Crypto

FBI probe reveals Turkey as key conduit for ISIS cryptocurrency funding – Nordic Monitor

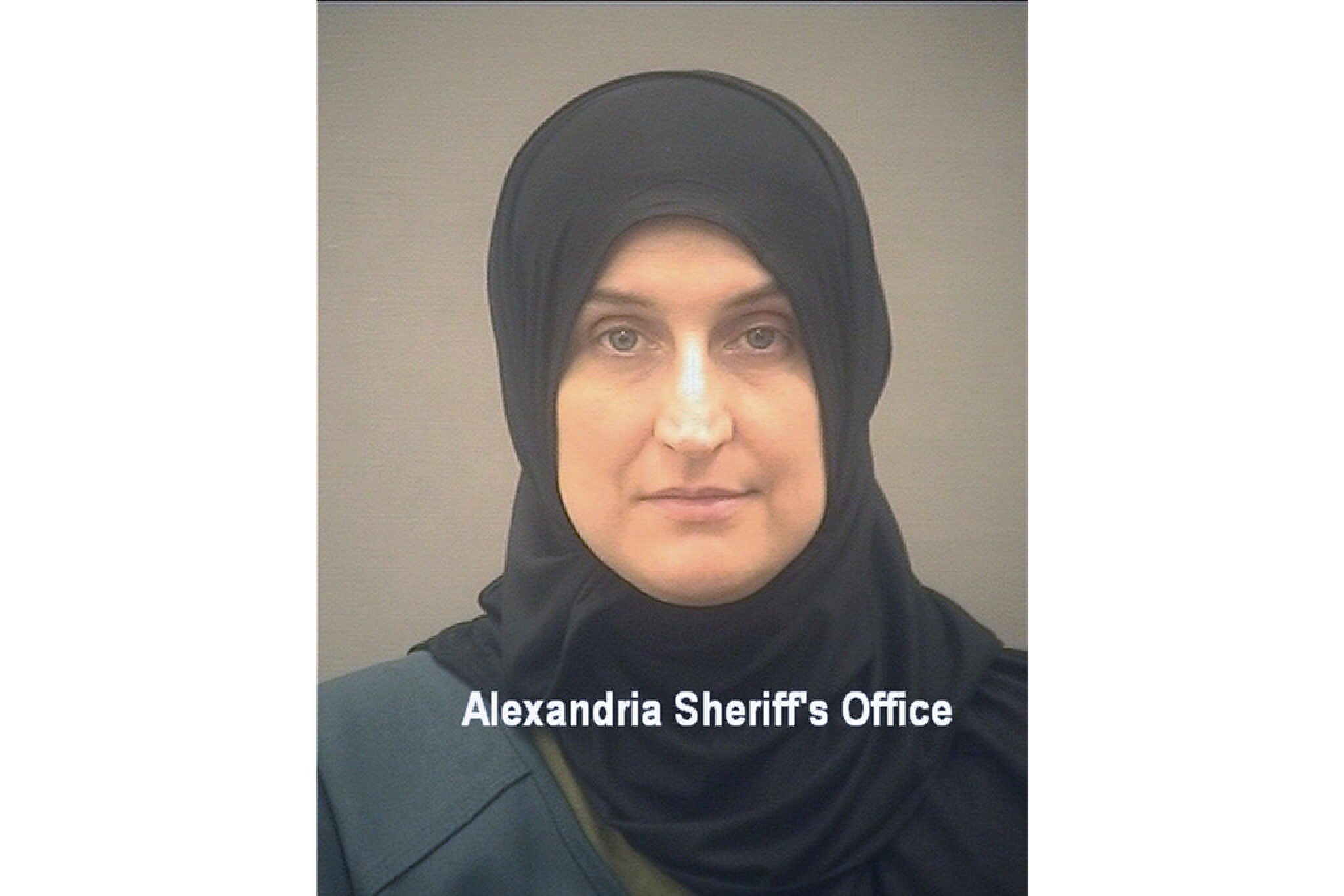

Abdullah Bozkurt/Stockholm

The indictment of an American citizen, prosecuted for funding the Islamic State in Iraq and Syria (ISIS), has exposed how Turkey became a key conduit for illicit cryptocurrency transactions used to finance the jihadist group’s operations in Syria.

Mohammed Azharuddin Chhipa, a 35-year-old Virginia resident and naturalized US citizen originally from India, transferred over $188,000 to ISIS. The funds were used to help secure the release of ISIS fighters and their families in Syria, utilizing Turkish intermediaries and cryptocurrency.

In an affidavit submitted to U.S. Magistrate Judge Lindsey R. Vaala on May 4, 2023, FBI Special Agent Gary T. Marosy explained that funds sent to ISIS in Syria often followed this method through Turkish brokers. The money was transferred via cryptocurrency, a difficult-to-trace form of currency, to couriers in Turkey. These couriers would then convert the cryptocurrency into cash, which was secretly smuggled into Syria without leaving a trace.

Intercepted communications revealed that Chhipa’s contact in Syria advised him not to send money directly to Syria or elsewhere, but rather to route it through Turkey, where ISIS could safely collect the cash and redirect it to fund their operations in Syria.

Chhipa, an IT professional who has lived in the US since the age of four after his family emigrated from India, was flagged by the FBI in 2019. The law enforcement agency was alerted when a dozen social media accounts he managed began posting violent jihadist messages.

Affidavit submitted to U.S. Magistrate Judge Lindsey R. Vaala on May 4, 2023 by FBI Special Agent Gary T. Marosy:

Chhipa_affidavit_FBI

In a post dated March 18, 2019 he wrote: “The sword is a must. Jihad is a must. Nothing terrifies the enemies – the enemies of the Muslimin– nothing terrifies them like power, force and, weapons…Jihad is a brick and solid pillar of the Shari’ah…This din [religion] can not be established and firmly planted without jihad, ever.”

On the same day, in another post, Chhipa quoted Shaykh al-Allamah Humud Ibn Ulqa ash-Shu’aybi, a renowned radical Saudi cleric who was supportive of the Afghan Taliban and the September 11, 2001 attacks.

In a chat conversation on March 16, 2019 Chhipa said he would either end up in prison, engage in jihad by moving abroad or become a martyr by killing himself. In June 2019, during communications with a covert FBI-run social media account, Chhipa admitted his support for ISIS and expressed his desire to carry out an attack against what he referred to as infidels and hypocrites, hoping to die in the name of Allah.

Chhipa fled the country on August 2, 2019, believing he would be arrested following an FBI search warrant executed at his home. The US secured a blue notice through INTERPOL, requesting assistance in locating, identifying or obtaining information about him in connection with a criminal investigation. Chhipa was forced to return to the US before reaching Egypt, part of his planned multi-route escape through Mexico, Guatemala, Panama and Germany. He was detained near the Mexican-Guatemalan border and deported to the US by Mexican authorities on August 16, 2019.

The FBI uncovered a cache of evidence during the search, which included instructions for building a bomb, PDF copies of the ISIS publication Dabiq and photos depicting beheadings and armed ISIS fighters.

After returning to the US without facing charges, Chhipa believed he was in the clear and resumed his activities on behalf of ISIS. He frequently communicated with British ISIS women living in Syria who were funding ISIS fighters and assisting in the escape of their family members from the Al Hawl camp (also known as Al Hol).

The camp was established in 2016 to house Iraqis and Syrians fleeing ISIS-controlled areas. By March 2019 over 50,000 women and children had settled in a special section of the camp known as the annex, following the final defeat of ISIS by the US-led coalition. The annex is guarded by Syrian Democratic Forces (SDF) fighters, who are reportedly open to bribes to allow ISIS family members to escape the camp.

The annex continues to serve as a stronghold for ISIS ideology, operating under strict Islamic sharia law similar to that of ISIS. The SDF is considered a terrorist organization by Turkey due to their alleged ties to the Kurdistan Workers’ Party (PKK), which is designated as a terrorist group by the US, the EU and Turkey.

Beginning in November 2019, Chhipa started depositing cash into his Apple Federal Credit Union bank account, converting the funds into cryptocurrency through service providers Coinbase and Binance, and sending them to Turkey.

The FBI’s analysis revealed that over $18,000 was sent to cryptocurrency wallets associated with ISIS women in Syria, $61,000 went to wallets located in Turkey, and more than $60,000 remains unaccounted for.

US Government’s Memorandum in Support of Pre-Trial Detention for Mohammed Azharuddin Chhipa, an ISIS Suspect:

US_attorney_motion_for _detention_ISIS-suspect

In a communication obtained by the FBI, an ISIS member advised Chhipa never to send money directly to her, but rather through Turkey. “Never sent directly to me it[’]s always sent to [T]urkey and then secretly sent to me with no tracks,” she wrote, prompting Chhipa to reply by saying that “I know how it works.”

The FBI used several covert accounts to communicate with Chhipa and his ISIS contact in Syria through what is known as FBI Controlled Persona (FBICP), which refers to accounts operated by undercover agents or confidential human sources. This communication was instrumental in deciphering the scheme Chhipa was running for ISIS.

In late April 2023 the FBI placed Chhipa under close surveillance, which he noticed, prompting him to attempt to flee the country for a second time. He received tips from an unidentified person with a German phone number on how to avoid detection. When he withdrew $8,000 in cash from his bank account, the FBI concluded that he was planning to escape.

Chhipa was arrested by the FBI on May 4, 2023 on an arrest warrant charging him with providing material support to ISIS, a crime that carries a potential penalty of up to 20 years in prison and possibly a lifetime of supervised release. He was detained pending trial on May 10, 2023.

During a May 2023 hearing, Assistant US Attorney Anthony Aminoff revealed that Chhipa had a relationship with Allison Fluke-Ekren, an American ISIS member from Kansas who is currently serving a 20-year sentence. Fluke-Ekren pleaded guilty in 2022 to organizing and leading Khatiba Nusaybah, a battalion where approximately 100 women and girls were trained in the use of automatic weapons, grenades and suicide belts. The two married through an online encounter, and Chhipa had been attempting to adopt Fluke-Ekren’s children.

Chhipa’s case underscores how the government of President Recep Tayyip Erdogan appears to tolerate ISIS activities in and through Turkey, rather than genuinely cracking down on the terrorist network. Official figures indicate that only about one in four ISIS detainees is arrested during arraignment in Turkish courts, effectively creating a revolving door policy for ISIS suspects.

Many ISIS suspects who were arrested are later released during trial hearings, and very few actually receive convictions and serve prison time. The Turkish government avoids disclosing how many ISIS members have been convicted, despite parliamentary inquiries from opposition parties.

For years, the Erdogan government turned a blind eye as ISIS moved fighters, funding and logistical supplies through Turkey. During 2015-2016, Turkish intelligence agency MIT reportedly contracted the ISIS network in Turkey to carry out a series of violent bombings to further a political agenda and help the Erdogan government maintain power amid increased terrorist threats during election cycles.

Key Takeaways

- Dragonfly’s Rob Hadick says stablecoins could grow 10x as payments adoption accelerates.

- Tether and Circle are shifting from reserve yield toward payments and financial rails.

- Hadick expects USDT and USDC to face rising competition from banks and fintechs.

Stablecoins and the Fall of Legacy Payments

For years, the stablecoin market has been viewed through the lens of issuance. The most visible winners have been the companies minting the assets, holding reserves, and benefiting from interest income. But Rob Hadick, General Partner at Dragonfly, believes that view is too narrow for where the market is heading.

In Hadick’s view, stablecoins do not simply improve the existing payment system. They compress much of it.

“ Stablecoins collapse the legacy payment infrastructure and reduce the dependency on intermediaries,” Hadick said. “When you’re a stablecoin native, everything is just a book transfer.”

That shift changes where value accrues. In the traditional payments system, value was spread across banks, card networks, processors, settlement layers, compliance vendors, and middleware providers. Stablecoins make many of those roles less necessary, or at least less defensible.

The result, Hadick argues, is an inversion of the 2010s fintech playbook. During that era, major companies were built by creating connections between software startups and legacy banking payment rails. In the stablecoin era, the opportunity is not simply connecting to those legacy banking payment rails. It is replacing them.

That means in the future, the most valuable businesses may sit at the edges of the system: the companies that own customer distribution, merchant relationships, compliance workflows, banking access, and regulatory infrastructure.

From Reserve Yield to Payments

Within the stablecoin vertical of crypto, stablecoin issuers have been the clearest winners so far. Tether and Circle built large networks, accumulated liquidity, and benefited from high interest rates on reserves, which they haven’t had to pass on to users. That model has proven powerful, especially while rates remain elevated.

But Hadick does not expect reserve yield alone to define the next stage of the market. “Going forward, both have started investing heavily in moving from asset management models to payment models,” he said.

That transition is already visible. Hadick pointed to Tether’s investments in companies and ecosystems such as Whop, Transfi, Rumble, and Plasma, while Circle has launched the Circle Payments Network and Arc. These moves suggest that the largest issuers understand the limits of being purely reserve-backed asset managers. In other words, issuance was the first business model, but it will not be the final one.

The Full Stack Starts to Collapse

One of the largest open questions is what the winning stablecoin companies will actually look like. Will they resemble banks, software platforms, payment networks, protocols, or something else entirely?

Hadick answers that today’s market contains all of the above. But he believes stablecoins create room for a new kind of company that blends several financial functions into one.

Imagine a company issuing its own stablecoin, serving users directly, handling merchant settlement, and performing identity, fraud, and compliance checks on an open ledger. In that world, the need for separate issuing banks, merchant banks, card networks, clearing systems, and settlement intermediaries begins to shrink.

“You don’t need both an issuing and merchant bank,” Hadick said. “You don’t need the card network if the merchant and consumer are already known to the provider. You don’t need the network to facilitate clearing and settlement.”

For Hadick, the winners will not be simple network aggregators sitting in the middle. They will be companies that control the last mile, solve compliance problems, face customers directly, and take real operational responsibility.

Where Retail Investors Can Partake

Hadick remains strongly bullish on stablecoin growth. “ Stablecoins are here to stay,” he said. “I think they’re going to grow tenfold.”

He pointed to an estimate from McKinsey that stablecoins account for roughly 3% of cross-border payments, up from almost nothing a year earlier. Hadick expects that share to continue rising sharply.

As for retail investors, Hadick believes the investment map is not just about who issues the token; it is about who owns the flow.

Overfunded Middleware and Crowded Consumer Fintech

Not every part of the stablecoin market looks equally attractive. Hadick is particularly skeptical of aggregated API (application programming interface) platforms that simply wrap or connect third-party services without taking on compliance or operational risk themselves. These companies may be able to charge high fees today, but Hadick believes their margins are vulnerable.

“They call themselves ‘Plaid for stablecoins,’ forgetting that blockchains already solve many of the original pain points Plaid solved for traditional banking,” he said.

The critique is straightforward. If a company is only aggregating APIs and not owning the customer, compliance layer, liquidity, or operational burden, it may be squeezed as the market matures. To remain valuable, these platforms may need to move closer to the end customer or take on more of the stack.

Hadick also sees risk in consumer fintech. Stablecoin infrastructure makes it easier than ever to launch a neobank or payment app. But that accessibility creates a crowded field.

Established brands such as Nubank, Robinhood, and Revolut can add stablecoin features to existing user bases. That makes it difficult for new consumer startups to stand out unless they offer a clear wedge, strong distribution, or a differentiated regional use case.

Hadick expects failure rates in this category to be high. Still, he does not dismiss the sector entirely. A small number of consumer fintech winners could become large global businesses if they solve real customer problems and use stablecoins as infrastructure rather than branding.

The biggest winners so far may not be the final winners. As the stack collapses, the real value will move toward the companies that own users, flows, compliance, and trust.

The Delaware House of Representatives has passed a bill that would prohibit the operation of cryptocurrency ATMs across the state, citing growing concerns over fraud and consumer protection. The legislation, now headed to the state Senate for consideration, would require all existing crypto ATMs to be shut down and removed within 90 days of enactment.

What the Bill Proposes

House Bill 123, as reported by Decrypt, targets the proliferation of cryptocurrency kiosks that have become common in convenience stores, gas stations, and other retail locations. Lawmakers argue that these machines are increasingly used to facilitate scams, particularly targeting elderly and vulnerable residents who may not fully understand the technology. The bill would make it illegal to operate, maintain, or permit the installation of a cryptocurrency ATM anywhere in Delaware.

Why This Matters for Consumers

Cryptocurrency ATMs allow users to buy or sell digital currencies like Bitcoin using cash or debit cards. While legitimate users appreciate the convenience, regulators have flagged them as high-risk for money laundering and fraud. The Federal Trade Commission has reported a surge in scams where victims are directed to deposit cash into these machines under false pretenses. Delaware’s proposed ban reflects a broader state-level push to rein in unregulated crypto financial services.

Similar Actions in Other States

Delaware is not alone in taking a hard line. Indiana, Tennessee, and Minnesota have previously enacted comparable restrictions or outright bans on crypto ATMs. These measures often include licensing requirements, transaction limits, and mandatory disclosures. The trend signals a growing skepticism among state legislators about the consumer safety risks posed by unmonitored crypto kiosks.

What Happens Next

The bill now moves to the Delaware State Senate, where it will undergo committee review and potential amendments. If passed, Delaware would join a small but growing list of states with explicit bans. Industry advocates argue that such laws could stifle innovation and push transactions underground, while consumer protection groups praise the move as necessary to prevent financial harm.

Conclusion

Delaware’s legislative action highlights the ongoing tension between cryptocurrency adoption and consumer safety. As the bill advances, stakeholders on both sides will be watching closely. For now, the message from Dover is clear: protecting residents from crypto-related fraud is a priority that may outweigh the benefits of unregulated ATM access.

FAQs

Q1: What is a cryptocurrency ATM?

A cryptocurrency ATM is a kiosk that allows users to buy or sell digital currencies like Bitcoin using cash, debit cards, or other payment methods. Unlike traditional ATMs, they are not connected to a bank account.

Q2: Why does Delaware want to ban crypto ATMs?

Lawmakers cite a rise in fraud cases, especially among seniors, where scammers trick victims into depositing cash into these machines. The bill aims to eliminate this vector for financial exploitation.

Q3: What happens to existing crypto ATMs in Delaware if the bill becomes law?

Operators would have 90 days to shut down and remove all machines. Failure to comply could result in penalties. The timeline is designed to give businesses a reasonable window to adjust.

Key Takeaways

Word Play With a Warning

Robert Kiyosaki, the author of the best-selling personal finance book “Rich Dad Poor Dad,” is recasting a familiar piece of investing advice. In a post on X, he argued that many investors only believe they are protected, adding:

“De-Worse-ified means they think they are diversified, but they have all their diversified assets, such as gold, silver, Bitcoin, stocks, bonds, real estate, and oil, in one asset class.”

His point is that spreading money across many holdings does not help if those holdings all move the same way in a crisis. When a liquidity shock hits, correlations rise and supposedly diverse portfolios can fall in unison, leaving investors “de-worsified” rather than diversified.

The commentary is consistent with the stance Kiyosaki has pushed throughout 2026 as he recently named bitcoin among the safest investments for the year, grouping it with what he calls real assets. He has repeatedly listed gold, silver, oil, food, bitcoin, and ether as his preferred holdings, framing them as scarce stores of value that printed money cannot dilute.

He has paired that view with stark price calls, setting a target of $250,000 for BTC by year’s end alongside a longer-term goal of $1 million. At current levels, the move would require a gain of more than 230%. On the precious metals side of things, he recently suggested a possible $200-per-ounce silver level this year, calling the metal’s climb a signal of mounting financial stress.

Kiyosaki’s broader thesis is darker still, warning investors of a historic market crash that he ties to surging global debt and fragile private credit markets, urging followers to build income streams, learn trade skills, and accumulate hard assets before the storm.

Timing Is Everything

The “de-worsified” warning arrives at a tense moment for markets, especially as bitcoin posted its worst week since the 2022 collapse of Sam Bankman-Fried’s FTX exchange, sliding below $60,000 as record exchange-traded fund (ETF) outflows and risk-off sentiment gripped the sector.

That is exactly the kind of broad drawdown scenario (where bitcoin, equities, and other assets fall together) that Kiyosaki has used time and again to illustrate his point.

That said, he has become an increasingly polarizing voice within the broader economic landscape, with skeptics pointing out that his crash predictions are frequent and his price targets aggressive (and that he has issued similar warnings for years). Supporters argue his core message of owning scarce assets, avoiding hidden correlation, and preparing for volatility is a reasonable hedge against an era of heavy money printing and rising debt.

Whether or not his $250,000 bitcoin call lands, the distinction he is drawing is a real one, as true diversification really does depend on owning assets that behave differently (not simply owning many of them). In a market where everything from gold to crypto to stocks can move on the same macro headlines, that lesson may matter more than any single forecast.

-

Wisconsin1 minute ago

Wisconsin1 minute agoThousands remain without power after Wisconsin storms

-

West Virginia4 minutes ago

West Virginia4 minutes agoWest Virginia residents oppose proposed transmission line at public hearing

-

Wyoming9 minutes ago

Wyoming9 minutes agoWyoming Highway Patrol launches “Citizen Connect” interactive data searching website | News

-

Crypto16 minutes ago

Crypto16 minutes agoDragonfly’s Rob Hadick Says Stablecoins Could Grow 10x as Payments Adoption Expands

-

Finance19 minutes ago

Finance19 minutes agoBezant secures $7m financing package for Namibian copper project

-

Fitness24 minutes ago

Fitness24 minutes agoNew gym opening in Woodbury uses AI to help people rethink their workout

-

Movie Reviews34 minutes ago

Movie Reviews34 minutes agoJinsei Review: Traveling Over Many Years and Many Names • The Austin Chronicle

-

World46 minutes ago

Anthropic pledges $200 million to research AI’s economic impact as CEO suggests job loss solutions