Cop30 nearly went up in smoke – quite literally when a fire broke out in the conference centre. While the official statements talk about the historic success of the negotiations, a closer look at the results reveals a more fractured reality. Mired in geopolitical tensions, there were no clear winners. While some progress was made, the lack of a US delegation left a gaping hole in leadership; one that China was well positioned to take up, but failed to step up on its commitments.

With no one to put pressure on other economies like China and petrostates to take more responsibility, there was a lack of consensus and deep division on key issues. An effort to adopt a plan to phase out fossil fuels was dropped, and there was very little pressure on the shortfall in national climate commitments. The lack of a transition away from fossil fuels nearly derailed negotiations and in the end no mention of fossil fuels was made.

“Despite the disagreements over an explicit plan for the transition away from fossil fuels, the Paris Agreement implicitly mandates this as it is impossible [to] meet its goals without the replacement of dirty energy with clean alternatives across the world,” said Nicholas Stern, chair of the Grantham Research Institute at the London School of Economics.

Instead, leadership on transitioning away from fossil fuels is happening outside Cop, with the governments of Colombia and the Netherlands announcing their own international conference on the just transition away from fossil fuels, hoping to fill the gap that Cop30 has failed to address.

Still, it wasn’t all doom and gloom. Some measures were passed, including efforts on adaptation, just transition and climate finance. It also succeeded in putting more people impacted by climate change at the heart of the discussions, with a record number of Indigenous Peoples attending.

Advertisement

Adaptation finance to triple by 2035

On adaptation, Cop30 delivered what Stern called “genuine progress” with a pledge to triple the finance goal from US$40bn to $120bn annually by 2035. Yet this five-year delay from the 2030 timeline proposed by climate vulnerable nations leaves frontline communities without the necessary support to “match the escalating needs they are facing now”, said Mohamed Adow of Powershift Africa.

In Belém, parties formalised the Baku Adaptation Roadmap, a 2026-2028 work programme for operationalising adaptation goals, including support for vulnerable nations to develop national adaptation plans. A comprehensive set of 59 voluntary, non-prescriptive indicators to track progress under the Global Goal on Adaptation was also finalised at the summit, representing a significant step forward for transparency and accountability.

But there’s a flaw: no dedicated funding or clear mechanism was introduced to require rich countries to actually deliver adaptation finance. While the summit’s presidency promised adaptation would no longer be secondary to mitigation, the final text merely “urges” rich nations “to increase the trajectory of their collective provision of climate finance for adaptation”.

Consequently, there are fears those most exposed to, and least responsible for, climate impacts will be left to pick up the bill. Mamadou Ndong Toure of Practical Action in Senegal argued that: “Adaptation cannot be built on shrinking commitments; people on the frontline need predictable, accountable support.” Without binding finance, there is a danger adaptation goals remain aspirational.

Groundbreaking just transition mechanism established, but finance gap threatens delivery

Another serious institutional achievement of this year’s Cop was the establishment of the Belém Action Mechanism on Just Transition, following years of civil society pressure. The mechanism commits to providing technical assistance, capacity-building and knowledge sharing to ensure the transition away from fossil fuels supports workers and communities.

Advertisement

The new mechanism provides concrete steps towards implementation and ensures just transition will remain on the agenda at future summits.

Karabo Mokgonyana of Power Shift Africa celebrated the outcome, noting it had “finally grounded just transition in justice” by recognising equity, inclusivity, and the developmental needs of workers and communities, not just sectors or technologies as previous iterations did.

However, its effectiveness depends entirely on implementation. As Friederike Strub of Recourse Finance cautioned: “To make just transition happen we need public finance backing, systemic economic reform, and a clear roadmap to end fossil fuels.”

A critical concern remains that multilateral development banks (MDBs), which are expected to finance just transition projects, continue funding fossil fuels. With 73% of MDB climate finance delivered as loans rather than grants – often tied to austerity conditions – and MDBs actively promoting gas as a “transition fuel,” countries risk being locked into extractive models that directly contradict just transition principles.

Loss and damage fund launches

The final text also included a review of the Warsaw mechanism for loss and damage, the UN’s core policy framework for supporting countries on the frontlines of climate impacts. Financing for loss and damage has long been a fraught topic at previous Cops, with progress painfully slow: about $789m has been pledged to the fund but only around $432m is actually in the fund’s account.

Advertisement

At Cop30, the fund launched its first call for funding requests with US$250m in grants allocated for 2025–2026. Applications open on 15 December, with countries given six months to submit proposals.

Cop30 president André Corrêa do Lago speaking at Paris Climate and Nature Week, October 2025. Photo: Moriah Costa

Harjeet Singh, global engagement director at the Fossil Fuel Non‑Proliferation Treaty Initiative, argued that while the institutional architecture is now “fit for purpose”, money remains the missing piece: “A system cannot rebuild a home without money. Bureaucratic pledges cannot feed a family whose crops have failed.”

Two-year work programme on climate finance

Climate finance wasn’t one of the main agenda items but it ended up playing a key role during Cop. One of the efforts included the launch of a two-year work programme on climate finance with a focus on article 9 of the Paris Agreement which states that countries “shall provide” climate finance. This usually means public financing, but the $300bn a year goal from last year’s Cop includes public and private finance.

This has caused some debate, as developing countries argue it allows developed countries to meet the goal without increasing their contributions.

Instead, a compromise was reached to include a two-year roadmap on how to implement article 9, including the provision on country obligations which will be co-chaired by representatives from developing and developed countries.

Advertisement

This is part of a larger financing goal to $1.3tn, known as the Baku to Belém roadmap. While the roadmap delayed implementation by five years from 2030 to 2035, it includes practical steps on how to drive investment, said Ani Dasgupta, president and CEO of the World Resources Institute.

“Announcements throughout the week, from risk guarantees to country platforms, showed that these ideas are already moving from concept to implementation,” Dasgupta said.

$6.6bn in funding for Brazil’s Tropical Forest Forever Facility

Despite momentum around Brazil’s Tropical Forest Forever Facility (TFFF), the final outcome did not include a commitment to tackling deforestation. Still, Cop30 president André Aranha Corrêa do Lago said the Brazilian presidency would work on creating roadmaps on deforestation outside of Cop.

The final text did emphasise the importance of halting deforestation by 2030 to meet the Paris Agreement, but earlier drafts to reverse deforestation were left out

Brazil’s TFFF was hailed as a milestone by the Cop30 presidency, after it secured $6.6bn in funding from Germany, Norway, Brazil, Portugal, France and the Netherlands. The aim is to pay countries to keep their tropical forests instead of allowing them to be destroyed. It hopes to secure $25bn in funding to help support 74 tropical forest countries including Brazil and those in the Congo basin.

Advertisement

However, some have questioned how effective the fund will be without binding government rules to stop harmful logging practices, as well as concerns about the financial risk and very little involvement with Indigenous Peoples and local communities.

Critical minerals removed from final text

The removal of all references to critical minerals governance from the final text ranks among the summit’s most consequential failures. Despite vocal support from the African Group of Negotiators and the Alliance of Small Island States, draft language on “social and environmental risks” in mining and “responsible” mineral processing was deleted in final negotiations.

China’s delegation led the opposition, citing a lack of consensus on definitions and potential damage to Chinese business interests, according to observers speaking to Dialogue Earth. Yet the stakes are undeniable. “Minerals are the backbone of the shift away from fossil fuels,” warned Antonio Hill of the Natural Resource Governance Institute. “Leaving their governance out of just-transition planning will undermine efforts to accelerate renewable energies by 2030.”

Beyond Cop’s negotiating rooms, African leaders are charting their own course. At a high-level dialogue held ahead of the G20 summit, senior policymakers outlined a pan-African strategic plan for turning mineral wealth into negotiating power.

Panellists stressed the importance of harmonised, robust ESG standards as well as a home-grown regional green mineral development fund. They also insisted technology transfers – another commitment cut from Cop30’s final text – must be “non-negotiable” for partners relying on the continent’s abundant mineral wealth to drive their own green industrialisation going forward.

Advertisement

Marit Kitaw, former director of the African Union’s Minerals Development Centre who appeared on the panel, framed the challenge in comments on LinkedIn: “Africa holds the mineral ingredients for the global energy transition. The question is: is Africa ready to lead, to bargain, to industrialise, and become a rule-maker?”

When you’re running a business of whatever size, it’s critical to know your numbers – but when you’re running the finances for 22 schools, it’s even more imperative to get your maths right.

Established in 2016, Sapientia Education Trust (SET) is responsible for more than 8,500 pupils and 1,300 staff across Norfolk and Suffolk. However, until 2022, the administration of its finances was still being done the old school way – manually – with piles of paper-based files and spreadsheets.

Steven Dewing, SET’s chief financial officer, says: “When I joined in September 2021, the team were struggling. The trust was recovering after Covid, and getting invoices paid on time and reports delivered on time was a challenge.”

The system being used by the trust was adopted back when it encompassed just five schools. By the time Dewing joined, the number of schools had risen to 15 – each with its own database and no sharing of data. “There were lots of silos.”

Dewing recalls how his deputy needed a whole day each month simply to reconcile it all, with numbers pulled out and manually put on to consolidated spreadsheets. Only then could data be manipulated into the right formats needed.

Advertisement

“That was not uncommon for finance departments,” he says, “but it is very prone to error. Also, invoices were being manually signed, requisitions were written by hand, and because we had a different system for each school, we couldn’t join these up. People physically carried around loads of paper, so it was hard to maintain compliance.”

‘Everything in one database’

All this changed in September 2022 when SET moved to a new system, Sage Intacct, which was rolled out with the support of ION, a Sage Education implementation partner.

And for a trust that includes the country’s largest state boarding school with 1,400 children alongside small, rural primary schools with as few as 16 pupils, the finance platform was a gamechanger.

The trust includes the country’s largest state boarding school

“Now we have everything in one database,” says Dewing. “Each school is still its own entity, but it’s all shared so there is no manual reconciling, it all just happens in the system.”

He adds that using Intacct has also meant SET can combine purchasing across the trust, allowing it to benefit from economies of scale and supplier discounts, while reducing the admin of having to purchase across all its schools.

Advertisement

He also highlights the platform’s ease of use and describes how having access to personalised dashboards for every user has been a massive step forward. “We used to pull out data and then email it to people,” he says, “but now depending on what level you are and what your role is, there are different dashboards. Users can go in and see information whenever they want and drill down to the transaction. It has enabled us to empower them with data they need, when they need it.”

Successful use cases for this part of the implementation include head teachers in SET’s small rural schools seeing an accurate and real-time position of their finances, with staff able to login from any location any time to study the data and reports.

“What’s good is we can pull in non-financial information too, like pupil numbers and staff numbers,” adds Dewing. “You can then combine that with other data to give cost per student, cost per staff member, and much more, without any Excel manipulation.”

Adding up the time saved with AI

Within SET’s finance department, a pool of four people is responsible for multiple schools reporting to Dewing. Below this there are others who input transactions, invoices and payments.

To ensure the department was up to speed from day one, ION provided training in Sage Intacct during the onboarding process. It offered Dewing and his colleagues a structured programme, which the CFO says was a major help given “it’s a really big bit of software with lots of different functionality”.

Advertisement

AI tools have proved to be an invaluable timesaver for processing invoices

“Having someone guide you through it and teach you what it does, while making sure you’re doing the right things at the right time, was vital,” he says. “We broke the training down into four two-hour sessions rather than one whole day and also got them to record some short videos, which we continue to use.”

Dewing has found a number of Sage Intacct’s AI-driven tools particularly useful. For instance, Outlier Detection, which automatically spots data appearing in odd patterns and suggests corrections, and Accounts Payable Automation, which uses AI to populate invoices against purchase orders.

Given that SET processes more than 25,000 invoices a year, this represents a transformational timesaver for colleagues who no longer have to input the details themselves and simply now check over the AI-prepared documents.

Dewing cites this as just one key example of how the move to Sage Intacct has revolutionised what his finance team can do for the wider trust.

“It has enabled finance to move from a pure admin function, where you carry bits of paper around and get things paid, to a strategic partner in the organisation,” he says. It’s become less about ‘have we paid this on time or have we ordered that’, because that just happens through the system.

Advertisement

“We can now spend far more time supporting people to take financial decisions and in budgeting. Sage Intacct has changed our relationships with the schools because they see what value we bring.”

Find out more about Sage Intacct and book a demo, at: sage.com

There’s no better time to start preparing your portfolio for volatility.

Stock prices may be surging, but many investors are having mixed feelings about the market.

While nearly 40% of investors still feel optimistic about the next six months, according to the most recent weekly survey from the American Association of Individual Investors, roughly 30% worry that stock prices will fall in the coming months.

Nobody can predict the future, especially the short term. But there are a couple of warning signs investors may want to pay attention to right now — along with some steps to prepare for a potential downturn.

Image source: Getty Images.

Advertisement

Will the stock market crash in 2026?

There’s no way to predict what the market will do this year, but it can sometimes be helpful to use historical context to get a sense of what’s happened in similar circumstances. And there are two stock market metrics that have not-so-good news for investors.

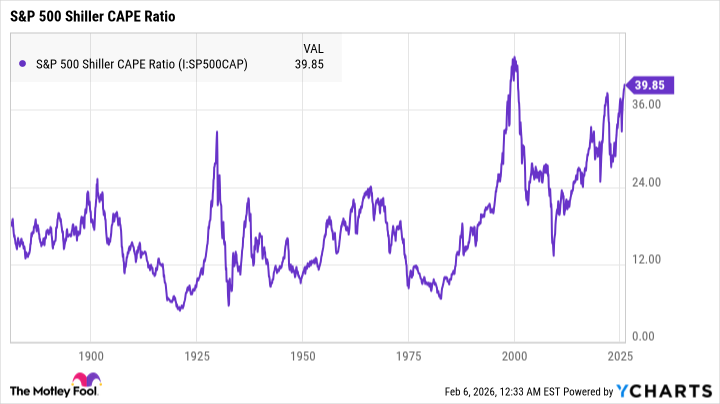

First, the S&P 500 Shiller CAPE (cyclically adjusted price-to-earnings) ratio. This metric is based on the average inflation-adjusted earnings over the last 10 years, and it’s commonly used to determine whether the S&P 500 is over- or undervalued. The higher the figure, the more overvalued the index may be.

Historically, the average Shiller CAPE ratio sits at around 17. As of February 2026, though, this metric is nearing 40. This is the second-highest value in history, next to the peak prior to the dot-com bubble in the early 2000s.

S&P 500 Shiller CAPE Ratio data by YCharts. CAPE Ratio = cyclically adjusted price-to-earnings ratio.

The second metric to watch is the Buffett indicator, which measures the ratio of U.S. gross domestic product (GDP) to the total market value of U.S. stocks. It was popularized by Warren Buffett, who explained in a 2001 interview with Fortune magazine how he used the metric to correctly predict the dot-com bubble burst.

Advertisement

“For me, the message of that chart is this: If the percentage relationship falls to the 70% or 80% area, buying stocks is likely to work very well for you,” he said. “If the ratio approaches 200% — as it did in 1999 and a part of 2000 — you are playing with fire.”

As of this writing, the Buffett indicator sits at 221%. The last time the metric neared 200% was in November 2021, just before stocks entered a bear market that would last nearly a year.

What should investors do right now?

No stock market metric is perfect, as past performance doesn’t predict future returns. Even if there are strong historical patterns suggesting a downturn could be looming, that doesn’t necessarily mean a crash, recession, or bear market is imminent.

Perhaps the best thing investors can do right now is ensure their portfolios are prepared for volatility, just in case. That involves double-checking that you’re only investing in stocks with strong fundamentals, such as:

Healthy finances: A company needs to be on a solid financial footing to survive an economic downturn. Shaky companies can still thrive when the market is surging, so stock price alone isn’t necessarily a sign of financial health. Now is a good time to comb through financial statements to review metrics such as profitability, debt, revenue growth, and other factors that can indicate whether a company is likely to survive tough economic times.

Competitive advantage: When the dot-com bubble burst in the early 2000s and much of the tech sector collapsed, the companies that survived were those that had a leg up over their peers. Organizations that didn’t offer anything unique or had nonviable business models crashed and burned, and the same could happen again if we face another significant downturn.

A strong leadership team: Sometimes, a company’s survival depends on the decisions by leadership during pivotal moments. Even a strong business may struggle if the executive team consistently makes poor choices, making this a key factor for long-term success.

The stronger your portfolio, the more likely it is that it will survive even the worst bear market or recession. By double-checking all your investments now, you’ll be prepared no matter what may lie ahead.

Fifty years ago, the U.S. Supreme Court decided Buckley v. Valeo, legitimizing the idea that spending money in elections is a form of free speech. Thirty-four years later, Citizens United v. FEC went even further, granting corporations and unions, not just individuals, the right to spend unlimited sums to influence American elections.

These rulings, and the distorted view of the First Amendment behind them, have had serious consequences. Nearly $15 billion was spent in the 2024 election cycle alone, even as large majorities of Americans agree that money in politics is a threat to our elections. Here in Oregon, where we value civic participation and close-to-the-voter elections, it’s increasingly difficult for ordinary voters to compete with massive outside spending.

Even at the state and local level, Oregonians have limited authority over how money operates in our elections. That power has been centralized in the hands of unelected judges who were never meant to write election policy for the entire nation. It’s part of why everything feels so broken: a system where citizens cannot govern the rules of their own elections is not sustainable.

There is hope. A constitutional amendment would restore the ability of Congress and the states, including Oregon, to set reasonable limits on money in politics. Our nation is at a turning point, and we need to take action now. I encourage my fellow Oregonians to learn more about this vital issue, and urge our elected officials to support a constitutional amendment that will allow us to create common sense limits on the power of money in our elections.

Maud McCole, Eugene

Advertisement

Other things to consider about Good, Pretti deaths

While we all can agree that the deaths of the two protesters in Minneapolis were regrettable, it should be noted that those deaths were entirely preventable.

First and foremost, the incompetent and corrupt Biden administration allowed millions of illegal aliens into the United States without any sort of vetting or other means of identification.

Second, the sanctuary city policy of Minneapolis makes it very difficult for law enforcement to do their job. This, coupled with a fawning media and cowardly politicians cheering on and encouraging lawlessness, contributed largely to the deaths of Renee Good and Alex Pretti.

Raymond Moreno, Eugene

Advertisement

Support lodging tax increase for wildlife

The most important bill (to these readers) in the 2026 legislative session is HB 4134: “1% for Wildlife.” It adds 1.25% — less than the cost of a cup of coffee a day — to the statewide Tourism Lodging Tax (TLT). This legislation had bipartisan support in the 2025 legislature, but failed to get a floor vote in the Senate before adjournment. Funds raised with this fee go directly to Oregon Department of Fish and Wildlife for wildlife and habitat conservation. They assure a sustainable funding stream in the face of uncertain federal funds. This year’s bill adds .25% for wildlife stewardship and rehabilitation programs, including wolf depredation compensation.

Biological diversity — both floral and faunal — knows no geopolitical bounds nor ecological/economic bounds. Wildlife species, and their habitats, abound in Oregon. They transcend whatever artificial bounds we attempt to place upon them. Local, national, and international tourists visit throughout every year to enjoy our oceans, forests, valleys, mountains, watersheds, meadows, and deserts. Thus, in addition to the intrinsic ecological value of biodiversity, the economic value of our wildlife exceeds the investment to sustain it. From whale watchers to bird watchers, hunters to fishers, wildlife opportunities abound. Let’s make sure they stay that way.

Please urge your state representative and senator to vote YES on HB 4134.

David and Judy Berg, Eugene

Former Minneapolis residents horrified

As former residents of South Minneapolis, we are observing the horrifying, sad andgratifying events unfolding in real time; the horrifying killing of Renee Nicole Good, and Alex Pretti, then the sad adolescent, cruel and destructive response of the Trump administration and his sycophants.

Advertisement

What’s gratifying is to see the same savvy and united uprising of the activist neighborhood, many public officials, and the Twin Cities, and now in Eugene, Springfield, and the many other Oregon towns. Stay strong until ICE stands down and is held accountable.

“I’m not mad at you,” she said, and then Renee Nicole Good was dead …then Alex Pretti…???

Jan Nelson, Edward Winter and Rebecca La Mothe, all Eugene, et al.

Not all protesters are vandals

The First Amendment gives us the right to peacefully assemble and to petition the government for a redress of our grievances. To me, this is more than a right. It is my responsibility. If the citizens had not risen up in 1776 in the American Revolution, we would be an English territory under a king. That would have served the king well, but not the rest of us.

So I peacefully assemble and protest against anything that infringes on my freedom or the freedom of others; against anything that goes against the protections of the Constitution’s due process of law. I protest ICE and the many laws they break to meet quota.

Advertisement

I stand on the corner with my sign and I glory in the endless stream of cars honking in agreement and the occasional middle finger. It is invigorating to see the American spirit is alive and well.

Last Friday, during this peaceful gathering on Seventh and Pearl, a second, smaller gathering took place with a different approach at a slightly different location. They made loud noises and banged on the federal building office windows to the point of breaking the glass. The message was clear and the response was predictable.

I do not favor violence to any degree, from protesters or ICE agents. It draws attention away from the message we had congregated to express. But, I caution myself and others to not use disruption, broken windows or spray paint as an excuse to lump together the entire protesting world, imposing the identity of the minority with the entire movement.

Some people are horribly disturbed at the breaking of windows and spray paint. I’m against it, too. But I am more horrified at what is happening to citizens and guests in the U.S. by the violent and illegal grabbing of people off the streets — like they did in WWII Germany to the Jewish population. So if we are outraged at a broken window more than we are outraged at cruel and atrocious illegal arrests without warrant or due process, we need to rethink our stance and our purpose.

Candy Neville, Eugene

Advertisement

Not handouts, hands up

What if we could end homelessness — not with handouts, but with high school diplomas?

Research consistently shows that lacking a diploma is the single greatest risk factor for homelessness. Yet traditional education fails millions who learn differently. Global Sovereign University exists to change that.

GSU is a 501(c)(3) educational foundation built on one principle: teach a man to fish. Our free online platform meets learners where they are — whether they’re visual thinkers failed by rigid classrooms, adults seeking trade skills, or anyone overlooked by conventional systems.

What makes us different? Gamified learning that rewards progress. AI tutoring available 24/7. And “Civilization Builders” — retired professionals volunteering as mentors to share real-world wisdom with the next generation.

We don’t measure success by grades. We measure it by changed lives: someone landing their first job, a parent helping their child with homework, a veteran transitioning to civilian employment.

Advertisement

Education shouldn’t create dependency. It should build capability. GSU provides the tools; learners build their own futures.

Visit GlobalSovereignUniversity.org to learn more, volunteer as a mentor, or support our mission. Together, we can build a bridge to freedom—one learner at a time.