Finance

Flexport juices trade finance program with $200M credit line from KKR

Flexport Capital, the commerce finance arm of third-party logistics supplier Flexport, introduced Thursday it has secured a $200 million credit score facility from insurance coverage accounts managed by international funding agency KKR to help continued geographic growth and improvement of extra monetary merchandise.

Flexport’s suite of monetary providers offers importers and exporters with entry to working capital for stock and logistics bills. Suppliers usually require upfront cost for items that may be caught on the water and land terminals for months earlier than they are often offered to generate money.

Flexport mentioned demand for commerce finance is excessive now with many companies sitting on an excessive amount of stock and struggling to pay distributors due to rising provide chain prices. An in-house financing line additionally offers a liquidity possibility for shippers because the economic system slows and lenders tighten entry to credit score.

The KKR (NYSE: KKR) credit score facility is the primary exterior funding for Flexport Capital since its inception in 2017. Flexport has financed over $1 billion in invoices for greater than 500 cargo house owners in additional than 20 nations, with practically 150% year-over-year progress in its portfolio dimension. This 12 months it has expanded its mortgage choices to clients in 5 new areas: Canada, U.Okay., Netherlands, Belgium and Luxembourg.

As a digital freight forwarder, Flexport’s core power is automating worldwide commerce processes and sharing information in a central platform. Flexport Capital provides clients flexibility over conventional lenders as a result of it has deep perception of their enterprise fashions, buy order information and cargo information right down to the product degree. That information helps Flexport make choices on when to increase credit score and to supply extra versatile phrases. Flexport additionally provides customizable reimbursement phrases.

“Flexport Capital started from the assumption that an organization’s provide chain needs to be a core aggressive benefit and progress enabler, not a working capital obstacle,” mentioned Justin Sherlock, head of Flexport Capita, within the announcement. “With deeper visibility into total provide chain well being, we will help companies of all sizes — and their companions — to take away liquidity constraints within the midst of uncertainty. I’m thrilled to have KKR offering a credit score facility to assist us execute our imaginative and prescient to make international commerce straightforward for everybody.”

The KKR financing is likely one of the first main strikes Flexport has made since former prime Amazon govt Dave Clark joined the corporate as co-CEO on Sept. 1.

Click on right here for extra FreightWaves/American Shipper tales by Eric Kulisch.

RECOMMENDED READING:

Flexport faucets Amazon pipeline once more for operations chief

Air cargo peak season evaporates on decrease demand, greater capability

PA

PAFormer MSP Wendy Alexander claims she was asked to leave her senior post at Dundee University after asking “uncomfortable” questions about the institution’s finances, MSPs have been told.

Alexander was the university’s vice principal international for almost a decade but retired last year rather than accept what she said was the offer of a “package and trips.”

She said “cakeism, profligacy and hubris at the very top” led to “a failure to reign in expenditure” and that she “chose not to be bought off”.

She said former principal Prof Iain Gillespie, who was heavily criticised in a recent damning report into the university’s finances, “made clear” he wanted her to leave last October.

University of Dundee

University of DundeeAlexander’s comments were made in a statement submitted to Holyrood’s education committee.

Gillespie resigned with immediate effect in December after telling staff the previous month that job losses were “inevitable”.

He is expected to give evidence in person at the committee on Thursday.

The university currently faces a £35m deficit and has said it must cut 300 jobs through a voluntary redundancy scheme.

The independent report, published last week, said university bosses and its governing body failed multiple times to identify the worsening crisis and continued to overspend instead of taking action.

In her statement, former Labour MSP Alexander said: “I personally, was progressively frozen out of meetings, my objectives changed, data withheld and when I challenged the absence/adequacy of financial information in Sept (20)24, I was then asked to leave.

“I declined the offer of overseas trips at the university’s expense to be followed by a generous settlement payment.

“Quite simply, it seemed unethical and morally wrong.”

Alexander, who now sits as a baroness at the House of Lords, said she felt “punished for speaking out” and that the university “failed to fix the roof when the sun shone”.

She said international fee income had quadrupled over eight years to 2023, but the university was “barely breaking even”.

She said that international income plateaued in 2023/24 and fell the following year.

Alexander said there was a “misguided” shift away from a “laser-like focus on international student recruitment to a new globalisation strategy”.

She added that the university “deprioritised international student recruitment when it mattered most” and left the university “poorly equipped to deal with the downturn”.

The education committee is currently hearing evidence from the university’s former director of finance Peter Fotheringham, former chief operating officer Dr Jim McGeorge, and former chair of court Amanda Millar.

Alexander submitted her evidence rather than appearing in person due to a prior family event abroad.

It was announced on Tuesday that the university will receive an extra £40m from the Scottish government as the institution continues to tackle its financial crisis.

Education Secretary Jenny Gilruth said the decision would place specific conditions on the funding which will be paid over two academic years.

The university received £22m from the Scottish Funding Council in February as part of funding to support universities facing financial challenges.

Call to triple adaptation finance

At COP26 four years ago, governments agreed to “urge” developed countries to double finance for adapting to climate change up to around $40 billion a year by 2025.

That goal ends this year, although we will not know until 2027 if it has been met. But at a press conference in Bonn this afternoon, the Least Developed Countries group chair Evan Njewa called for a successor goal – tripling adaptation finance by 2030 on 2022 levels. “Adaptation is a lifeline,” he explained.

Other developing countries are likely to back this. Grupo Sur and the Like-Minded Developing countries have made the same call in different negotiating rooms and Njewa said he was sure that the small islands group AOSIS would back it too.

“We’re never going to say no to adaptation finance,” AOSIS finance negotiator Thibyan Ibrahim told Climate Home in Bonn. But he noted that even tripling “does little to close the adaptation finance gap”. The UN estimates that developing countries need $160-340 billion a year by 2030, whereas tripling on 2022 levels would bring in just under $100 billion.

Last year in Baku, developed governments would not agree to having a sub-goal on adaptation in the wider $300-billion-by-2035 finance goal and it’s not currently clear which negotiating track a new adaptation goal could be included in.

The doubling-by-2025 goal was in the COP26 cover decision – a stand-alone declaration all governments agree to – but the COP30 Presidency has said it does not want a cover decision.

It would fit in the Baku to Belem roadmap to $1.3 trillion or the Global Goal on Adaptation. But the roadmap is not an official negotiated UN agreement – so may not be followed up on – and developed-country governments have been resisting financial indicators in the Global Goal on Adaptation.

Meanwhile outside the world of UN climate talks, a recent CARE report showed that adaptation finance is likely to fall by 10% in 2026. France, Germany, the Netherlands and particularly the UK are set to make big cuts between 2025 and 2026.

The US is giving nothing in either 2025 or 2026. Commenting on US climate finance cuts generally, Njewa said he expects “someone somewhere to rise up and fill in the gap that that party has left”.

From Bonn to Nairobi?

Denouncing the visa problems faced by some developing country delegates heading to Bonn, more than 200 climate campaign groups made a joint call yesterday for governments to consider whether Germany should remain the default host for the mid-year climate talks.

Chanting “no borders, no nations, no visa applications”, a dozen campaigners gathered outside the conference centre on Tuesday morning, holding up a banner calling to move the annual talks to “visa-friendly countries”.

With many of those affected by the perennial issue unable to protest themselves, the demonstrators played a voice note from Roaa Alobeid, a young Sudanese climate activist who spoke movingly at COP28 about the war in her country.

She said she had gone to great lengths to get a visa for the Schengen area, which includes Germany, making an appointment, submitting 15 documents – including five letters of support and a bank statement – but was still rejected.

“I’m not there. I will never be there”, she said. “Why? I’m not worth it?” “We shouldn’t be left behind when we are the ones impacted.”

Cameroonian activist Zoneziwoh Mbondgulo-Wondieh did make it, but told the protest her one-year-old daughter had been refused a visa for being too young. She asked why Germany would implicitly tell a nursing mother they must stay at home and not work abroad.

When Climate Home questioned the German foreign office on this issue last year, a spokesperson said it was important to the government that all delegates could attend but there are legal requirements for getting a visa for the EU’s Schengen zone of free movement.

Rachitaa Gupta, head of the Global Campaign to Demand Climate Justice, said it would be better to hold the annual mid-year talks somewhere like Nairobi or Bangkok – where UN facilities already exist and visas are easier to obtain. Holding the meetings in the Global South would also be cheaper, Gupta added.

Climate finance on the rise – mostly for the rich

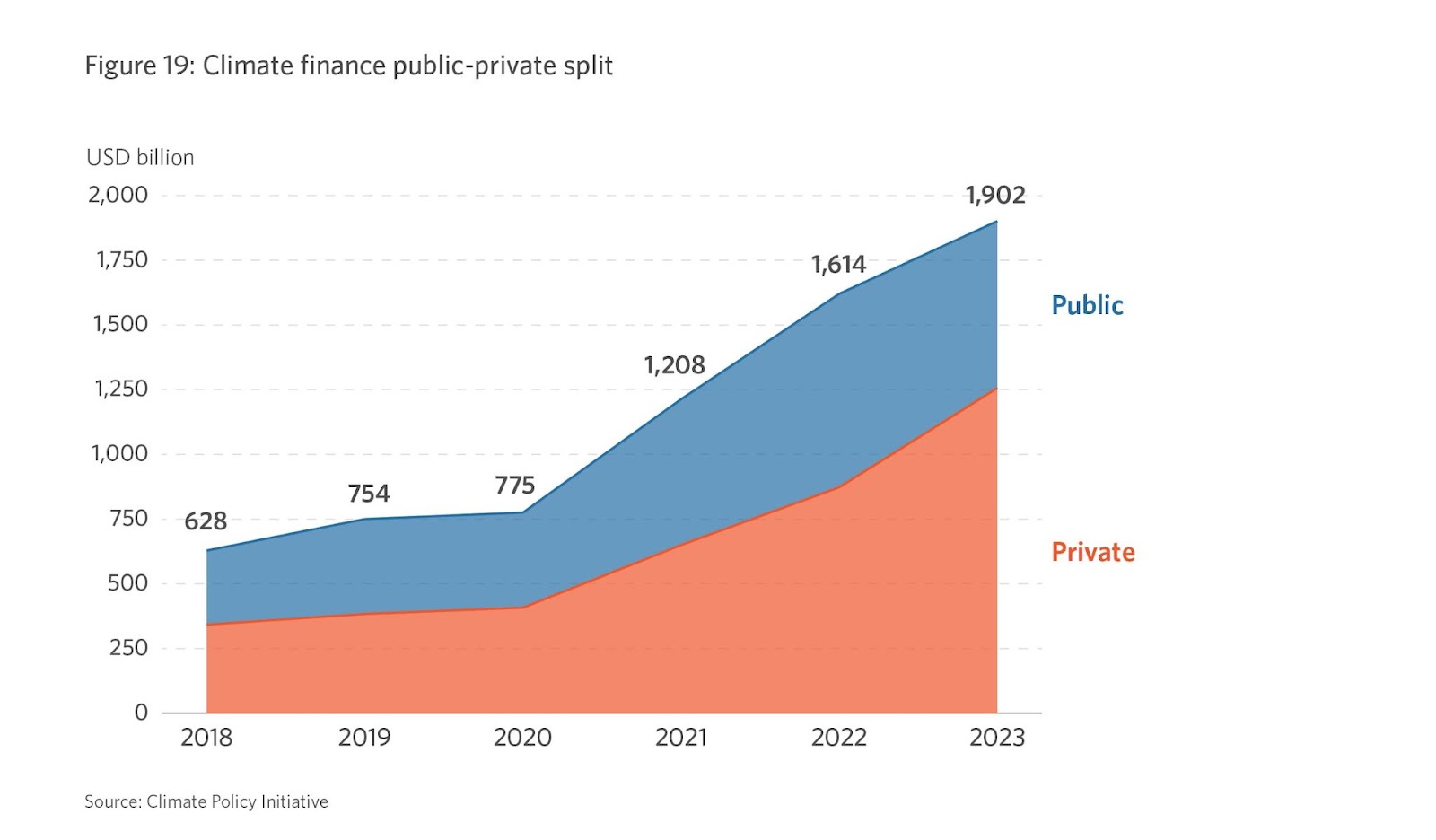

New figures out today paint a fairly positive picture of global climate finance, showing it climbed to a record $1.9 trillion in 2023, more than tripling over six years.

Climate Policy Initiative (CPI), which compiles the data, said that at the current rate of growth, the world could deliver $6 trillion in annual climate investment – the most conservative estimate of needs – by 2028.

Private-sector funding rose above $1 trillion for the first time in 2023, driven by household spending on electric vehicles, solar and energy-efficient housing – with clean energy in advanced economies and China receiving the bulk of the money.

While this suggests the long-touted need to “shift the trillions” towards green investment is underway, the headline numbers mask the fact that many of the poorest countries are still failing to receive anything like the amounts they need.

The CPI report shows that overall public climate finance fell by about 8% from 2022 to 2023, as government budgets were tight after the COVID-19 pandemic. It also warned that recently announced cuts to official development assistance, in countries such as the US and the UK, raise concern that money from this source could decline further.

International climate finance for emerging markets and developing countries reached $196 billion in 2023, with 78% of that from public sources. Yet while both climate-related development finance and private investment rose, CPI said the least-developed countries still face barriers to accessing affordable capital, and need more financial innovation and support.

In a separate report released on Monday, however, Oil Change International and 17 other NGOs warned that a widely used approach of using government money to lower investment risk and bring in more commercial cash – known as “blended finance” – is falling short of expectations.

The report found that every public dollar of concessional lending is bringing in 4-7 times less private investment than anticipated, leaving the Global South with massive shortfalls of cash for its energy transition. Most money, it said, is going to Global North countries and China, with the remaining 69% of the world’s population receiving just 15% of finance in 2023-2024.

“A just energy transition is dramatically more affordable than continued fossil fuel dependence. But unfortunately affordable doesn’t mean ‘attractive to banks and hedge funds’,” said Bronwen Tucker, global public finance lead at Oil Change. “It is clear from the data that private investors are not fit to lead the way to the fossil free future we need, and that governments must step in.”

Mineral justice for Africa

Efforts to revive the Lobito Corridor trade route in central Africa must prioritise local economic development over raw material exports, researchers at the International Institute for Environment and Development (IIED) said, as campaigners in Bonn call for justice for resource-rich countries and an end to the extractive injustices of the fossil fuel era.

The US and the European Union are providing financial support to Angola, the Democratic Republic of Congo and Zambia to upgrade their infrastructure to aid transport of critical energy transition minerals like cobalt and copper through a rail system which terminates at the port of Lobito on Angola’s Atlantic coast.

In a policy brief issued this week, highlighting the Corridor’s opportunities and challenges for a just transition, the researchers questioned how the project’s development will benefit the wider economies of the countries involved, while protecting social benefits and human rights including being fair to the people whose land it might encroach upon and the artisanal miners who dig up many of the raw materials.

They said the involvement of the EU and the US has raised concerns in participating countries such as Zambia, where a parliamentary committee has said the Lobito Corridor project appears to focus on “mopping up critical raw materials” to respond to the energy security concerns of wealthy nations without adding value to the countries.

Lorenzo Cotula, IIED principal researcher, said if the EU and other prospective funders are interested in a genuine, long-term partnership with Angola, Congo and Zambia, they should support their efforts to promote economic development and improve the lives of their citizens.

“This project shouldn’t just be a means to export more raw materials more quickly to wealthier countries, or another chess piece in the great power game,” Cotula said.

“Millions of people in mineral-rich, lower-income countries are being sidelined in a global rush for materials to power electric cars, computers and even military technologies in richer nations,” he added.

Sharing similar concern, campaigners from Power Shift Africa and the Natural Resource Governance Institute (NRGI) convened a press conference at the ongoing talks in Bonn calling for the need for just minerals in the just transition, because one cannot exist without the other.

Anabella Rosemberg, senior advisor on just transition at Climate Action Network International (CAN-I), said the transition that is happening is not one that is needed for a climate-compatible world because the needs of resource-rich countries are being ignored.

Rosemberg said there is need for international cooperation to overturn the current competition over resources, adding that “we know that investment and trade deals are being arranged to secure the supply of these minerals, and in the end, we are reproducing all the mistakes that have been done in the past with the fossil-based economy”.

Samira Ally, project officer at Power Shift Africa, said Africa’s mineral wealth can accelerate a global shift to net zero when governed by justice and stability with necessary guardrails in place.

To do this, she asked governments to integrate language from the G20 and the UN panel on critical minerals into the climate talks and national climate plans so that they “reference sustainable supply chains and the right to development and industrialisation in the Global South”.

The Reserve Bank of Australia (RBA) could be pushed to take a “more aggressive” rate-cutting approach following the conflict in the Middle East and the potential oil price shock. Some analysts now expect the central bank could cut interest rates a further three times this year.

KPMG has estimated the conflict in the Middle East could shave between 0.15 and 0.20 per cent of the GDP from the Australian economy this year, should the world oil market react in a similar way to how it responded to the first Iraq War. It said an “oil shock” combined with the continuing threat of a global tariff fallout could “force” the RBA’s hand.

“The longer an oil price shock is sustained, the worse its impact is in terms of inflation outcomes, inflation expectations and short-term growth,” KPMG said.

RELATED

“This is because oil price shocks can be particularly damaging to an economy like Australia’s as the road transport sector — one of the heaviest users of oil in our economy — touches every single other sector (including itself) across the country.”

Global oil prices slid 7.2 per cent on Monday following Iran’s retaliatory missile strike on a US airbase. The Brent crude price fell to around $US70 a barrel. This has eased fears of major supply disruptions, but markets remain cautious as tensions continue.

KPMG said it had revised down its RBA cash rate forecasts and now expects a further three rate cuts this year, one more than its original expectation at the start of 2025, bringing the cash rate down to 3.1 per cent by the end of the year.

It expects the RBA to “look through” any short-term inflationary impact of any oil shock and noted this would be combined with core inflation now looking well entrenched in the target band and overall weakness in the Australian economy.

If the RBA cuts interest rates three times, homeowners could see their repayments drop by $265 a month. That’s based on someone with an average $600,000 loan with 25 years remaining.

Markets have an 86 per cent expectation of an interest rate change at the next RBA meeting in July and are almost fully priced in for three more reductions by the end of the year.

NAB is the only Big Four bank predicting an interest rate cut next month, with ANZ, Commonwealth Bank and Westpac expecting a cut in August.

Westpac chief economist Luci Ellis said the RBA would be more focused on inflation than the oil price.

Los Chinelos de Morelos bring colorful Mexican dance to Indianapolis

Former Eagles RB Has Steelers Attention

Blackfin Purchases Sage Creek Apartments in Augusta, Georgia for $17.3M

July 4th 2025 Fireworks, Events Around Washington, D.C.

3 Players The Cleveland Cavaliers Should Target In The NBA Draft

-

Arizona7 days ago

Arizona7 days agoSuspect in Arizona Rangers' death killed by Missouri troopers

-

News1 week ago

News1 week agoAt Least 4 Dead and 4 Missing in West Virginia Flash Flooding

-

News1 week ago

News1 week agoOakland County sheriff urging vigilance after shootings of 2 Minnesota lawmakers

-

Culture1 week ago

Culture1 week agoBook Review: “The Möbius Book, by Catherine Lacey

-

Technology1 week ago

Technology1 week agoHow to build the best keyboard in the world

-

Movie Reviews1 week ago

Movie Reviews1 week ago10 Great Movies Panned Upon Release, From ‘The Thing’ to ‘Twin Peaks: Fire Walk With Me’

-

Business5 days ago

Business5 days agoDriverless disruption: Tech titans gird for robotaxi wars with new factory and territories

-

Politics1 week ago

Politics1 week agoSen Padilla insists he wasn’t disrupting Noem press conference: ‘I was simply asking a question’