Business

Column: Pharmacy middlemen claim to keep prescription prices low. In fact, they've cost consumers billions

In 2022, an executive of a big pharmacy middleman firm acknowledged the noxious reality of its business model:

It was designed to massively overcharge customers by steering them to its affiliated or “preferred” pharmacies or its home delivery subsidiary.

Referring to a generic version of Gleevec, a leukemia drug taken by nearly 200,000 patients, the executive noted in an internal memo that “you can get the drug at a non-preferred pharmacy (Costco) for $97, at Walgreens (preferred) for $9000, and at preferred home delivery for $19,200…. We’ve created plan designs to aggressively steer customers to home delivery where the drug cost is ~200 times higher.”

PBMs are not lowering prices for drugs used by patients to treat severe diseases like prostate cancer and leukemia.

— Federal Trade Commission

The executive concluded, “The optics are not good and must be addressed.”

What that memo described, according to a new report from the Federal Trade Commission, is standard operating procedure among the nation’s largest pharmacy benefit managers, or PBMs.

Originally devised in the 1960s as intermediaries helping health insurers process claims, steering doctors and hospitals to the cheapest drug alternatives and giving insurers greater leverage in negotiations with drug manufacturers, they soon became just another special interest in America’s fragmented healthcare system.

Thanks to a wave of consolidation and growth of healthcare conglomerates, the FTC says, the three largest PBMs manage nearly 80% of all prescriptions filled in the U.S. They have accumulated enough power to profit “by inflating drug costs and squeezing Main Street pharmacies,” driving the independents out of business.

Once posed as an answer to high drug costs, they’re today at the hub of a system that drives up drug prices for consumers.

Starting in the 1990s, some of the biggest PBMs were acquired by drug companies, creating conflicts of interest that led to federal orders for divestment.

Then came a wave of mergers and acquisitions within the PBM universe, followed by acquisitions by insurers and pharmacy companies — CVS acquired Caremark, then the biggest PBM, in 2007 and UnitedHealth merged CatamaranRx, then the fourth-largest PBM, into OptumRx in 2015.

Between 2000 and 2021, 39 individual healthcare companies — drugstore chains, health insurers, managed care firms and PBMs — all coalesced into three healthcare behemoths, Cigna, CVS and UnitedHealth.

CVS Health Corp. owns not only the Caremark PBM, which controls 34% of the prescription market, but the insurance company Aetna and about 9,000 retail drugstores.

Cigna Group, which has a prescription market share of 23%, owns the mail-order PBM Express Scripts and the Cigna insurance company. UnitedHealth Group is the largest U.S. health insurer and owns 1,000 walk-in health clinics as well as physician groups; through its OptumRx PBM, its prescription market share is 22%.

Between 2000 and 2021, mergers and acquisitions combined these 39 independent healthcare companies into three huge conglomerates.

(Federal Trade Commission)

Along with Humana, the fourth-ranked PBM with a market share of 7%, those conglomerates produced combined revenue of $456 billion in 2016, 14% of national health spending. Today, they collect more than $1 trillion in revenue, or 22% of U.S. healthcare spending.

Despite the predictably anticompetitive effects of these mergers and acquisitions, not a single one was challenged by antitrust enforcement agencies, says the FTC — one of the antitrust regulators asleep at the switch.

Among the stratagems employed by PBMs to boost profits, the FTC says, is steering health plans and patients to their own affiliated pharmacy chains.

Some patients have discovered that their drugs won’t be covered by their insurers unless they buy them at specified pharmacies, the result of deals the PBMs have made with insurers, including those with which they share a parent. But the customers may have to pay more out of pocket at the affiliated pharmacies than they would at an independent.

The FTC staff found that for “specialty prescriptions” — a designation the PBMs place on certain drugs, often without explanation — 55% were filled at affiliated pharmacies. The same ratio didn’t occur with prescriptions under Medicare’s Part D prescription coverage, because federal law requires that those prescriptions can be filled at almost any licensed pharmacy. Only 22% of Part D prescriptions were filled at PBM-affiliated pharmacies. That suggests that PBMs may be steering patients to their pharmacies where that’s not forbidden by law.

The statistics were drawn from submissions by two of the three top PBMs, which are unidentified. The third didn’t submit the necessary data.

The FTC also touches on a relatively new wrinkle in drug pricing — rebates by drugmakers to PBMs in order to gain preferential positions in drug formularies.

The agency says its review of contracts between manufacturers and PBMs shows that some drug companies promise PBMs higher rebates if the latter exclude competing drugs from their formularies — including generic versions that are chemically identical to the brand-name products — or require prior authorization before covering the rival drugs.

Predictably, the big PBMs and their lobbyists find much to dislike in the FTC report, which the agency describes as an interim staff report, part of an investigation launched in 2022.

A spokesperson for Cigna’s Express Scripts criticized the report for “blatant inaccuracies” (but didn’t offer specifics in an email to me). A spokesman for CVS blamed drugmakers for high prescription prices, stating that an FTC effort to “limit the use of PBM negotiating tools would instead reward the pharmaceutical industry.” Optum didn’t reply to my request for comment.

J.C. Scott, president of the Pharmaceutical Care Management Assn., the PBM lobbying arm, accused the FTC of advancing “pre-determined conclusions … irrespective of the facts or the data.”

Drawing from more than 1,200 comments submitted by stakeholders in healthcare and by other members of the public, the agency outlined a host of methods PBMs are accused of using to benefit their affiliated services, block patient access to inexpensive generics and pocket discounts that should properly go to customers.

The FTC also mined lawsuits, including a 2023 case the state of Ohio filed against Express Scripts, charging that the PBM exploits its knowledge that “Ohioans in need of medication, particularly life-saving medication, will pay the asking price. The choice is binary — pay or suffer.”

Drug manufacturers capitulate to the PBMs’ rebate demands, the lawsuit says, to avoid being dropped from the PBMs’ formularies, the rosters of drugs that they’ll cover. “Patients pay more, manufacturers get less, and the PBMs profit. Handsomely.”

PBMs have been the targets of drug industry participants for years — sometimes fingered by drugmakers or insurers to deflect accusations that they’re responsible for prescription drug inflation.

It may be true that all those entities share the blame for high prices. Over the last couple of decades, however, all have become tentacles of the same octopus. The consolidation of drug chains, physician groups, insurers and PBMs into conglomerates has made it much harder to identify responsibility for drug inflation.

Contracts between PBMs and unaffiliated pharmacies, the FTC says, are “opaque, complex, and conditional, making it challenging to understand what pharmacies will ultimately be paid for any given drug.” The result is that smaller, nonchain pharmacies may get pushed out of the market, “leading to higher costs and lower quality services for people around the country.”

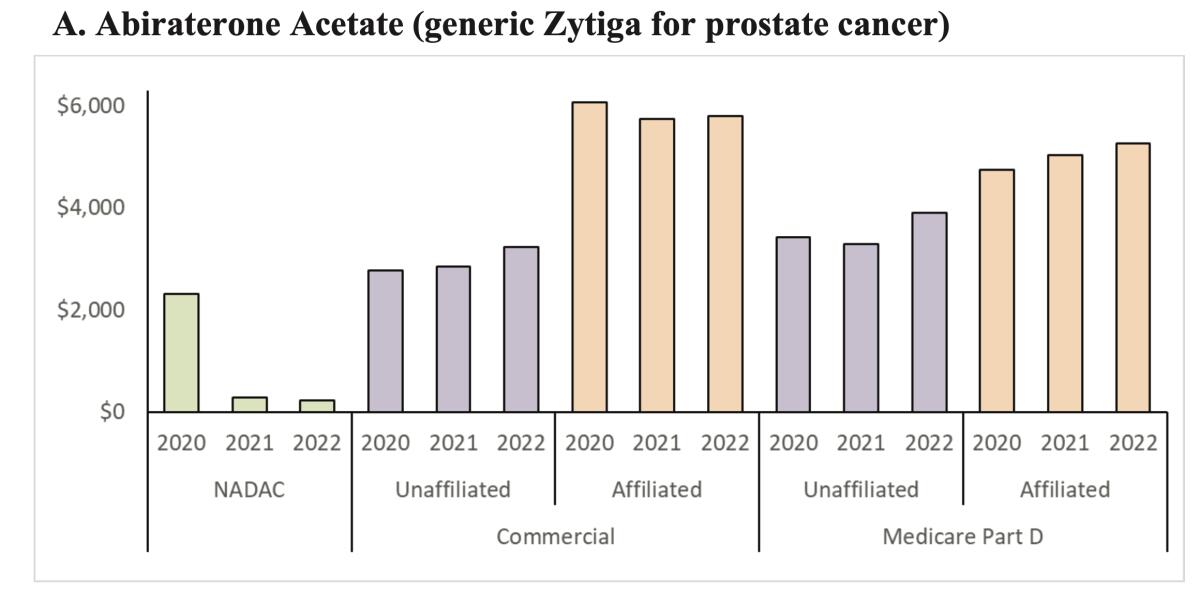

The FTC report offers two case studies involving generic cancer drugs in which the agency says PBMs reimbursed their affiliated pharmacies more for prescriptions than unaffiliated pharmacies, yielding nearly $1.6 billion in gross profits from 2020 through mid-2022 for those affiliated pharmacies over the national average of those drug costs.

The drugs are a generic version of Zytiga, a treatment for prostate cancer, and a generic for Gleevec, a drug for leukemia. The high reimbursement rates for druggists dispensing those drugs may “translate into high out-of-pocket costs for patients,” the FTC says. In other words, “PBMs are not lowering prices for drugs used by patients to treat severe diseases like prostate cancer and leukemia.”

Magnify the gains on those two drugs by the potential profits the PBMs may be extracting from the entire spectrum of prescription pharmaceuticals, and the toll becomes breathtaking.

Prices that PBMs paid affiliated pharmacies for the generic version of prostate cancer drug Zytiga were much higher than they paid independent pharmacies, and much higher than the national average cost. As a result, patients may have been charged much higher co-pays at the affiliates — but may not have had any other option.

(FTC)

“It appears that PBMs are having the commercial health plans and Medicare Part D prescription drug plans they manage pay their affiliated pharmacies rates that are grossly in excess” of national average prices or prices paid to unaffiliated pharmacies.

No one escapes the consequences of this sort of market manipulation. The internal transactions, largely hidden from the public and regulators, may distort the statistics that health plans submit to the government to show they meet the coverage standards required by the Affordable Care Act, allowing the conglomerates to “game” the rules, the FTC says.

They may drive up healthcare costs for self-insured clients such as large companies, which may pare back health coverage for their employees as a result.

They can raise co-pays for patients, lead to cutbacks in the availability of coverage for some drugs, or prompt patients to ration their prescriptions, risking their health to save money. To the extent they affect Part D, they may drive up government spending.

To quote the Ohio lawsuit, PBMs were created as a counterweight to perceived profiteering by Big Pharma. But once they “grew powerful enough to themselves extract exorbitant fees … the solution became the problem.”

The FTC says it issued its interim report because several PBMs haven’t provided the agency with the information they’re required to submit, hindering its ability to complete its investigation.

At the very top of the report, the FTC warns that the firms better come across “promptly,” or they’ll be taken to court. The FTC should start suing now, because the PBMs’ apparent code of silence raises a familiar question: What must they be hiding?

Walmart is rapidly expanding its network of electric vehicle chargers designed for customers to use while they shop.

The network could help fill gaps in EV infrastructure in states with greater need for chargers. Walmart, which has more than 5,000 locations in the U.S. and hundreds in California, says more than 90% of Americans live within 10 miles of one of its stores.

The chargers also offer an incentive for customers to choose Walmart — Walmart Plus members will receive a 10% discount off an average price of $0.46 per kilowatt-hour of energy at the company’s chargers.

Walmart chargers are already available at more than 75 locations in 17 states, with Texas boasting the most charging stations, followed by Florida and Arizona.

Matthew Nelson, Walmart’s director of energy policy, said last week on LinkedIn that the network will soon reach 29 states, including California.

“We are delivering on the promise of affordable, reliable and convenient charging,” Nelson said in his post.

According to Walmart’s website, six charging stations are coming to California soon, though the company did not offer a specific timeline.

The chargers will be installed at stores in Antelope, Brea, Fresno, Stockton, Suisun City and Vallejo.

Most charging sites in California will include eight to 16 fast-charging stalls, said Walmart spokesperson Kelsey Bohl.

The company first announced plans in April 2023 to install its own EV chargers at Walmart and Sam’s Club stores, with a goal of installing thousands of chargers by 2030. Partnering with ABB E-Mobility and Alpitronic, it added 25 new charging sites this past May and six more in June.

“Walmart is building a leading retail-integrated EV fast-charging network, focused on delivering an affordable, reliable and convenient charging experience where customers already shop,” Bohl said in an emailed statement. “Customers can charge while they shop, access stations through the Walmart app they already use, and benefit from affordable pricing.”

The charging stations already available include 612 individual charging stalls using 400-kilowatt chargers. Each stall has a dual charging cord with both Combined Charging System and North American Charging Standard connectors. The standard connectors, designed by Tesla, are smaller and lighter than the combined systems.

The primary way to pay for the chargers is through the Walmart app, but the company is also experimenting with built-in credit card readers to allow those without the app to use the stations.

Customers can check charger availability on the Walmart app. The company said the chargers will be available 24 hours a day.

Robotaxis could be turning into robocops.

A self-driving Waymo reported two teens to San Mateo, Calif., police on Monday after they were found drinking alcohol and shooting toy guns in the back of the vehicle.

According to a social media post from the San Mateo Police Department, officers detained two 15-year-olds after the Waymo they were riding in contacted the department and stopped in a parking lot until law enforcement arrived.

“Parents do you know where your teens are?” the San Mateo Police Department wrote on Facebook following the incident. “Waymo does!”

Officers removed both teens from the vehicle and determined they were using toy guns to shoot Orbeez out the windows. Orbeez are small, water-absorbing beads sold at toy stores.

“Toy guns, water guns, and BB guns all pose real dangers, especially to an untrained eye,” the Police Department said. “The simple handling of them can cause fear in [passersby].” “

A video posted on Facebook shows at least five officers and a police dog responding to the scene and approaching the Waymo with their weapons raised.

Waymo did not immediately respond to a request for comment.

Waymo vehicles have internal cameras and microphones that may be used in an emergency or to “promote safety and security,” according to Waymo’s online support page.

The cameras are also used to ensure the vehicles are clean and to help find lost items, according to the support page.

The company said it does not use facial recognition or other biometric identification technologies to identify individuals.

“In more urgent circumstances, support may access live video during a trip,” the Waymo page said.

The San Mateo Police Department’s Facebook post has garnered nearly 60 comments, with one user accusing Waymo of “snitching.”

“At least they got a designated driver?!” one user commented.

Business

Commentary: How right-wing anti-transgender attacks led to a Supreme Court ruling upholding sex discrimination

At the Supreme Court, the unfounded fear of boys masquerading as girls in youth sports rolled the clock back on gender equality.

On the surface, the Supreme Court’s June 30 opinion upholding state laws barring transgender girls from women’s and girl’s sports teams looks like a victory for women’s rights.

The 6-3 opinion by Justice Brett M. Kavanaugh certainly presents itself that way. “Females and males have inherent physical differences relevant to athletic performance,” Kavanaugh wrote. “Therefore, in contact sports, forcing female athletes to compete against males can create significant safety risks.” He also asserted that “forcing female athletes to compete against males can undermine competitive fairness.”

The ruling applied to prohibitions enacted in Idaho and West Virginia against “biological” males’ participation on women’s teams in public schools. Federal judges in both states overturned the bans. The Supreme Court majority restored them. The ruling essentially upholds similar bans enacted in 25 other states.

There was no record of any transgender person participating in school sports in the State, let alone any ‘problem’ with transgender students … creating unfair competition or unsafe conditions.

— Justice Sonia Sotomayor, demolishing the Supreme Court’s argument in favor of banning transgender girls from girl’s sports

Kavanaugh, like Donald Trump and others in the anti-transgender camp, maintained that one’s gender is an immutable fact of life, established even before birth.

Anything else, Trump stated in an executive order he issued on inauguration day 2025, could only be the product of “gender ideology extremism.” The U.S., his order stated, recognizes “two sexes, male and female. These sexes are not changeable and are grounded in fundamental and incontrovertible reality.” That’s a “biological truth,” he declared.

In his own version of this overconfident and factually insupportable conclusion, Kavanaugh wrote: “As all agree, females and males have inherent physical differences relevant to athletic performance.”

Science recognizes that some people are “born with sex traits that don’t fit into typical male or female patterns,” to cite a discussion on the Cleveland Clinic web page on the topic “intersex.” The condition “may involve chromosomes, hormones, reproductive organs or genitals.”

From a psychological standpoint, medical science recognizes “gender dysphoria” as a real condition often requiring counseling and medical intervention such as the use of puberty blockers and hormones to stave off the development of secondary sex characteristics until the condition can be resolved.

No one disputes that there are physical differences between the sexes. Few would dispute that on average or even at the median, males may be bigger and more powerful than females, or that in certain contact sports the difference may be telling and on occasion dangerous.

But that’s not the same as asserting that the physical differences between males and females invariably mean that men will invariably prevail over women in all competitions or that their participation will endanger women.

The International Olympic Committee — in a policy statement Kavanaugh cited incompletely — says that in “most running and swimming events,” males have a 10% to 12% advantage over women. That’s a range that would accommodate the full spectrum of outcomes — transgender females win, cisfemales win, they tie. (The “cis” prefix denotes those living consistent with their birth gender.)

West Virginia and Idaho addressed this ambiguity by banning transgender women from all girls’ teams. So under their rules transgender girls can’t play football or soccer with cisgirls. But what’s the argument in favor of banning them from the 100-yard dash, or cross-country track, or diving, or archery?

But something else is going on here. The Supreme Court’s ruling was almost preordained, given the years-long campaign by conservatives to demonize transgender individuals as if they’re members of an alien species.

It will be recalled that during his presidential campaign, Trump spun a despicable fantasy in which children were kidnapped in school and secretly subjected to sex-change operations.

Trump’s executive order wiped out policies aimed at protecting transgender adults from discrimination. He moved to outlaw gender-affirming medical therapies for anyone under 19 by cutting off federal funding for healthcare institutions that provide such care.

He banned transgender individuals from serving in the military and ordered federal prison officials to move transgender inmates into the general populations consistent with their birth genders, which exposes them to physical assault. (Federal Judge Royce Lamberth of Washington, D.C., has blocked the government from transferring three transgender women into the male prison population or terminating their hormone treatments.)

I wrote during Trump’s first term, when his anti-transgender policies were still gestating, that the goal was to show that “one can target any community, as long as it doesn’t have a strong political voice or political power. These are the actions of bullies and cowards, pretending to be strong.”

Last year, the Supreme Court struck its first blow against transgender rights by upholding a Tennessee law banning transgender care, including puberty blockers and hormone therapy, for minors. Similar laws have been enacted in 25 other states. The majority in that ruling by Chief Justice John G. Roberts Jr. was identical to the one in the June 30 ruling — Roberts, Kavanaugh, and Justices Clarence Thomas, Samuel A. Alito Jr., Neil M. Gorsuch and Amy Coney Barrett.

Who are the targets of this ideological campaign? They number only about 1.6 million U.S. adults, or one-half of 1% of the U.S. population. About 300,000 adolescents ages 13 to 17, or 1.4%, identify as transgender, according to a study by UCLA School of Law.

In West Virginia, as Justice Sonia Sotomayor observed in her dissenting opinion, “there was no record of any transgender person participating in school sports in the State, let along any ‘problem’ with transgender students … creating unfair competition or unsafe conditions.”

In endorsing the flat bans directed at transgender women in Idaho and West Virginia, Kavanaugh argued that any attempt to implement case-by-case judgments of students’ requests to join sports teams inconsistent with their biological gender would create “an enormous practical and administrability problem.”

Is that so? That wasn’t the case in Maine, where the annual K-12 population is more than 170,000. There, a committee was charged with determining whether a student’s participation in a sport consistent with their gender identity but inconsistent with their biological sex would “result in an unfair athletic advantage” or present a risk of injury to others. The committee held 56 hearings from 2013 through 2021, or an average of seven per year. During the entire time span, only four involved transgender girls. (The outcome of those hearings couldn’t be learned.)

It was Maine’s policy, one might recall, that provoked a confrontation between Trump and Maine Gov. Janet Mills at the White House last year, when Trump threatened to withhold federal funding from the state unless it barred transgender students from competing on women’s sports teams. “We’ll see you in court,” Mills snapped.

Whether the Idaho and West Virginia laws genuinely protect girls from unfair competition is questionable. (The Idaho law is styled the “Fairness in Women’s Sports Act.”) In practice, the laws may subject women in public schools to “invasive sex verification procedures,” as educational expert George Theoharis of Syracuse University wrote after the court ruling.

They’re also based on a retrograde view of women as fragile creatures needing men’s protection, Theoharis wrote — “the same logic that has historically been used to justify excluding women from making their own healthcare decisions and girls from rigorous math and science; that physically demanding work is simply beyond them.” (There don’t appear to be any state laws barring transgender women from competing in men’s sports.)

Becky Pepper-Jackson, the plaintiff in the West Virginia case, in which she is identified only as B.P.J., is the only transgender girl who sought to join girl’s teams — track and cross-country — in the state. That was in 2021, just after West Virginia passed its law and she was about to enter sixth grade. She didn’t appear to pose any competitive risk to others on the track and cross-country teams she applied to join — her lawyers told the Supreme Court that on those no-cut teams, she “came in near the back.”

Anyway, she had not gone through male puberty, which theoretically might have endowed her with a competitive advantage, because she had been taking puberty blockers and female hormones.

Thanks to the court’s ruling, Sotomayor observed in a dissent joined by Justices Elena Kagan and Ketanji Brown Jackson, West Virginia can deny Becky access to school sports “because it thinks they have an inherent athletic advantage, even if the facts show that they do not.”

B.P.J., Sotomayor wrote, “cannot practice on girls’ teams, even if she would not take anyone’s spot in an eventual competition, even if everyone who tries out for the team makes it, and even if having the chance to participate could aid immensely in treating B. P. J.’s gender dysphoria.”

So whose interest was really protected by the Supreme Court?

-

Finance20 seconds ago

Finance20 seconds agoHow Natura &Co Is Transforming Finance with Generative AI on SAP S/4HANA

-

Fitness5 minutes ago

Fitness5 minutes agoThis 30-second walking habit can make every walk more effective and boost your fitness in less time

-

– Awards Radar")

– Awards Radar") Movie Reviews16 minutes ago

Movie Reviews16 minutes agoFilm Review: ‘Gail Daughtry and the Celebrity Sex Pass’ Throws a Ton of Jokes at the Wall (and Enough Stick) – Awards Radar

-

World31 minutes ago

World31 minutes ago‘The Kitchen’ Director Alonso Ruizpalacios at BAM: ‘We Need More Trojan Horses’

-

News36 minutes ago

News36 minutes agoManhattan Building’s Columns Buckled Beneath New Addition, Images Show

-

Lifestyle1 hour ago

Lifestyle1 hour agoCan you say no to a friend’s wedding? : It’s Been a Minute

-

Technology1 hour ago

Technology1 hour agoThe robotaxi law that could ban Tesla

-

World1 hour ago

World1 hour agoUS urges donors to abandon UNRWA funding as UN defends agency’s mission