Business

Is this the solution to California's soaring insurance prices due to wildfire risk?

In the past several years, homeowners across the state have been either burdened with extremely high insurance premiums or have struggled to find coverage at all. Wildfires have sent California’s homeowners insurance market into crisis and the situation is only getting worse. So far, 2024 has seen 219,247 acres burned, more than 20 times the amount this time last year. As wildfires become more frequent and destructive, insurers have worked to lower their risk exposure through rate hikes, nonrenewals, and even halting new policies in the state entirely.

New buyers and those whose policies have not been renewed have limited options since the biggest companies, State Farm, Farmers, Allstate, USAA, Travelers, Nationwide and Chubb, have limited or paused new policies in the last few years. Earlier this month State Farm’s cancellations of 30,000 homeowner policies mostly in high wildfire risk areas, took effect. In late June, State Farm requested a 31% rate increase, its largest increase in recent history, on the heels of a 22% increase earlier this year. Allstate also recently filed a request for a significant 34% rate increase.

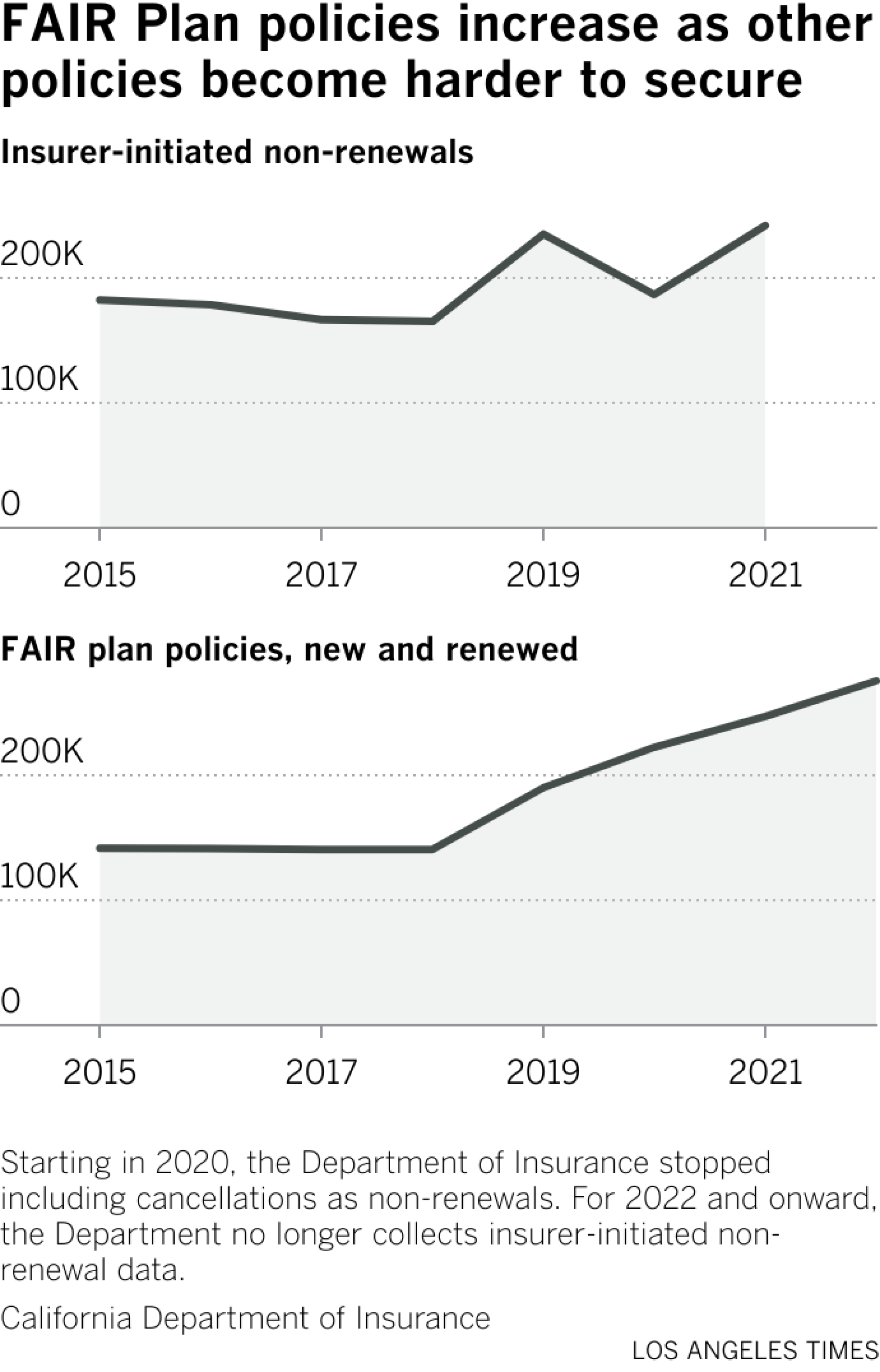

Homeowners are finding the expense and lack of options unsustainable. Sharon Goldman, longtime resident of the Pacific Palisades, has not had her policy canceled yet, but she has seen increases to her premium and worries she could be next. In her ZIP Code the wildfire risk is high, and State Farm decided to not renew 70% of their policies. Starting in 2019, rates of nonrenewals in high- and very high-risk areas grew to 14% compared with 3% and 2% for moderate- and low-risk areas.

Goldman, using her maiden name out of concern for retribution from State Farm, has paid her premiums each year since she bought her home 50 years ago. She has never filed a claim. But she has seen her rate increase 78% in the past two years. Her agent has told her that her fire coverage will be replaced with the state-run FAIR plan in 2025, an increasingly common insurer strategy that leaves homeowners paying more for less coverage.

Sharon Goldman poses for a portrait in Pacific Palisades in June. She is one of the many California homeowners struggling to maintain home insurance as costs increase and policies are dropped due to wildfire risk.

(Dania Maxwell/Los Angeles Times)

Goldman and her neighbors are left wondering what options they have left. She hears stories of people paying tens of thousands a year, an impossible amount for her to cover on her retirement budget. She has started looking into moving out of state and out of the home where she raised her children.

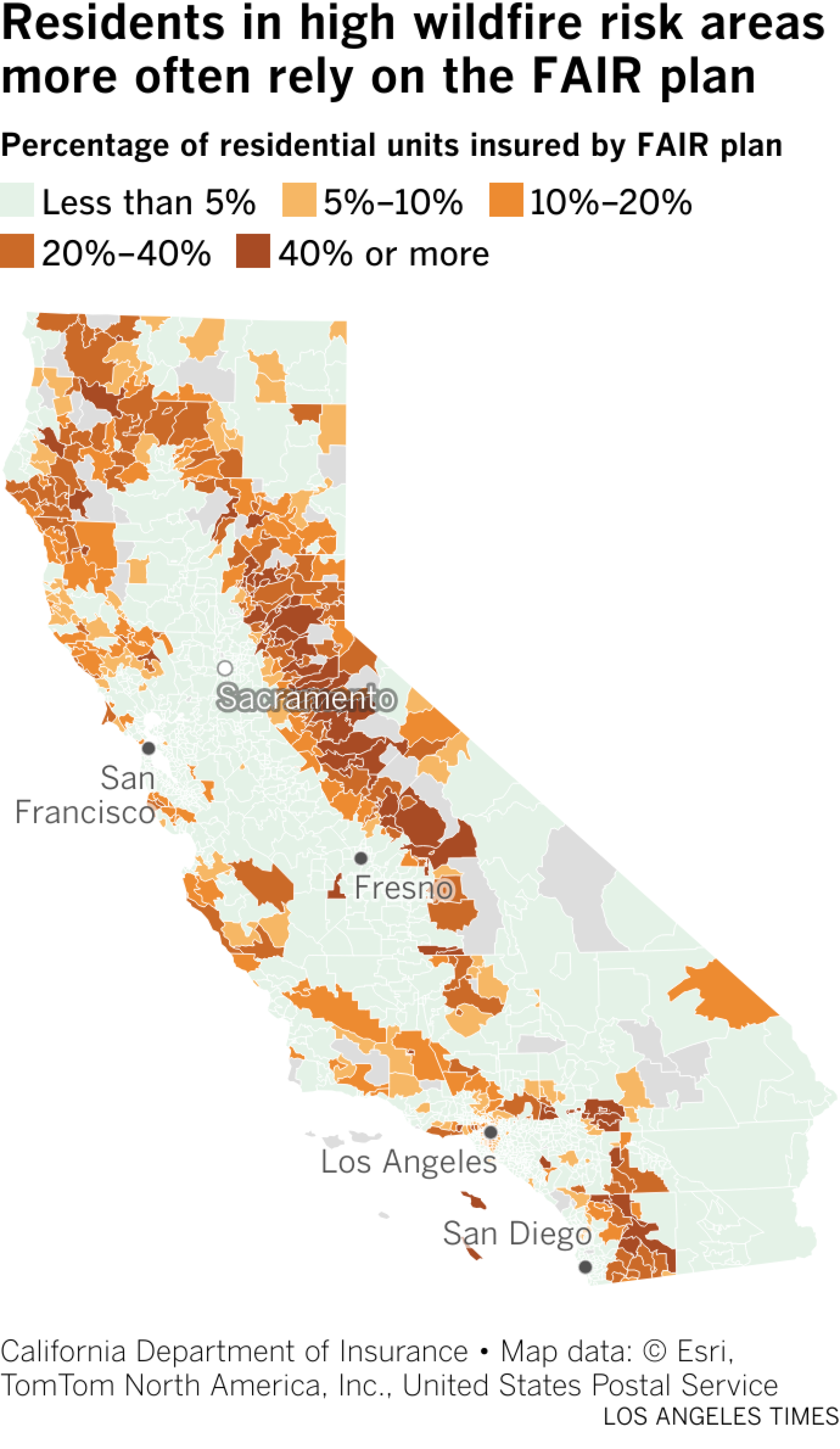

While the state does not require insurance, mortgage lenders do. So, going without is not an option for many. Those whose mortgage is paid off, like Goldman, may not be comfortable leaving their home, typically their most expensive asset, uninsured. High rates and loss of fire coverage have pushed desperate homeowners to riskier nonadmitted carriers or to the state-run FAIR plan, meant to be the plan of last resort. But the California Department of Insurance worries that it is quickly becoming overburdened.

Over the past year, Insurance Commissioner Ricardo Lara has been rolling out his plan to increase policy writing in vulnerable areas and get people off of the FAIR plan. One big component of his strategy is allowing insurers to use wildfire catastrophe models to set overall rates. Insurers say the tool would help them more accurately predict the correct rate for the amount of risk.

As a trade-off, Lara says companies that use these models will be required to increase service in distressed areas with a high wildfire risk and a high concentration of FAIR plan policies.

In public workshops held by the Department of Insurance, consumer advocates raised concerns about a lack of transparency with “black box” models that may be used to justify unnecessary rate hikes. Industry advocates are concerned the plan will take too long to implement when they desperately need changes now.

How likely is it a house will be damaged in a wildfire?

There are many versions of catastrophe models. Each modeling company has their own proprietary analysis but they all generally use the same data inputs to answer the same question.

The Harwarden fire burned over 500 acres, destroying three large homes and damaging seven others.

(Jen Osborne / For the Times)

Each modeled event starts with an ignition, the probability that a fire will start at that location, spread, the probability that the fire will travel based on the land cover in the area, and property characteristics. Using those data, the model simulates a large number of possible outcomes for a given location, estimates the likelihood that a structure will burn from wildfire, and calculates the loss for any buildings there.

The USDA Forest Service developed a national analysis of wildfire risk that is similar to what models created for insurance companies would look like. Based on vegetation and fire-behavior fuel models, topographic data, historical weather patterns and long-term simulations of large wildfire behavior, their wildfire likelihood map shows the probability of a fire in any given year.

A critical part of predicting the potential spread of the fire is the available fuel. The Forest Service’s land cover classifications are used in many wildfire models. They specify 40 different fuel types such as grass, shrub, timber, and nonburnable types. Each category is further subdivided based on depth of the cover and humidity or aridity of the climate.

For example, in an arid climate, coarse continuous grass at a depth of 3 feet would have a very high spread rate. A combination of low grass or shrubs and dead leaves or needles in the forest would have a low spread rate.

Property characteristics such as the type of roof or whether the siding is fire-resistive make a significant difference in whether a structure will ignite from wildfire embers. The Center for Insurance Policy and Research found that structural modifications can reduce wildfire risk up to 40%, and structural and vegetation modifications combined can reduce wildfire risk up to 75%.

All of these factors are combined in the model with information about the rebuilding cost and level of coverage to generate an amount of risk unique to the individual property.

Could these models turn the industry around?

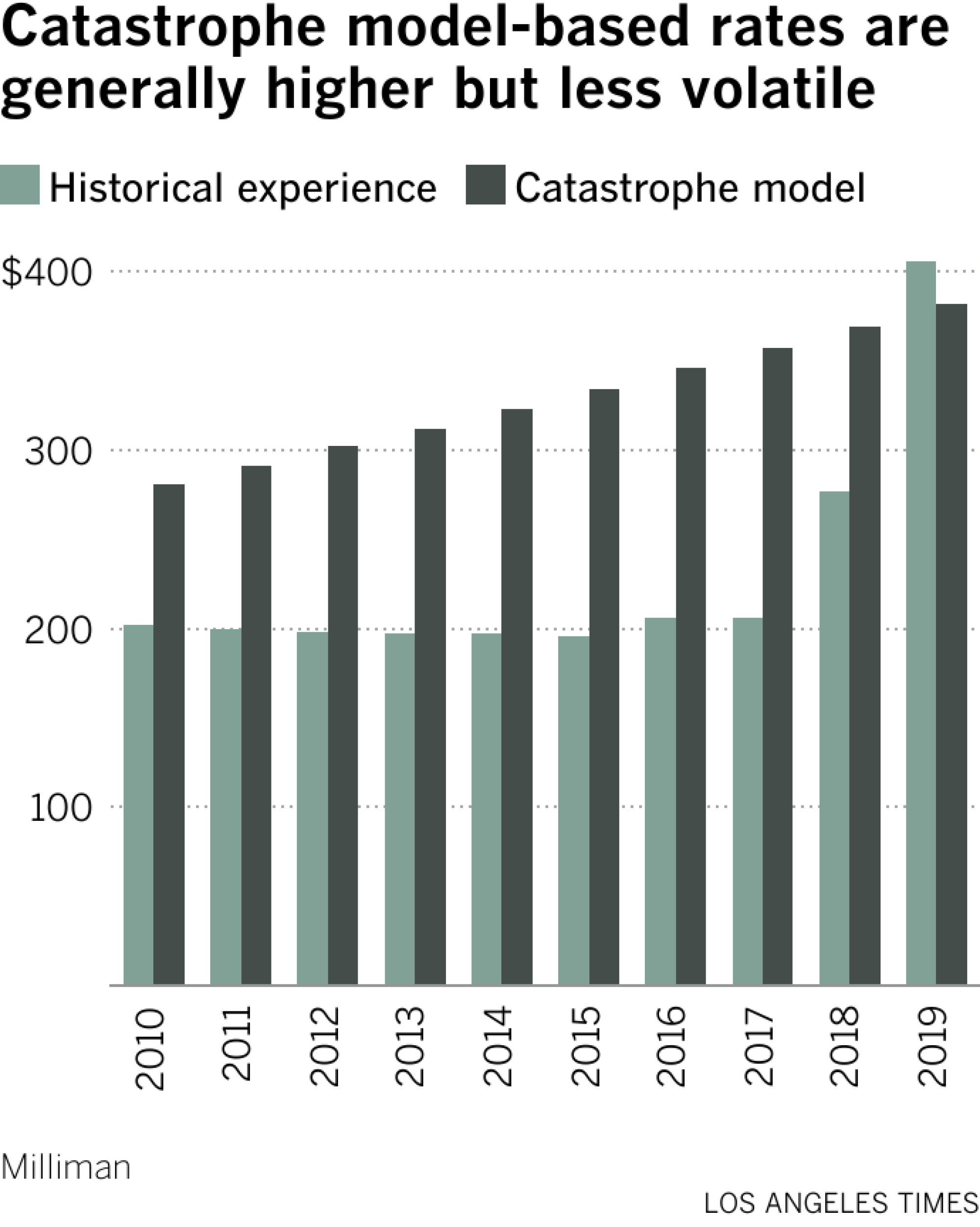

Currently, companies are required to calculate their projected losses, on which their overall rates are based, using a historical view of wildfire loss over the previous 20 years. As wildfires increase, however, this means that the average loss trails behind the current state of wildfire risk.

Nancy Watkins, an actuary and principal at the insurance consulting firm Milliman, said that she believes the inclusion of catastrophe models could save the industry. She analyzed the effect of a model on rates compared with using just historical experience. While the rates would generally be higher, the increases would be more even.

In April during a public meeting, Allstate said that if wildfire catastrophe models were allowed, they would once again start writing new policies in the state.

But wildfire catastrophe models are already used by insurance companies in California for some business decisions and have been for some time. They use models to determine where to write or renew policies, which is one of the reasons nonrenewals have disproportionately happened in high-risk areas.

In recent rate filings, Allstate, Farmers and State Farm cited a modeled wildfire risk score as the basis for not renewing policies. Allstate used CoreLogic’s Risk Meter score in 2019 to classify all policies that fell above certain risk thresholds as ineligible for renewal. A 2023 filing from Farmers documents eligibility guidelines for new and renewing policies that sets a risk level using Verisk’s FireLine and Zesty.ai’s Z-FIRE scores. State Farm’s recent 30,000 nonrenewals are based on CoreLogic’s Brushfire Risk Layer.

Amy Bach, executive director of United Policyholders, says that wildfire models worked their way into rates without enough state oversight. “We didn’t regulate the use of risk scores and now [they] are having a dramatic impact on the market and the genie is out of the bottle.”

Some companies use models to assess relative risk between properties and adjust individual rates accordingly. State Farm multiplies its base rate by a location rating factor, calculated using catastrophe models produced by CoreLogic and Verisk. Areas with high wildfire risk have seen dramatic increases in the location rating factor in the past few years.

This process is called segmentation and the Department of Insurance is aware that it is opaque. Department spokesperson Michael Soller says, “People do not know what their risk score is. They don’t know what goes into the risk score. It’s a black box. Yet, the risk score can be used to [charge you] double what somebody else pays.”

While these situations are significant for some, they generally only apply to select high-risk properties. The median effect of the location rating factor has remained fairly stable.

But under the commissioner’s new policy, model results could also be incorporated directly into the overall rate. Soller says that one important difference in this new regulation is that for a model to be valid, it will need to incorporate property and community level risk mitigation into rates, including state agency forest thinning and utility company efforts. As more investment goes into making communities safer, in theory the rates should decrease.

Only you can prevent forest fires?

Wildfire mitigation happens at the state and local level. Since 2020, in addition to baseline spending, California has allocated more than $2.6 billion towards its wildfire and forest resilience package. 872 communities in the state are registered participants in Firewise USA, a program administered by the National Fire Protection Association that sets standards for fire safety.

For an individual, retrofitting one’s home for wildfire resistance is not cheap. On average, homeowners spend $15,000 on a new roof.

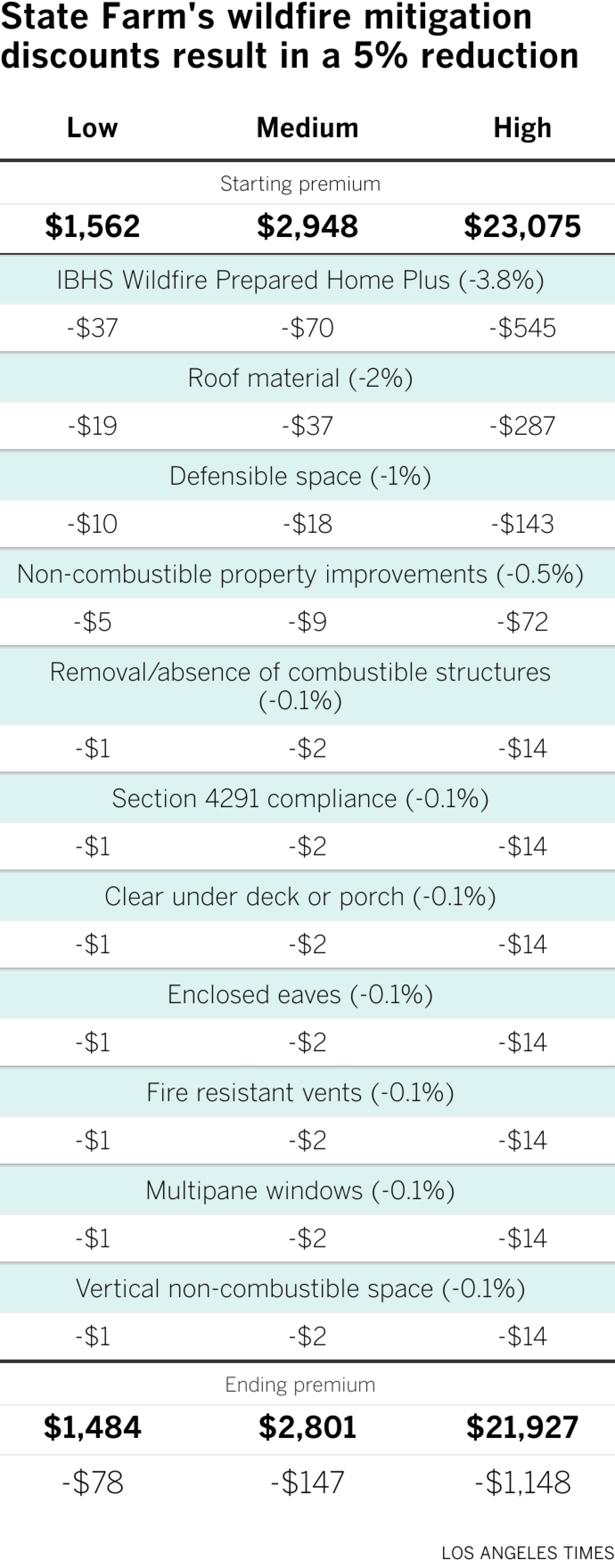

As of October 2022, companies such as State Farm that use wildfire models in segmentation are already supposed to give mitigation discounts. A February filing from State Farm breaks down how their discounts would work in a low-, medium- and high-risk area.

For the low-risk group, the dollar amount saved may not be worth the investment in mitigation. For the high-risk group, the slightly lower percentage reductions would still result in more substantial dollar amounts saved.

According to the State Farm documents, these discounts are given at a set rate for all properties across the state. Granular catastrophe models take into account the impact of mitigation on the property level, nearby community mitigation and any recent wildfire history that might indicate a temporarily reduced risk.

However, a complaint raised several times during the regulation workshops was that when homeowners do spend money, often thousands, on lowering risk, they do not see any changes in their insurance premiums. Some say their policies were still dropped.

Goldman has already completed the property-level mitigation work. She has a class A Spanish tile roof. She does the brush clearance every year. This past year it cost about $1,200. She even has an outdoor sprinkler system. But she did not learn about mitigation from her insurance company. Instead, it was on one of Bach’s monthly educational community calls where she got the idea to install fire-resistant vents.

Sharon Goldman walks through the exterior of her home where she has lived for about 50 years and raised four kids in Pacific Palisades. (Dania Maxwell/Los Angeles Times)

And yet, she has not received a mitigation credit from State Farm and has not received any information about how to receive one. When she asked her agent whether the work she had done on her home qualified for a discount he said no. The Department of Insurance says that they review consumer complaints for rate accuracy and conduct regular examinations of insurance companies. They noted that concerned consumers should contact them to review their specific situation.

Making models a reality

The catastrophe modeling regulation requires insurers to submit their modeling information to the Department of Insurance for review by an internal model advisor and any necessary consultants. Some proprietary information is allowed to remain confidential but proponents of the plan say that the regulators will have all the information they need to assess the models even if the general public does not.

Firefighters work to douse a home on fire in Harwarden Hills, a high-end living community in Riverside.

(Jen Osborne / For The Times)

The department says it is still considering public input from the most recent workshop and has no further plans for additional workshops. Once the regulation is finalized there will be a public hearing. Commissioner Lara plans to have this regulation and the rest of the Sustainable Insurance Plan in place by the end of the year.

In addition to forward-looking catastrophe models, Lara’s plan will introduce the ability for insurance companies to include reinsurance costs in rates and to increase coverage in the FAIR plan. Details for both of those changes are expected to be released this month.

Los Angeles County saw job gains in May, likely driven in part by rebuilding after the January 2025 wildfires, which destroyed or damaged more than 18,000 structures.

Construction added 2,300 jobs since April, while postings for new jobs in the industry jumped 45% over a year ago —indicating rebuilding in Pacific Palisades, Altadena and nearby is helping boost the local economy, according to a report by the Los Angeles County Economic Development Corp.

“This is consistent with the possibility that wildfire rebuilding activity is increasing construction labor demand in the area,” Max Chomas, an economist at the LAEDC Institute for Applied Economics, said at a presentation this week based on California Employment Development Department and other data.

Motion picture and sound recordings also added 2,800 jobs during the month, despite a deep downturn in Hollywood caused by a reduction in streaming filming, runaway production and other factors. The industry lost 6,700 jobs compared with a year ago.

Still, the job growth since April in construction and Hollywood were among the highlights of a month that saw total county payroll jobs — excluding agriculture and certain other sectors — grow by 9,000 jobs, to 4,618,400. Employment was virtually flat from the same time a year ago.

“May was a relatively good month for employment growth,” Chomas said.

The biggest monthly job gainers were the hotel and restaurant industries, which added 3,700 jobs.

Manufacturing, which has been hit by job losses over recent years, added 400 jobs since April. It also saw a 15% increase in job postings compared with a year ago.

That could reflect the resurgence in Southern California’s aerospace and defense industries, which have seen a sharp rise in startups.

Postings for all new jobs were up 1,134, or 2.4%, since a year ago. Chomas noted that May was only one of five months over the last three years that saw year-over-year growth in job postings.

The gains helped stabilize the county’s unemployment rate at 5.2%, matching April’s rate and down from 5.4% in May 2025.

Still, that is higher than May’s 4.3% national unemployment rate, and it masked some weakness in the local economy.

The rate is calculated by a household survey to determine which members are working, looking for work or no longer seeking employment.

It found 18,000 workers had dropped out of the county labor force in May, artificially driving down the unemployment rate, according the California EDD.

Similarly, California recorded a 5.3% unemployment rate in May, on par with April, despite a drop in the labor force.

That rate is higher than every state other than Delaware. In May, California only added 3,100 non-farm jobs month-over-month — a job growth rate that lags behind the nation, according to an analysis by the Inland Empire Economic Partnership and the Lowe Institute of Political Economy at Claremont McKenna College.

The LAEDC’s report also examined the potential effects the growth in artificial intelligence has been having on L.A. County jobs “exposed” to AI, meaning they are vulnerable to AI replacement.

California has been hit hard by thousands of AI-related layoffs in Silicon Valley as the software has been integrated into the tech workplace — even though there is fierce competition for software engineers with skills and expertise in the field.

The report found that since July 2023, job listings in Los Angeles County for AI-exposed positions — such as clerical and translation positions — have lagged behind other jobs. However, it is unclear whether businesses have replaced or are waiting to replace those workers with AI.

It may be that employers overhired for those positions during the COVID-19 pandemic and are now shedding them, since there is a correlation between AI-exposed positions and those jobs that can be completed from home, Chomas said.

The report also examined macroeconomic trends and policy decisions affecting the national, state and Los Angeles County economies — which have been hit by tariffs, the crackdown on immigrant labor and high energy costs, among other factors.

Nevertheless, consumers continue to spend despite affordability strains, and employers continue to hire selectively amid higher interest rates to battle inflation, said institute economist Shannon Sedgwick.

“During the previous decade, we experienced extraordinarily low inflation, near zero interest rates, relatively stable globalization, and abundant capital. So those conditions may have conditioned us to think that environment was normal,” she said.

“But historically speaking, today’s world of higher rates, greater geopolitical uncertainty and tighter labor markets, they may actually be closer to that long-run average,” Sedgwick noted.

A proposal to build a truck parking lot near the Port of Los Angeles is facing backlash from nearby residents.

Port officials say the parking lot would provide much-needed designated space for cargo trucks waiting to pick up loads from the port, helping to ease congestion in the area.

But some neighborhood groups say the proposed staging area would only increase traffic and air pollution in Wilmington.

Gina Martinez, chair of the executive board of the Wilmington Neighborhood Council, said the land in question provides a vital buffer between port activity and residential communities.

“It’s been a bad deal from the beginning,” Martinez said in an interview. “We want open space because we’ve been promised for decades a clear separation from port activities.”

The Los Angeles Harbor Commission signed off on the project in a meeting on June 11, but it was vetoed by the Los Angeles City Council this week.

The veto does not permanently ban the project, but allows for more time to discuss the implications for stakeholders and the community.

Los Angeles City Councilmember Tim McOsker, who introduced a special motion to halt the truck plans, said he was acting on behalf of community residents. McOsker represents Harbor City, Harbor Gateway, San Pedro, Watts, and Wilmington.

“Generally, folks in the community would say, ‘we don’t want the port industrial properties to creep into neighborhoods. We want them to retract or hold the line,’” McOsker told The Times.

The John S. Gibson Truck & Chassis Parking Lot, which was originally proposed in 2023 by the Port of Los Angeles, would cover 18 acres of privately owned land and include 393 truck and chassis parking stalls.

The land is currently designated as open space, though it’s undeveloped and not available for any recreational use. The completion of the parking lot would require a Port of Los Angeles master plan amendment to switch the land’s designation from open space to maritime support.

Martinez said the land should have never been sold to private developers because it’s included in the California State Lands Commission’s tidelands trust, which says certain land near the ocean must be available for public enjoyment.

Building a truck and chassis waiting lot on that space would increase congestion on the freeways and in Wilmington neighborhoods, add particulate matter into the air and increase already-problematic noise pollution from the port, she said.

“Of all the things Wilmington needs, it is not another parking lot for trucks,” Martinez said at a Los Angeles Harbor Commission meeting earlier this month. “It is not the responsibility of our community to take on every single truck that runs through the port.”

At the same meeting, Noel Gould of the Coastal San Pedro Neighborhood Council said the council is supporting the project after working closely with the developers to reach compromises.

The parking lot would prevent port-bound trucks from idling near schools and parks, he said. The lot would also include landscaping with native coastal plants.

“We didn’t start out in a position of support, but we worked very closely with them to get to a place where we felt it was really something that would benefit the community,” Gould said at the meeting.

In an interview, McOsker said there is already space set aside for trucks to wait to access the port.

At the Los Angeles City Council meeting Wednesday, the council unanimously approved what’s known as a 245 motion, which gives the council authority to temporarily veto certain actions taken by city boards and commissions.

“The 245 gives us the opportunity to meet and confer and see if there are revisions or additions or mitigation that can better protect the full community,” McOsker said.

The motion sends the project proposal back to the Harbor Commission for further review.

Supporters of the parking lot say the land is currently uninhabited and requires consistent police presence to deter criminal activities.

The Port of Los Angeles also clashed with coastal communities last year over the possible raising of the Vincent Thomas Bridge. The bridge was already slated to be redecked by the California Department of Transportation, but Port of Los Angeles executive director Gene Seroka proposed raising the bridge height as well.

Raising the bridge would allow larger cargo ships to pass under its deck, helping create jobs and keep the port relevant, Seroka said at the time. Most painfully for local commuters and businesses, it would mean the bridge will be closed for around 28 months rather than the originally planned 16 months.

Last December, the California State Transportation agency rejected the proposal to raise the bridge.

Business

Commentary: Puncturing the myth of Alan Greenspan, whose policies gave us the Great Recession

Noah Cross, the archvillain of the movie “Chinatown,” had the definitive line on how old age brings respectability. “‘Course I’m respectable,” he tells Jake Gittes. “I’m old. Politicians, ugly buildings and whores all get respectable if they last long enough.”

I wouldn’t necessarily slot former Federal Reserve Chairman Alan Greenspan into any of those categories, but the general reaction to his death Monday at age 100 puts the lie to Cross’ observation.

As much as he was revered during his nearly two decades as Fed chairman for protecting the stock market from a series of crashes and near-crashes, his obituaries take a more measured view. The headline on the Wall Street Journal’s main take on his legacy is: “The Myth of Alan Greenspan as ‘The Maestro.’”

Stripped of its academic jargon, the welfare state is nothing more than a mechanism by which governments confiscate the wealth of the productive members of a society to support a wide variety of welfare schemes.

— Alan Greenspan, writing as an Ayn Rand cultist (1966)

The Journal blames Greenspan for fostering “the great credit mania of the mid-2000s” and observes that “the music stopped in 2008, producing the panic that did so much harm to the free-market economy that Greenspan promoted.” That was the Great Recession, which started with the 2008 crash in the housing market and persisted into 2012.

That is from a publication that was more or less in accord with Greenspan’s goals of less regulation and lower taxes. His contemporary adversaries were harsher. “R.I.P. Alan Greenspan: You were charming, thoughtful, powerful, and wrong,” writes Robert Reich, who served as Bill Clinton’s Labor secretary while Greenspan led the Fed.

The Great Recession, “in which in which millions of Americans lost their jobs, their savings, and even their homes — resulted from the deregulation of Wall Street that Greenspan advocated,” Reich wrote. But he had to admit that Greenspan’s “iron grip” over Fed policy forced Clinton “to do exactly what Greenspan wanted — which was to reduce the federal budget deficit and thereby destroy much of the agenda Clinton ran on.”

It would be unfair to depict Greenspan’s influence as invariably pernicious. Social Security advocates still think highly of his work chairing the so-called Greenspan Commission of 1982-1983, which developed a series of changes in benefits and revenues for that program to address a looming, immediate fiscal crisis.

Greenspan led the bipartisan panel “masterfully,” recalls William J. Arnone, the former chief executive of the National Academy of Social Insurance, who witnessed its deliberations as a consultant to the New York Citizens Committee on Aging.

Before the commission’s formation, “Republicans and Democrats fiercely disagreed over underlying data,” Arnone told me. “Greenspan used his expertise as an economic empiricist to convince both sides to agree on a singular, shared set of actuarial facts. Quite an accomplishment.”

To the public, Greenspan was known for his impenetrably cryptic speaking style and for the relative tranquility in the American economy during his tenure, which has been termed “the great moderation” despite recurrent short-term crises.

Greenspan was the second-longest serving Fed chair. But he may have had the weirdest background. Having grown up in an affluent New York household, he was talented enough on clarinet and saxophone to have sat in with Stan Getz’s band and attended Juilliard for a time.

He began his economics education in 1945 at New York University and got as far as a master’s degree, but by then he was already working on Wall Street, where his skill at financial analysis propelled him toward the top echelons of high finance.

Somewhere along the line he fell in with the arch-libertarian Ayn Rand, becoming part of her inner circle of economic cultists. Referring to his dour mien and predilection for charcoal gray garb, Rand called him her “undertaker.”

Greenspan provided a veneer of rigorous economic analysis for Rand’s ideology, which lionized the rich and described them as fighting a ferocious battle with the lazy and grasping hoi polloi. He contributed three essays to her 1966 anthology “Capitalism: The Unknown Ideal.”

His association with Rand was seldom highlighted during his Fed tenure, but even a casual reading of those essays exposes the Randian underpinnings — and the Randian self-contradictions — of his Fed policies.

One essay defended the gold standard, which had been discredited in the 1930s. Greenspan blamed “welfare-state advocates” for the developed world’s abandonment of the gold standard.

He wrote, “Stripped of its academic jargon, the welfare state is nothing more than a mechanism by which governments confiscate the wealth of the productive members of a society to support a wide variety of welfare schemes…. Gold stands in the way of this insidious process. It stands as a protector of property rights” — language that could have come right out of the text of Rand’s “Atlas Shrugged.”

Another essay called for the dismantling of government regulators such as the Food and Drug Administration and the Securities and Exchange Commission. Greenspan’s argument was that the consumer was adequately protected by the businessman’s profit-seeking, which in turn depended on maintaining a reputation for honesty and fair-dealing.

For drug companies, he wrote, “the loss of reputation through the sale of a shoddy or dangerous product would sharply reduce the market value of the drug company.” The same goes for securities brokers — “The slightest doubt as to the trustworthiness of a broker’s word or commitment would put him out of business overnight.”

One might ask what inspired Greenspan’s faith in, well, the faithfulness of business enterprises, given centuries of proof otherwise. Anyway, he refuted his own argument. “The guiding purpose of the government regulator is to prevent rather than to create something,” he wrote. “He gets no credit if a new miraculous drug is discovered by drug company scientists; he does if he bans thalidomide.”

He didn’t bother to question why his trustworthy drug companies had tried to market as a morning-sickness drug in the U.S. a formulation that already had been shown to produce severe birth defects in the children of mothers who took it overseas. (American families were largely saved from this tragedy by Frances Oldham Kelsey, who blocked its importation as an official of, yes, the FDA.)

To stock market investors, Greenspan’s chief legacy was the “Greenspan Put.” This was an implicit commitment by the Fed to counteract sharp declines in the market by pumping liquidity into the economy through the mass purchase of Treasury bonds.

The term comes from the options market, in which a “put” gives the holder the right to sell the underlying stock at a set price in the future, even if the market price has fallen below that price. In effect, it establishes a floor to the investor’s losses in a downturn.

The Greenspan put first appeared on Oct. 19, 1987, when the stock market suffered its greatest one-day percentage crash ever, 20.47%. Greenspan had been in office for only a few weeks, but his Fed issued a statement promising to inject liquidity into the system and cut interest rates. “We will back you,” he told bankers in a series of phone calls.

In truth, Greenspan had no legal authority to make that pledge. In any event, the market recovered the next day, and the Fed’s image as a willing bulwark against market declines was born.

The problem was that the idea that the Fed would act in a market crisis encouraged ever more flagrant risk-taking on Wall Street.

The harvest was a series of crises, notably the 1998 collapse of the hedge fund Long Term Capital Management, which was founded by Nobel economics laureates to pursue abstruse arbitrage trades. It was brought low by market moves that confounded their projections. LTCM was so deeply embedded in Wall Street trading it had to be saved with a $3.6-billion bailout the Fed orchestrated.

The Greenspan put, like so many other such grand schemes, worked well right up until it stopped working. That moment came in 2008, with a crash and a long, throbbing hangover.

Testifying to Congress in 2008, Greenspan acknowledged that maybe self-regulation, that watchword of his economic worldview, didn’t work.

“I made a mistake in presuming that the self-interest of organizations, specifically banks and others, were such that they were best capable of protecting their own shareholders and their equity in the firms…. Something which looked to be a very solid edifice, and, indeed a critical pillar to market competition and free markets, did break down.”

That, he said, “shocked me.” It was a rare admission of blame by a man who, as my former colleagues Thomas S. Mulligan and Don Lee reported in their Greenspan obituary, had told CNBC a few months earlier that he had “no regrets” about his policies.

-

Lifestyle25 minutes ago

Lifestyle25 minutes agoThis mindset shift can help you get better at using up your leftovers

-

Technology35 minutes ago

Technology35 minutes agoTMD’s keyless bike lock is a $280 solution to a $60 problem

-

World40 minutes ago

World40 minutes agoAmerican rescue teams pull infant alive from rubble in Venezuela days after devastating twin earthquakes

-

Politics47 minutes ago

Politics47 minutes agoTrump scores another endorsement win with Louisiana Senate runoff victory

-

Health50 minutes ago

Health50 minutes agoNew blood test detects 90% of aggressive prostate cancer cases, beating current screenings

-

Sports55 minutes ago

Sports55 minutes ago2026 World Cup Round of 16 Odds: Which Teams Will Make It?

-

Technology1 hour ago

Technology1 hour agoApple raises prices as AI chip costs surge

-

Business1 hour ago

Wildfire rebuilding boosts L.A. County job growth in May