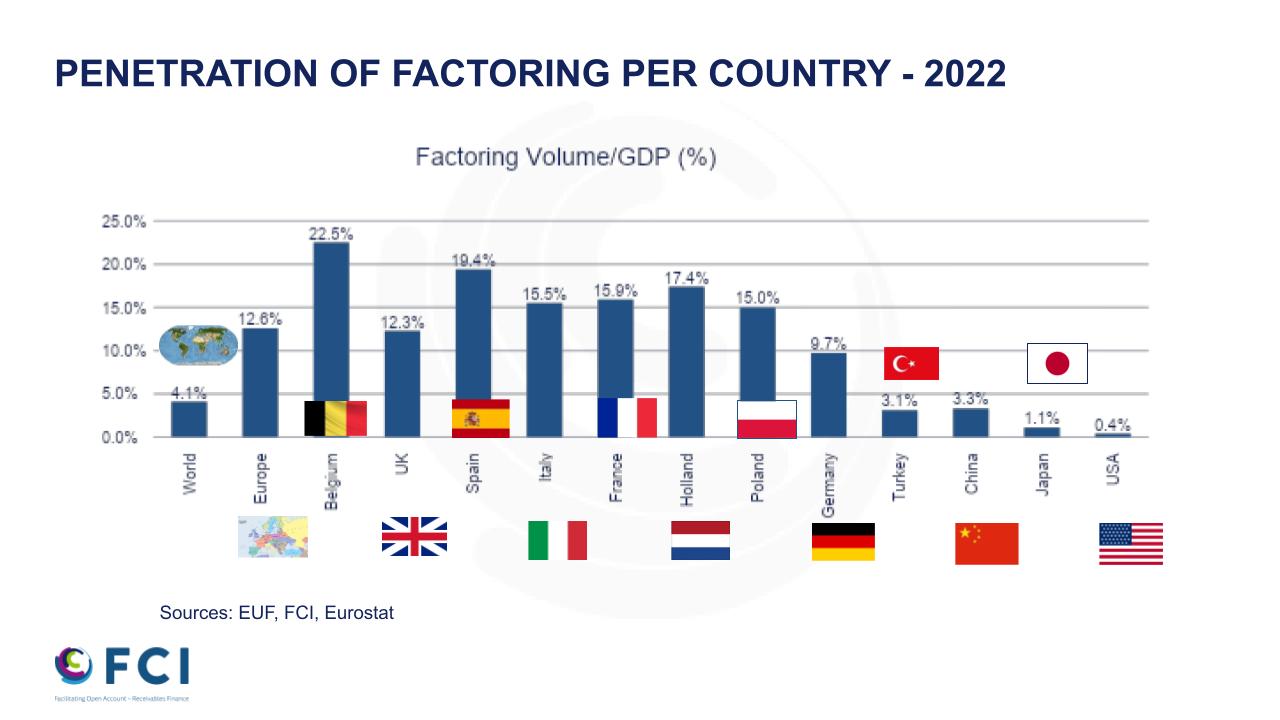

In developed regions like Europe, factoring’s penetration rate – a measure of the amount of trade volume that uses factoring – is around 15%, reflecting a more mature understanding and use of this financial product. By contrast, in emerging markets, the penetration rate is significantly lower, with countries like Turkey and Georgia showing rates as low as 3%.

This discrepancy highlights the knowledge gap and infrastructural deficiencies in these regions. Businesses in these markets often lack the necessary awareness and understanding of factoring, which limits their ability to leverage this financial tool to its full potential.

However, factoring usage in some emerging markets is growing.

Tyan said, “We see the progress in the countries where we started five to seven years ago, like Georgia. We recently had a workshop in Jordan, where we also see a more adapted market, more ready to look into this type of product.”

Further collaboration and efforts to promote regulatory reforms and technological advancements may be what is needed to drive factoring growth in these underutilised regions.

Regulatory reforms and technological integration

Regulatory reforms are crucial for the sustained growth and development of the factoring industry, and legal clarity is particularly important in emerging markets, where the absence of a well-defined regulatory environment can pose significant barriers to factoring’s growth.

One of the key areas that require attention is the standardisation of data exchange formats.

Creating common data standards for supply chain transactions can facilitate smoother integration between different platforms and financial institutions, improving efficiency, reducing administrative burdens, and enhancing the overall effectiveness of the factoring process.

Another important aspect of regulatory reform is cybersecurity.

Tyan said, “As this product heavily relies on platforms, clear regulation on data security and cybersecurity is crucial to build trust among the participants.”

Ensuring the integrity and security of transactions protects sensitive financial information from potential cyber threats and is vital for the long-term sustainability and credibility of the industry.

Digitalising to draw clients and talent to factor

The factoring industry has been significantly transformed by the integration of digital technologies that have made the process faster, more efficient, and more accessible, especially for small and medium-sized enterprises (SMEs).

Traditionally, the paperwork involved in factoring, particularly for international transactions, slowed down the process and added to its complexity but digital platforms are allowing for quicker access to funds and improving the overall client experience.

Baydar said, “Today, with digitalisation and the platforms, we are making our business much faster, quicker, and more effective. This really helps SMEs to touch the money very soon, very quickly. This makes our clients happier than before because they can experience a very fast, very effective, seamless transaction.”

This shift not only speeds up transactions but also minimises the risk of errors and fraud associated with manual paperwork and can help attract more young professionals to the industry.

Baydar said, “Young people prefer to work with new technology and high-level startup businesses rather than traditional models.”

The new generation of workers is drawn to innovation and technologically advanced sectors. By embracing digital advancements, the factoring industry can position itself as a forward-thinking and dynamic field, appealing to young talent looking for exciting career opportunities. This influx of new talent is essential for sustaining the industry’s growth and development in the long term.

Organisations that fail to embrace digitalisation risk being left behind in a rapidly evolving market, meaning that investing in digital solutions is not just an option but a necessity for the future of the factoring industry.

The Senate Finance Committee is set to hear from a panel of Treasury nominees that includes a pick Democrats said was unaware of economic fallout planning ahead of the Iran war and a former executive at Secretary Scott Bessent’s hedge fund.

The July 16 confirmation includes George McMaster, who was the trading chief at Key Square Group, a macro hedge fund run by Bessent, and Sriprakash Kothari, whose behind-the-scenes answers to the panel during the vetting process raised red flags for ranking member Ron Wyden (D-Ore.).

Finance Chair Mike Crapo (R-Idaho) announced Thursday the panel will consider McMaster and Kothari …

Author: Leonardo Aguilera, CEO, Banreservas

Banreservas’ international expansion strategy is centred on strengthening economic ties with the Dominican diaspora as a strategic economic partner, rather than just operating as a full retail bank abroad, and the bank has successfully used mortgage fairs as part of this expansion strategy. These client-centric engagement events bring together diaspora clients, credible Dominican real estate developers, fiduciary-backed projects and bank representatives in one venue to help address key diaspora challenges such as distance and lack of trusted intermediaries, legal and documentation uncertainty, difficulty assessing projects remotely and limited access to tailored financing.

By simplifying the sending process from the US and Europe, reducing operational friction, and offering greater convenience and security, Banreservas has incentivised increased use of formal remittance channels. This strategy has had, and is expected to continue to have, a highly positive impact on remittance flows to the Dominican Republic, both in terms of volume and formalisation.

Reimagining the diaspora relationship

Banreservas’ model relies on representative offices set in strategic cities to provide advisory, pre-qualification and customer support services, while the financing and account opening itself is referred to Banreservas in the Dominican Republic, where they are operatively managed and booked.

The US (New York and Miami) and Spain (Madrid) were chosen as priority hubs to channel diaspora engagement and long-term investment because they are home to some of the largest and most economically active Dominican communities worldwide. By establishing representative offices in these strategic locations, Banreservas delivers tailored financial services to historically underserved expatriate communities, enabling them to invest, save, and build wealth in the Dominican Republic while contributing to national economic development, unlocking sustainable growth opportunities and deepening its role as a financial bridge between Dominicans abroad and their home country.

Banreservas uses mortgage fairs to compress what is traditionally a long, fragmented cross‑border process into a single, guided experience that combines education, advisory, and support. Diaspora clients can receive on-the-spot pre-qualification, explore real estate projects nationwide, and receive information and guidance about loan processes, although final approvals and disbursements are processed in the Dominican Republic.

The response in the US and Madrid has been characterised by sustained momentum and the diversity of participant profiles, from first-time buyers to repeat investors and returning nationals, which suggests that the fairs are resonating beyond a narrow segment of the diaspora. In US cities with long-established Dominican communities, the fairs have evolved into anticipated events rather than exploratory initiatives, with those in New York and Lawrence generating financing exceeding $49m. However, the initiative was newer in Europe, so the response in Madrid followed a slightly different trajectory, with early editions focusing heavily on education and orientation. That said, the first fair in Madrid attracted thousands of participants and closed with financing requests of more than $21m.

Risk mitigation is central to the model and projects are carefully vetted, many supported under a fiduciary account or an estate asset trust fund and backed by clear legal frameworks. Banreservas’ direct involvement is one of the defining features of its diaspora strategy to ensure transparency, regulatory compliance and investor protection throughout the process. By offering direct access to Banreservas’ experts, vetted developers, fiduciary-backed projects and consistent financing terms, these events are helping create a relationship-building platform that improves transparency, credibility and institutional confidence. Internal customer experience reports emphasise that word-of-mouth referrals, repeat attendance, and post-fair engagement are among the clearest indicators that trust has been established organically, particularly within close-knit diaspora communities. Banreservas’ role as the national leading institution further reassures clients investing from abroad.

Transaction to transformation

Rather than a single-product offering, Banreservas approaches diaspora customers with a portfolio mindset, providing a robust cross-border selection including mortgage loans, savings and checking accounts, remittance-linked products and investment solutions tied to real estate development.

Banreservas has deliberately adopted a scalable and selective expansion logic

Remittances are a core strategic pillar of Banreservas’ international expansion, and the creation of new digital channels and specialised financial products are helping transform remittances into a gateway for deepening financial inclusion. The Remesas Reservas app enables Dominicans abroad to send money from the US and Europe using international cards, with funds credited directly to bank accounts or debit cards in the Dominican Republic, eliminating the need for cash, queues, or physical travel. The app is complemented by the home delivery remittances service, which extends financial access to rural communities that were previously excluded from the formal financial system. Service performance data shows that 97 percent of remittances sent through the app complete the entire process digitally, while 94 percent are received directly in bank accounts, strengthening financial traceability. This supports the sustainability and potential growth of remittance inflows to the Dominican Republic that already exceeds $12bn annually, while also expanding the banked customer base and improving the overall efficiency of the national financial ecosystem.

The strategy is further strengthened by the introduction of remittance-based consumer and mortgage loans, specifically designed for remittance recipients. These products allow recurring remittance flows to be converted into formal financial history, facilitating access to credit, and reinforcing the ‘bankarisation’ process. As a result, remittances evolve from a basic transfer mechanism into a financial development tool, integrating beneficiaries into the banking system with solutions tailored to their real income patterns and needs.

Mortgage financing in the Dominican Republic is embedded within a broader set of banking solutions designed to support the full investment and ownership journey. At the core are residential mortgage products structured for non-resident clients looking to acquire property in the Dominican Republic. These are complemented by linked deposit and savings accounts, which allow clients to organise funds, manage payments and maintain an ongoing banking relationship once the purchase process begins. In parallel, Banreservas leverages its digital channels and remittance services to facilitate the movement of funds and day-to-day interaction with Banreservas, reinforcing continuity beyond the initial transaction.

For first-time diaspora investors, the emphasis is on financial orientation and readiness with solutions structured to simplify entry into the formal mortgage system in the Dominican Republic. For returning nationals, products and advisory conversations are typically aligned with reintegration objectives. In both cases, the underlying principle is adaptability within a controlled institutional framework, rather than bespoke products that introduce additional risk.

They have the support of President Luis Abinader, who has created the conditions for Dominicans in the diaspora take advantage of the macroeconomic stability, legal security, and full guarantees that receive all foreign investors who trust in the Dominican Republic to make their business.

Modernising remittance ecosystem

Modernising the remittance ecosystem combined with specialised financial products generates a direct multiplier effect on strategic sectors, strengthening the real economy and territorial development. In the construction sector, the remittance mortgage loan transforms recurring remittance flows into formal financing capacity for homeownership and has taken centre stage in Banreservas’ participation in international mortgage fairs. Diaspora demand supports property acquisition and upstream activities such as project development, construction services, materials supply, legal services and professional employment.

Equally important is the impact on financial deepening and formalisation. When diaspora investors enter the banking system through regulated mortgage channels, their participation strengthens the use of formal financial products, thereby expanding the reach and resilience of the financial system. This dynamic is a key contribution to economic maturity, as it encourages long-term financial relationships rather than one-time transactions.

From a tourism perspective, the strategy strengthens the economic and emotional ties between the diaspora and the country. Home purchases financed through mortgage loans paid via remittances promote more frequent visits, longer stays, and increased spending on tourism-related services, while also encouraging investment in vacation properties and second homes. Additionally, increased formal income and financial inclusion among remittance-receiving households boosts domestic consumption, benefiting transportation, commerce and service sectors closely linked to tourism.

The scalable model

Banreservas has deliberately adopted a scalable and selective expansion logic, prioritising model stabilisation in proven markets before extending to new ones. However, any future expansions are likely to be opportunity-driven and phased, to ensure that each new market sustains long-term client relationships. This strategy allows for progressive expansion, but only where three conditions converge: concentrated Dominican diaspora communities with sustained economic ties to the Dominican Republic, regulatory and operational feasibility, particularly the ability to support activity through representative offices or equivalent structures, and demonstrated demand signals.

The next three to five years points to a qualitative shift in diaspora investment behaviour. First, there is a clear movement from sentimental ownership to strategic investment. Second, diaspora investors are showing a stronger preference for formal, institutionally mediated channels. And finally, the younger diaspora segment tends to prioritise entry-level or future-orientated assets, while more established individuals focus on retirement, anchoring, or reintegration-linked purchases. This diversification of motivations is influencing how Banreservas structures advisory conversations and sequences client engagement over time.

With diaspora investment contributing to national economic development primarily by transforming external household income into structured, long-term domestic capital, Banreservas’ long-term objectives are driving financial inclusion, fostering foreign direct investment and supporting key productive sectors. By empowering confident diaspora investment, Banreservas reinforces its leadership role in national development while expanding its international footprint in a sustainable way by adopting a focused model that strengthens value creation in the Dominican Republic through targeted international interaction.

From a growth perspective, the expansion allows Banreservas to diversify its customer acquisition channels by engaging Dominican communities abroad at earlier stages of their financial decision-making. From an economic development standpoint, the strategy is goal orientated.

By facilitating diaspora investment in housing and related sectors in the Dominican Republic, Banreservas acts as a conduit that transforms external income flows into productive domestic investment.

TORONTO — Insurance provider Intact Financial Corp. says it had higher catastrophe losses and large losses in the second quarter than it initially expected.

Intact Financial reported that its combined catastrophe and large losses were $247 million above its expectations for the second quarter on a pre-tax and net of reinsurance basis.

The combined higher losses amount to $1.08 per diluted common share after tax.

Total catastrophe losses reached $416 million on a pre-tax basis during the second quarter and net of reinsurance.

The company says catastrophe losses in Canada were due to weather events, while commercial fires drove losses in the United Kingdom and Ireland.

Intact Financial says the increase in large losses included higher-frequency fire claims as well as other property losses across different geographies.

This report by The Canadian Press was first published July 8, 2026.

Companies in this story: (TSX: IFC)

The Canadian Press

-

Nevada20 seconds ago

Nevada20 seconds agoLocal artists on Northern Nevada stages, now through Labor Day weekend

-

New Hampshire3 minutes ago

New Hampshire3 minutes agoTrans athletes drop lawsuit to gain access to girls’ sports in New Hampshire after SCOTUS ruling

-

New Jersey8 minutes ago

New Jersey8 minutes agoFamily describes frantic moments delivering baby on the NJ Turnpike

-

New Mexico15 minutes ago

New Mexico15 minutes agoHidden gem in Cloudcroft, New Mexico has best BBQ in US

-

North Carolina18 minutes ago

North Carolina18 minutes agoNorth Carolina Airport Looks to Expand Commercial Service | AirlineGeeks.com

-

North Dakota23 minutes ago

North Dakota23 minutes agoSan Francisco plots risky socialist bank modeled after controversial experiment

-

Ohio30 minutes ago

Ohio30 minutes agoFeeling itchy? Ohio leads nation with 6 cities on Orkin’s 2026 bed bug list

-

Oklahoma33 minutes ago

Oklahoma33 minutes agoOklahoma’s Brent Venables named to 2026 Dodd Trophy Preseason watch list