Business

Is this the solution to California's soaring insurance prices due to wildfire risk?

In the past several years, homeowners across the state have been either burdened with extremely high insurance premiums or have struggled to find coverage at all. Wildfires have sent California’s homeowners insurance market into crisis and the situation is only getting worse. So far, 2024 has seen 219,247 acres burned, more than 20 times the amount this time last year. As wildfires become more frequent and destructive, insurers have worked to lower their risk exposure through rate hikes, nonrenewals, and even halting new policies in the state entirely.

New buyers and those whose policies have not been renewed have limited options since the biggest companies, State Farm, Farmers, Allstate, USAA, Travelers, Nationwide and Chubb, have limited or paused new policies in the last few years. Earlier this month State Farm’s cancellations of 30,000 homeowner policies mostly in high wildfire risk areas, took effect. In late June, State Farm requested a 31% rate increase, its largest increase in recent history, on the heels of a 22% increase earlier this year. Allstate also recently filed a request for a significant 34% rate increase.

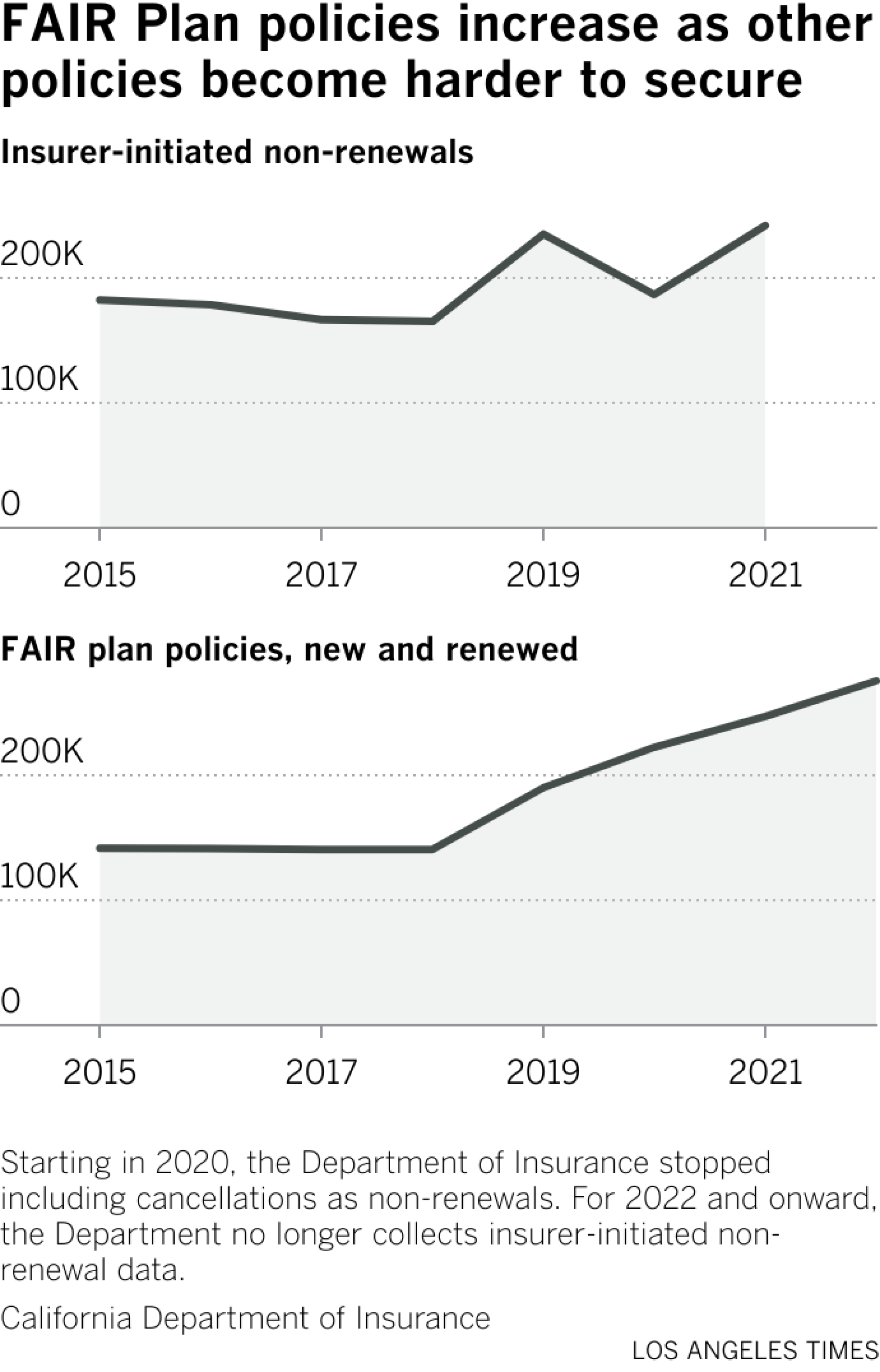

Homeowners are finding the expense and lack of options unsustainable. Sharon Goldman, longtime resident of the Pacific Palisades, has not had her policy canceled yet, but she has seen increases to her premium and worries she could be next. In her ZIP Code the wildfire risk is high, and State Farm decided to not renew 70% of their policies. Starting in 2019, rates of nonrenewals in high- and very high-risk areas grew to 14% compared with 3% and 2% for moderate- and low-risk areas.

Goldman, using her maiden name out of concern for retribution from State Farm, has paid her premiums each year since she bought her home 50 years ago. She has never filed a claim. But she has seen her rate increase 78% in the past two years. Her agent has told her that her fire coverage will be replaced with the state-run FAIR plan in 2025, an increasingly common insurer strategy that leaves homeowners paying more for less coverage.

Sharon Goldman poses for a portrait in Pacific Palisades in June. She is one of the many California homeowners struggling to maintain home insurance as costs increase and policies are dropped due to wildfire risk.

(Dania Maxwell/Los Angeles Times)

Goldman and her neighbors are left wondering what options they have left. She hears stories of people paying tens of thousands a year, an impossible amount for her to cover on her retirement budget. She has started looking into moving out of state and out of the home where she raised her children.

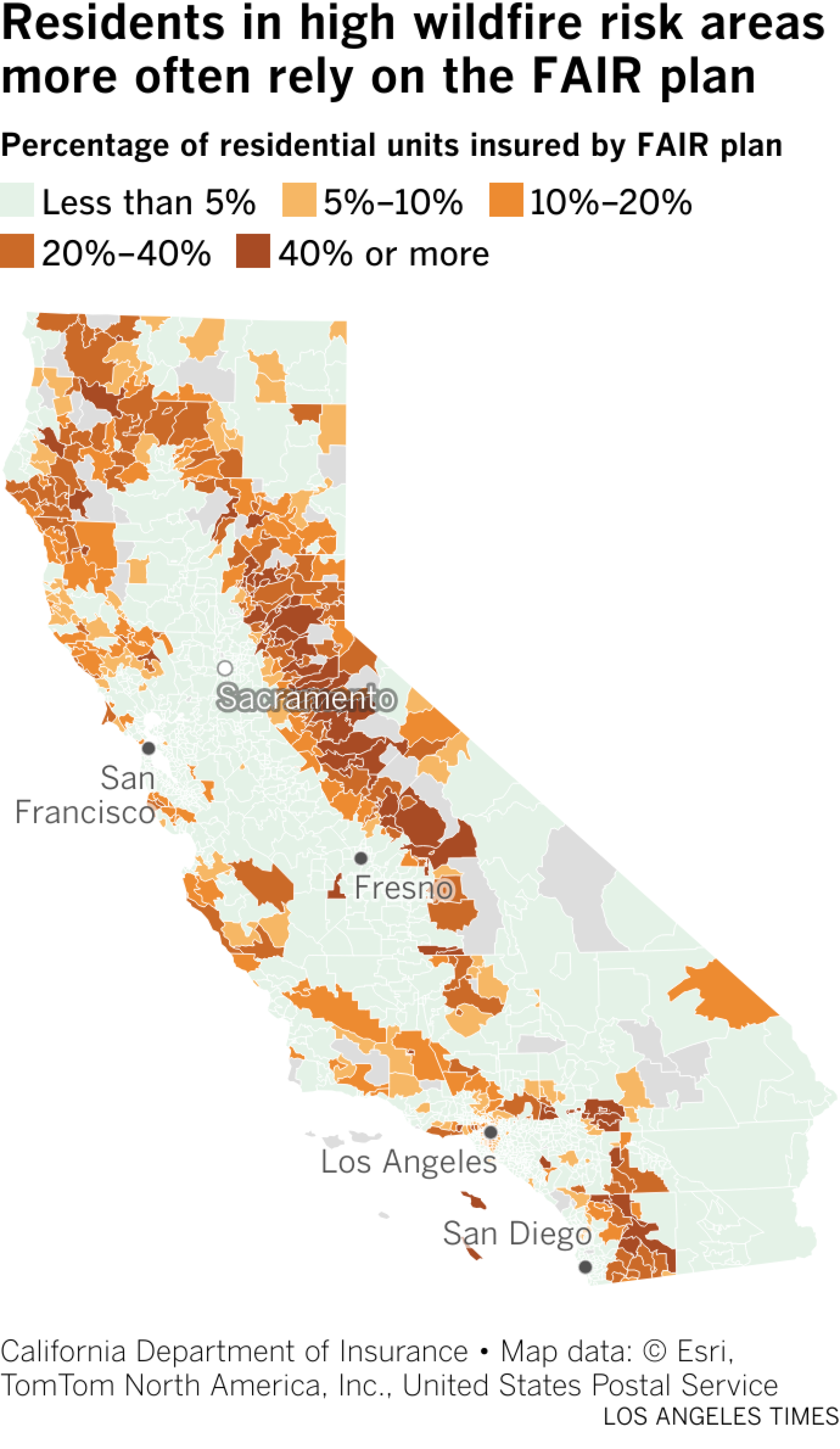

While the state does not require insurance, mortgage lenders do. So, going without is not an option for many. Those whose mortgage is paid off, like Goldman, may not be comfortable leaving their home, typically their most expensive asset, uninsured. High rates and loss of fire coverage have pushed desperate homeowners to riskier nonadmitted carriers or to the state-run FAIR plan, meant to be the plan of last resort. But the California Department of Insurance worries that it is quickly becoming overburdened.

Over the past year, Insurance Commissioner Ricardo Lara has been rolling out his plan to increase policy writing in vulnerable areas and get people off of the FAIR plan. One big component of his strategy is allowing insurers to use wildfire catastrophe models to set overall rates. Insurers say the tool would help them more accurately predict the correct rate for the amount of risk.

As a trade-off, Lara says companies that use these models will be required to increase service in distressed areas with a high wildfire risk and a high concentration of FAIR plan policies.

In public workshops held by the Department of Insurance, consumer advocates raised concerns about a lack of transparency with “black box” models that may be used to justify unnecessary rate hikes. Industry advocates are concerned the plan will take too long to implement when they desperately need changes now.

How likely is it a house will be damaged in a wildfire?

There are many versions of catastrophe models. Each modeling company has their own proprietary analysis but they all generally use the same data inputs to answer the same question.

The Harwarden fire burned over 500 acres, destroying three large homes and damaging seven others.

(Jen Osborne / For the Times)

Each modeled event starts with an ignition, the probability that a fire will start at that location, spread, the probability that the fire will travel based on the land cover in the area, and property characteristics. Using those data, the model simulates a large number of possible outcomes for a given location, estimates the likelihood that a structure will burn from wildfire, and calculates the loss for any buildings there.

The USDA Forest Service developed a national analysis of wildfire risk that is similar to what models created for insurance companies would look like. Based on vegetation and fire-behavior fuel models, topographic data, historical weather patterns and long-term simulations of large wildfire behavior, their wildfire likelihood map shows the probability of a fire in any given year.

A critical part of predicting the potential spread of the fire is the available fuel. The Forest Service’s land cover classifications are used in many wildfire models. They specify 40 different fuel types such as grass, shrub, timber, and nonburnable types. Each category is further subdivided based on depth of the cover and humidity or aridity of the climate.

For example, in an arid climate, coarse continuous grass at a depth of 3 feet would have a very high spread rate. A combination of low grass or shrubs and dead leaves or needles in the forest would have a low spread rate.

Property characteristics such as the type of roof or whether the siding is fire-resistive make a significant difference in whether a structure will ignite from wildfire embers. The Center for Insurance Policy and Research found that structural modifications can reduce wildfire risk up to 40%, and structural and vegetation modifications combined can reduce wildfire risk up to 75%.

All of these factors are combined in the model with information about the rebuilding cost and level of coverage to generate an amount of risk unique to the individual property.

Could these models turn the industry around?

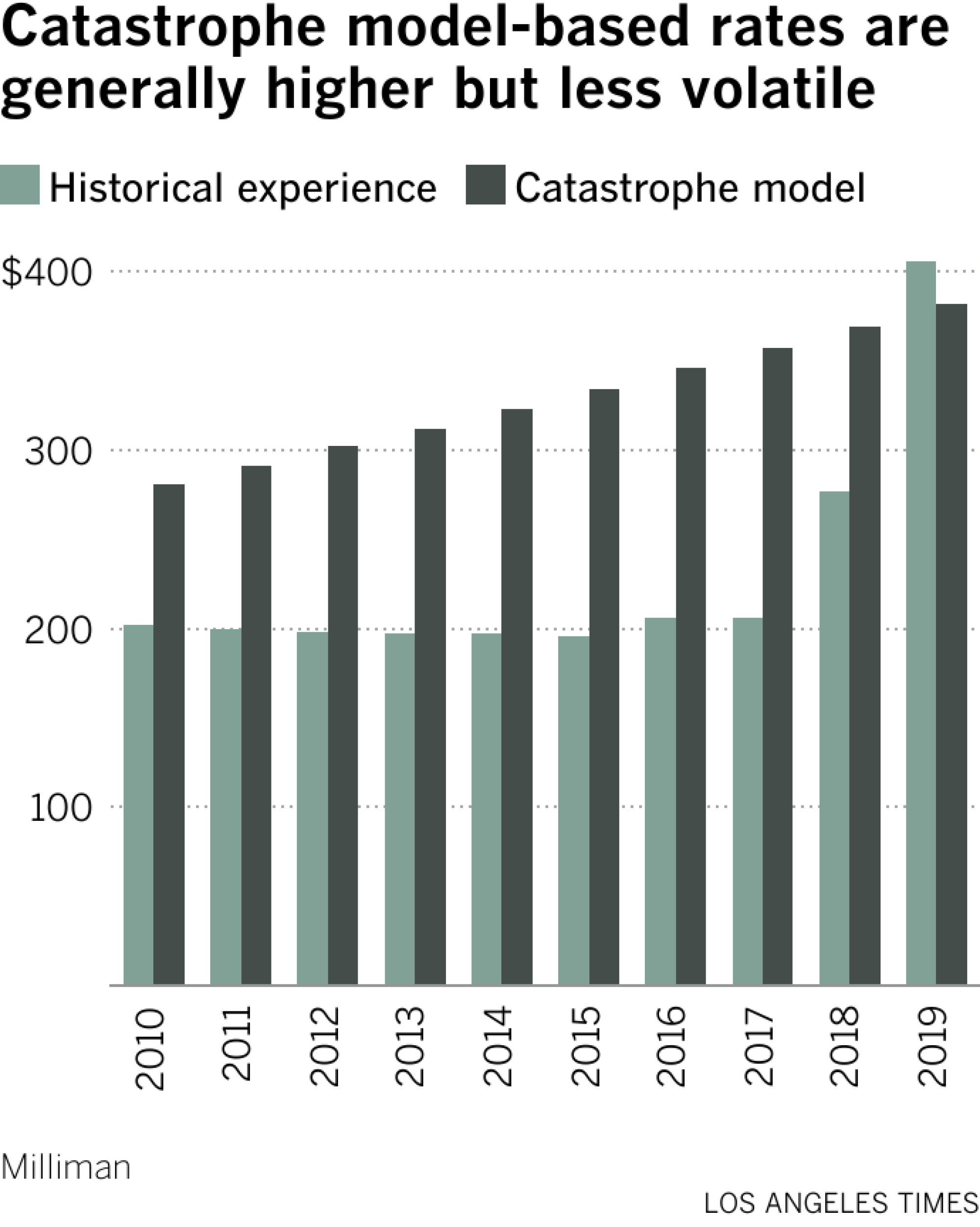

Currently, companies are required to calculate their projected losses, on which their overall rates are based, using a historical view of wildfire loss over the previous 20 years. As wildfires increase, however, this means that the average loss trails behind the current state of wildfire risk.

Nancy Watkins, an actuary and principal at the insurance consulting firm Milliman, said that she believes the inclusion of catastrophe models could save the industry. She analyzed the effect of a model on rates compared with using just historical experience. While the rates would generally be higher, the increases would be more even.

In April during a public meeting, Allstate said that if wildfire catastrophe models were allowed, they would once again start writing new policies in the state.

But wildfire catastrophe models are already used by insurance companies in California for some business decisions and have been for some time. They use models to determine where to write or renew policies, which is one of the reasons nonrenewals have disproportionately happened in high-risk areas.

In recent rate filings, Allstate, Farmers and State Farm cited a modeled wildfire risk score as the basis for not renewing policies. Allstate used CoreLogic’s Risk Meter score in 2019 to classify all policies that fell above certain risk thresholds as ineligible for renewal. A 2023 filing from Farmers documents eligibility guidelines for new and renewing policies that sets a risk level using Verisk’s FireLine and Zesty.ai’s Z-FIRE scores. State Farm’s recent 30,000 nonrenewals are based on CoreLogic’s Brushfire Risk Layer.

Amy Bach, executive director of United Policyholders, says that wildfire models worked their way into rates without enough state oversight. “We didn’t regulate the use of risk scores and now [they] are having a dramatic impact on the market and the genie is out of the bottle.”

Some companies use models to assess relative risk between properties and adjust individual rates accordingly. State Farm multiplies its base rate by a location rating factor, calculated using catastrophe models produced by CoreLogic and Verisk. Areas with high wildfire risk have seen dramatic increases in the location rating factor in the past few years.

This process is called segmentation and the Department of Insurance is aware that it is opaque. Department spokesperson Michael Soller says, “People do not know what their risk score is. They don’t know what goes into the risk score. It’s a black box. Yet, the risk score can be used to [charge you] double what somebody else pays.”

While these situations are significant for some, they generally only apply to select high-risk properties. The median effect of the location rating factor has remained fairly stable.

But under the commissioner’s new policy, model results could also be incorporated directly into the overall rate. Soller says that one important difference in this new regulation is that for a model to be valid, it will need to incorporate property and community level risk mitigation into rates, including state agency forest thinning and utility company efforts. As more investment goes into making communities safer, in theory the rates should decrease.

Only you can prevent forest fires?

Wildfire mitigation happens at the state and local level. Since 2020, in addition to baseline spending, California has allocated more than $2.6 billion towards its wildfire and forest resilience package. 872 communities in the state are registered participants in Firewise USA, a program administered by the National Fire Protection Association that sets standards for fire safety.

For an individual, retrofitting one’s home for wildfire resistance is not cheap. On average, homeowners spend $15,000 on a new roof.

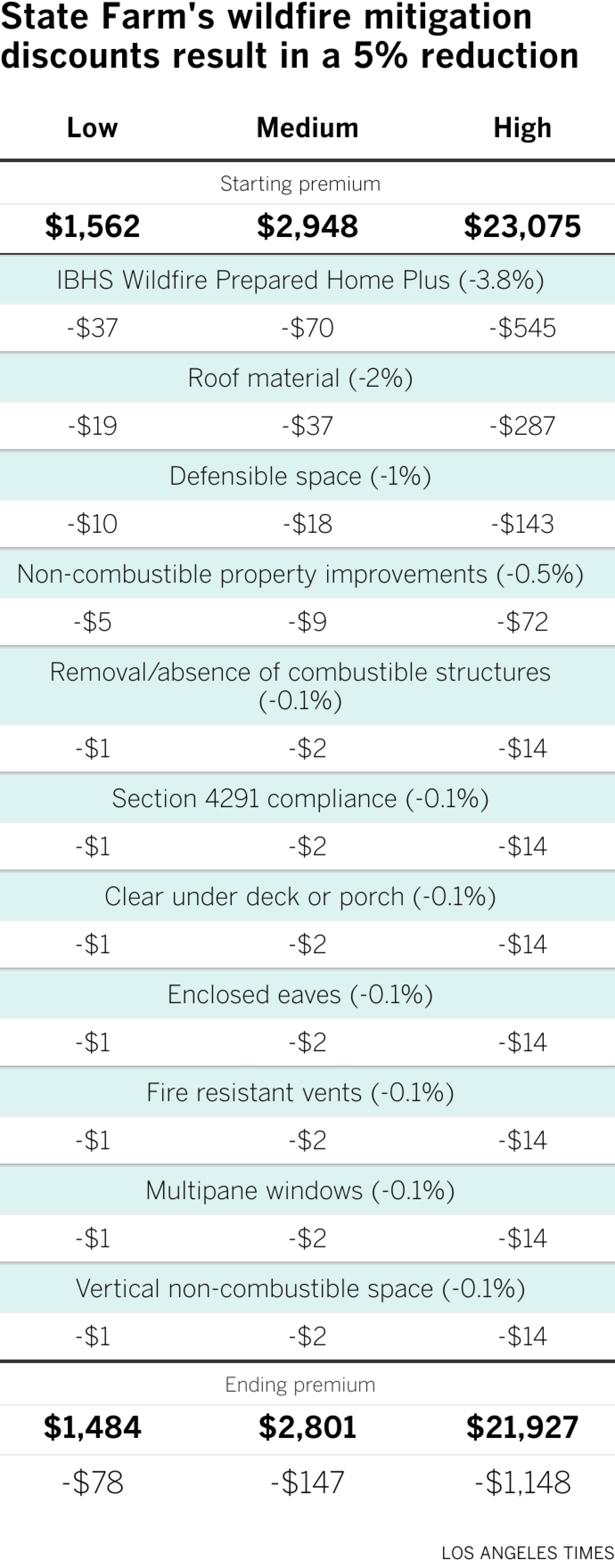

As of October 2022, companies such as State Farm that use wildfire models in segmentation are already supposed to give mitigation discounts. A February filing from State Farm breaks down how their discounts would work in a low-, medium- and high-risk area.

For the low-risk group, the dollar amount saved may not be worth the investment in mitigation. For the high-risk group, the slightly lower percentage reductions would still result in more substantial dollar amounts saved.

According to the State Farm documents, these discounts are given at a set rate for all properties across the state. Granular catastrophe models take into account the impact of mitigation on the property level, nearby community mitigation and any recent wildfire history that might indicate a temporarily reduced risk.

However, a complaint raised several times during the regulation workshops was that when homeowners do spend money, often thousands, on lowering risk, they do not see any changes in their insurance premiums. Some say their policies were still dropped.

Goldman has already completed the property-level mitigation work. She has a class A Spanish tile roof. She does the brush clearance every year. This past year it cost about $1,200. She even has an outdoor sprinkler system. But she did not learn about mitigation from her insurance company. Instead, it was on one of Bach’s monthly educational community calls where she got the idea to install fire-resistant vents.

Sharon Goldman walks through the exterior of her home where she has lived for about 50 years and raised four kids in Pacific Palisades. (Dania Maxwell/Los Angeles Times)

And yet, she has not received a mitigation credit from State Farm and has not received any information about how to receive one. When she asked her agent whether the work she had done on her home qualified for a discount he said no. The Department of Insurance says that they review consumer complaints for rate accuracy and conduct regular examinations of insurance companies. They noted that concerned consumers should contact them to review their specific situation.

Making models a reality

The catastrophe modeling regulation requires insurers to submit their modeling information to the Department of Insurance for review by an internal model advisor and any necessary consultants. Some proprietary information is allowed to remain confidential but proponents of the plan say that the regulators will have all the information they need to assess the models even if the general public does not.

Firefighters work to douse a home on fire in Harwarden Hills, a high-end living community in Riverside.

(Jen Osborne / For The Times)

The department says it is still considering public input from the most recent workshop and has no further plans for additional workshops. Once the regulation is finalized there will be a public hearing. Commissioner Lara plans to have this regulation and the rest of the Sustainable Insurance Plan in place by the end of the year.

In addition to forward-looking catastrophe models, Lara’s plan will introduce the ability for insurance companies to include reinsurance costs in rates and to increase coverage in the FAIR plan. Details for both of those changes are expected to be released this month.

, Biz Council Reined In")

President Trump on Friday directed federal agencies to stop using technology from San Francisco artificial intelligence company Anthropic, escalating a high-profile clash between the AI startup and the Pentagon over safety.

In a Friday post on the social media site Truth Social, Trump described the company as “radical left” and “woke.”

“We don’t need it, we don’t want it, and will not do business with them again!” Trump said.

The president’s harsh words mark a major escalation in the ongoing battle between some in the Trump administration and several technology companies over the use of artificial intelligence in defense tech.

Anthropic has been sparring with the Pentagon, which had threatened to end its $200-million contract with the company on Friday if it didn’t loosen restrictions on its AI model so it could be used for more military purposes. Anthropic had been asking for more guarantees that its tech wouldn’t be used for surveillance of Americans or autonomous weapons.

The tussle could hobble Anthropic’s business with the government. The Trump administration said the company was added to a sweeping national security blacklist, ordering federal agencies to immediately discontinue use of its products and barring any government contractors from maintaining ties with it.

Defense Secretary Pete Hegseth, who met with Anthropic’s Chief Executive Dario Amodei this week, criticized the tech company after Trump’s Truth Social post.

“Anthropic delivered a master class in arrogance and betrayal as well as a textbook case of how not to do business with the United States Government or the Pentagon,” he wrote Friday on social media site X.

Anthropic didn’t immediately respond to a request for comment.

Anthropic announced a two-year agreement with the Department of Defense in July to “prototype frontier AI capabilities that advance U.S. national security.”

The company has an AI chatbot called Claude, but it also built a custom AI system for U.S. national security customers.

On Thursday, Amodei signaled the company wouldn’t cave to the Department of Defense’s demands to loosen safety restrictions on its AI models.

The government has emphasized in negotiations that it wants to use Anthropic’s technology only for legal purposes, and the safeguards Anthropic wants are already covered by the law.

Still, Amodei was worried about Washington’s commitment.

“We have never raised objections to particular military operations nor attempted to limit use of our technology in an ad hoc manner,” he said in a blog post. “However, in a narrow set of cases, we believe AI can undermine, rather than defend, democratic values.”

Tech workers have backed Anthropic’s stance.

Unions and worker groups representing 700,000 employees at Amazon, Google and Microsoft said this week in a joint statement that they’re urging their employers to reject these demands as well if they have additional contracts with the Pentagon.

“Our employers are already complicit in providing their technologies to power mass atrocities and war crimes; capitulating to the Pentagon’s intimidation will only further implicate our labor in violence and repression,” the statement said.

Anthropic’s standoff with the U.S. government could benefit its competitors, such as Elon Musk’s xAI or OpenAI.

Sam Altman, chief executive of OpenAI, the company behind ChatGPT and one of Anthropic’s biggest competitors, told CNBC in an interview that he trusts Anthropic.

“I think they really do care about safety, and I’ve been happy that they’ve been supporting our war fighters,” he said. “I’m not sure where this is going to go.”

Anthropic has distinguished itself from its rivals by touting its concern about AI safety.

The company, valued at roughly $380 billion, is legally required to balance making money with advancing the company’s public benefit of “responsible development and maintenance of advanced AI for the long-term benefit of humanity.”

Developers, businesses, government agencies and other organizations use Anthropic’s tools. Its chatbot can generate code, write text and perform other tasks. Anthropic also offers an AI assistant for consumers and makes money from paid subscriptions as well as contracts. Unlike OpenAI, which is testing ads in ChatGPT, Anthropic has pledged not to show ads in its chatbot Claude.

The company has roughly 2,000 employees and has revenue equivalent to about $14 billion a year.

new video loaded: The Web of Companies Owned by Elon Musk

By Kirsten Grind, Melanie Bencosme, James Surdam and Sean Havey

February 27, 2026

Business

Commentary: How Trump helped foreign markets outperform U.S. stocks during his first year in office

Trump has crowed about the gains in the U.S. stock market during his term, but in 2025 investors saw more opportunity in the rest of the world.

If you’re a stock market investor you might be feeling pretty good about how your portfolio of U.S. equities fared in the first year of President Trump’s term.

All the major market indices seemed to be firing on all cylinders, with the Standard & Poor’s 500 index gaining 17.9% through the full year.

But if you’re the type of investor who looks for things to regret, pay no attention to the rest of the world’s stock markets. That’s because overseas markets did better than the U.S. market in 2025 — a lot better. The MSCI World ex-USA index — that is, all the stock markets except the U.S. — gained more than 32% last year, nearly double the percentage gains of U.S. markets.

That’s a major departure from recent trends. Since 2013, the MSCI US index had bested the non-U.S. index every year except 2017 and 2022, sometimes by a wide margin — in 2024, for instance, the U.S. index gained 24.6%, while non-U.S. markets gained only 4.7%.

The Trump trade is dead. Long live the anti-Trump trade.

— Katie Martin, Financial Times

Broken down into individual country markets (also by MSCI indices), in 2025 the U.S. ranked 21st out of 23 developed markets, with only New Zealand and Denmark doing worse. Leading the pack were Austria and Spain, with 86% gains, but superior records were turned in by Finland, Ireland and Hong Kong, with gains of 50% or more; and the Netherlands, Norway, Britain and Japan, with gains of 40% or more.

Investment analysts cite several factors to explain this trend. Judging by traditional metrics such as price/earnings multiples, the U.S. markets have been much more expensive than those in the rest of the world. Indeed, they’re historically expensive. The Standard & Poor’s 500 index traded in 2025 at about 23 times expected corporate earnings; the historical average is 18 times earnings.

Investment managers also have become nervous about the concentration of market gains within the U.S. technology sector, especially in companies associated with artificial intelligence R&D. Fears that AI is an investment bubble that could take down the S&P’s highest fliers have investors looking elsewhere for returns.

But one factor recurs in almost all the market analyses tracking relative performance by U.S. and non-U.S. markets: Donald Trump.

Investors started 2025 with optimism about Trump’s influence on trading opportunities, given his apparent commitment to deregulation and his braggadocio about America’s dominant position in the world and his determination to preserve, even increase it.

That hasn’t been the case for months.

”The Trump trade is dead. Long live the anti-Trump trade,” Katie Martin of the Financial Times wrote this week. “Wherever you look in financial markets, you see signs that global investors are going out of their way to avoid Donald Trump’s America.”

Two Trump policy initiatives are commonly cited by wary investment experts. One, of course, is Trump’s on-and-off tariffs, which have left investors with little ability to assess international trade flows. The Supreme Court’s invalidation of most Trump tariffs and the bellicosity of his response, which included the immediate imposition of new 10% tariffs across the board and the threat to increase them to 15%, have done nothing to settle investors’ nerves.

Then there’s Trump’s driving down the value of the dollar through his agitation for lower interest rates, among other policies. For overseas investors, a weaker dollar makes U.S. assets more expensive relative to the outside world.

It would be one thing if trade flows and the dollar’s value reflected economic conditions that investors could themselves parse in creating a picture of investment opportunities. That’s not the case just now. “The current uncertainty is entirely man-made (largely by one orange-hued man in particular) but could well continue at least until the US mid-term elections in November,” Sam Burns of Mill Street Research wrote on Dec. 29.

Trump hasn’t been shy about trumpeting U.S. stock market gains as emblems of his policy wisdom. “The stock market has set 53 all-time record highs since the election,” he said in his State of the Union address Tuesday. “Think of that, one year, boosting pensions, 401(k)s and retirement accounts for the millions and the millions of Americans.”

Trump asserted: “Since I took office, the typical 401(k) balance is up by at least $30,000. That’s a lot of money. … Because the stock market has done so well, setting all those records, your 401(k)s are way up.”

Trump’s figure doesn’t conform to findings by retirement professionals such as the 401(k) overseers at Bank of America. They reported that the average account balance grew by only about $13,000 in 2025. I asked the White House for the source of Trump’s claim, but haven’t heard back.

Interpreting stock market returns as snapshots of the economy is a mug’s game. Despite that, at her recent appearance before a House committee, Atty. Gen. Pam Bondi tried to deflect questions about her handling of the Jeffrey Epstein records by crowing about it.

“The Dow is over 50,000 right now, she declared. “Americans’ 401(k)s and retirement savings are booming. That’s what we should be talking about.”

I predicted that the administration would use the Dow industrial average’s break above 50,000 to assert that “the overall economy is firing on all cylinders, thanks to his policies.” The Dow reached that mark on Feb. 6. But Feb. 11, the day of Bondi’s testimony, was the last day the index closed above 50,000. On Thursday, it closed at 49,499.50, or about 1.4% below its Feb. 10 peak close of 50,188.14.

To use a metric suggested by economist Justin Wolfers of the University of Michigan, if you invested $48,488 in the Dow on the day Trump took office last year, when the Dow closed at 48,448 points, you would have had $50,000 on Feb. 6. That’s a gain of about 3.2%. But if you had invested the same amount in the global stock market not including the U.S. (based on the MSCI World ex-USA index), on that same day you would have had nearly $60,000. That’s a gain of nearly 24%.

Broader market indices tell essentially the same story. From Jan. 17, 2025, the last day before Trump’s inauguration, through Thursday’s close, the MSCI US stock index gained a cumulative 16.3%. But the world index minus the U.S. gained nearly 42%.

The gulf between U.S. and non-U.S. performance has continued into the current year. The S&P 500 has gained about 0.74% this year through Wednesday, while the MSCI World ex-USA index has gained about 8.9%. That’s “the best start for a calendar year for global stocks relative to the S&P 500 going back to at least 1996,” Morningstar reports.

It wouldn’t be unusual for the discrepancy between the U.S. and global markets to shrink or even reverse itself over the course of this year.

That’s what happened in 2017, when overseas markets as tracked by MSCI beat the U.S. by more than three percentage points, and 2022, when global markets lost money but U.S. markets underperformed the rest of the world by more than five percentage points.

Economic conditions change, and often the stock markets march to their own drummers. The one thing less likely to change is that Trump is set to remain president until Jan. 20, 2029. Make your investment bets accordingly.

How to Watch Virginia vs. Duke Basketball Game Online Without Cable

Man charged with shooting co-worker in Washington Heights

Wisconsin Lottery Mega Millions, Pick 3 results for Feb. 27, 2026

As Mountaineers try to move forward from recent struggles, freshman sensation Dybantsa awaits – WV MetroNews

, Biz Council Reined In")

University Of Wyoming Budget Spared (For Now), Biz Council Reined In

Florida High School Football Rankings: Top 25 teams – Oct. 21

Cleary's 21 help Le Moyne down Central Connecticut State 69-64 in OT

How old is Bo Nix? What to know about Oregon quarterback ahead of 2024 NFL Draft

99th annual Pony Swim held in Virginia

Indiana Members Credit Union announced as new anchor tenant at Bottleworks District

ICE blasts Washington mayor over directive restricting immigration enforcement

Did the EU bypass Hungary’s veto on Ukraine’s €90 billion loan?

How the federal government is painting immigrants as criminals on social media

Where Iran’s ballistic missiles can reach — and how close they are to the US

Has India’s influence in Afghanistan grown under the Taliban?

-

World2 days ago

World2 days agoExclusive: DeepSeek withholds latest AI model from US chipmakers including Nvidia, sources say

-

Massachusetts2 days ago

Massachusetts2 days agoMother and daughter injured in Taunton house explosion

-

Montana1 week ago

Montana1 week ago2026 MHSA Montana Wrestling State Championship Brackets And Results – FloWrestling

-

Louisiana5 days ago

Louisiana5 days agoWildfire near Gum Swamp Road in Livingston Parish now under control; more than 200 acres burned

-

Denver, CO2 days ago

Denver, CO2 days ago10 acres charred, 5 injured in Thornton grass fire, evacuation orders lifted

-

Technology7 days ago

Technology7 days agoYouTube TV billing scam emails are hitting inboxes

-

Technology7 days ago

Technology7 days agoStellantis is in a crisis of its own making

-

Politics7 days ago

Politics7 days agoOpenAI didn’t contact police despite employees flagging mass shooter’s concerning chatbot interactions: REPORT