Listen to this podcast on Spotify, Apple Podcasts, Podbean, Podtail, ListenNotes, TuneIn

The volatility of the geopolitical and macroeconomic environment in recent years has caused some problems in the trade, treasury, and payments industries.

However, industry actors have adapted and are working together to build resilience and make international trade even stronger.

Advertisement

To hear about developments in the factoring and supply chain finance world, Trade Finance Global (TFG) spoke with Çağatay Baydar, Chairman at FCI and Irina Tyan, Principal Banker, TFP at the European Bank for Reconstruction and Development (EBRD).

Challenges and growth in the factoring industry

The factoring industry has demonstrated impressive growth since the turn of the century despite facing significant challenges, particularly in emerging markets.

Baydar said, “The growth rate in 2023 was 3.3% globally in the volume of the world factoring and in 2022 it was 18%. Over the last 20 years, the average growth rate has been 8% which shows that factoring is becoming a mainstream financial product globally, which is very good indeed.”

The sector, which revolves around the purchase of receivables from businesses to provide them with immediate liquidity, has become an essential component of global trade finance, but it also faces challenges. One of the primary challenges is the bureaucratic and infrastructural limitations inherent in the current system.

Factoring, being an invoice-based product, requires a significant amount of paperwork and documentation, which can be cumbersome and traditionally relies on a paper-based system that only adds to the administrative burden for businesses.

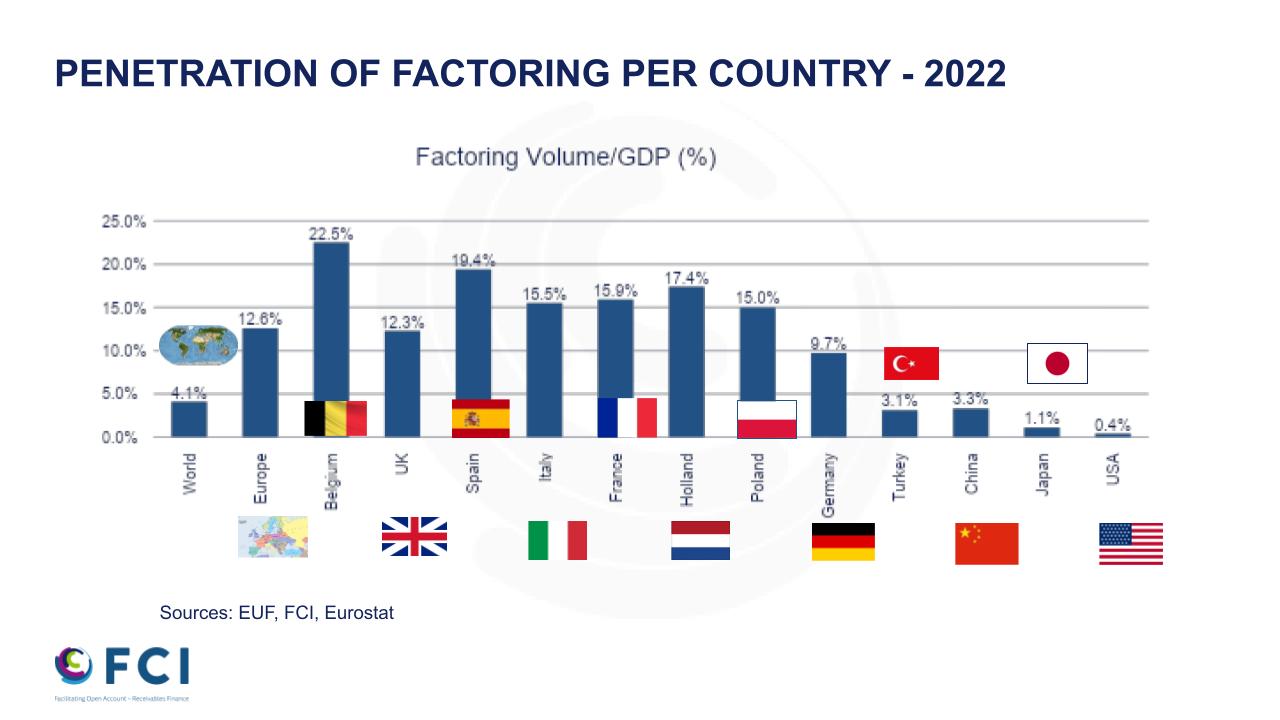

In developed regions like Europe, factoring’s penetration rate – a measure of the amount of trade volume that uses factoring – is around 15%, reflecting a more mature understanding and use of this financial product. By contrast, in emerging markets, the penetration rate is significantly lower, with countries like Turkey and Georgia showing rates as low as 3%.

Advertisement

This discrepancy highlights the knowledge gap and infrastructural deficiencies in these regions. Businesses in these markets often lack the necessary awareness and understanding of factoring, which limits their ability to leverage this financial tool to its full potential.

However, factoring usage in some emerging markets is growing.

Tyan said, “We see the progress in the countries where we started five to seven years ago, like Georgia. We recently had a workshop in Jordan, where we also see a more adapted market, more ready to look into this type of product.”

Further collaboration and efforts to promote regulatory reforms and technological advancements may be what is needed to drive factoring growth in these underutilised regions.

Regulatory reforms and technological integration

Regulatory reforms are crucial for the sustained growth and development of the factoring industry, and legal clarity is particularly important in emerging markets, where the absence of a well-defined regulatory environment can pose significant barriers to factoring’s growth.

One of the key areas that require attention is the standardisation of data exchange formats.

Advertisement

Creating common data standards for supply chain transactions can facilitate smoother integration between different platforms and financial institutions, improving efficiency, reducing administrative burdens, and enhancing the overall effectiveness of the factoring process.

Another important aspect of regulatory reform is cybersecurity.

Tyan said, “As this product heavily relies on platforms, clear regulation on data security and cybersecurity is crucial to build trust among the participants.”

Ensuring the integrity and security of transactions protects sensitive financial information from potential cyber threats and is vital for the long-term sustainability and credibility of the industry.

Digitalising to draw clients and talent to factor

The factoring industry has been significantly transformed by the integration of digital technologies that have made the process faster, more efficient, and more accessible, especially for small and medium-sized enterprises (SMEs).

Traditionally, the paperwork involved in factoring, particularly for international transactions, slowed down the process and added to its complexity but digital platforms are allowing for quicker access to funds and improving the overall client experience.

Advertisement

Baydar said, “Today, with digitalisation and the platforms, we are making our business much faster, quicker, and more effective. This really helps SMEs to touch the money very soon, very quickly. This makes our clients happier than before because they can experience a very fast, very effective, seamless transaction.”

This shift not only speeds up transactions but also minimises the risk of errors and fraud associated with manual paperwork and can help attract more young professionals to the industry.

Baydar said, “Young people prefer to work with new technology and high-level startup businesses rather than traditional models.”

The new generation of workers is drawn to innovation and technologically advanced sectors. By embracing digital advancements, the factoring industry can position itself as a forward-thinking and dynamic field, appealing to young talent looking for exciting career opportunities. This influx of new talent is essential for sustaining the industry’s growth and development in the long term.

Organisations that fail to embrace digitalisation risk being left behind in a rapidly evolving market, meaning that investing in digital solutions is not just an option but a necessity for the future of the factoring industry.

Consumer confidence has plunged among traditionally optimistic younger adults amid fears for their personal finances and the wider economy, figures show.

GfK’s long-running Consumer Confidence Index remained unchanged at an overall score of minus 23 in June.

However, the analyst said this was was “misleading as, beneath the surface, there are new signs that confidence is weakening”.

Source: GfK

Neil Bellamy, consumer insights director at GfK, said: “The biggest fall this month is among those aged 16 to 29, traditionally one of the most optimistic groups.

“Here confidence has dropped 11 points over the past month to minus two, the lowest level seen for two years, driven by large falls in views on both their own personal finances and the wider economy.

Advertisement

“More broadly, there are now no demographic groups with a positive confidence score, including higher-income households earning £50,000 or more, who have slipped back into negative territory as of June.

“Confidence remains subdued and vulnerable to further economic or political uncertainty.”

Sourve: GfK

Overall, confidence in personal finances over the coming year remained flat at minus two, four points lower than this time last year.

The measures of both personal finances and the economy over the previous 12 months were both slightly down, by two points and three points respectively, “reflecting the sense that things have been extremely tough over the last year for so many”, GfK said.

The only measure to increase was expectations for the wider economy over the next 12 months, up two points to minus 36 but still eight points below this time last year.

The major purchase index, an indicator of confidence in buying big ticket items, remained at minus 20, four points lower than June last year.

“Ships of the World, start your engines. Let the oil flow!” said Donald Trump on social media after he announced the signing of an interim peace deal with Iran on Sunday. Under the agreement – which Iran acknowledged included a 60-day negotiating period for a final deal – the president said that following retrieval of mines, there would be a “toll free opening” of the Strait of Hormuz.

But many of the finer details remain “unclear”, said The Guardian. There are questions over the “exact timing of the reopening of the maritime route, who will oversee safe passage and whether any conditions will be applied”.

Financial markets have welcomed the announcement, but further volatility could yet hit people’s pockets.

The Week

Escape your echo chamber. Get the facts behind the news, plus analysis from multiple perspectives.

SUBSCRIBE & SAVE

Advertisement

Sign up for The Week’s Free Newsletters

From our morning news briefing to a weekly Good News Newsletter, get the best of The Week delivered directly to your inbox.

From our morning news briefing to a weekly Good News Newsletter, get the best of The Week delivered directly to your inbox.

Latest Videos From

Have oil prices changed?

The price of oil fell to about $83 (£62) per barrel following Sunday’s announcement, its “lowest since the early days of the war”. Then on Tuesday it dipped below $80. In February, before the first missiles struck Iran, each barrel cost around $73. The price peaked at around $120 at the height of the conflict.

Prices are expected to fall in the wake of a prolonged ceasefire, and there are “real grounds for optimism”, said Politico. Damage to oil-specific infrastructure has been “limited”, meaning it could take “as little as six weeks to resume outflows”.

“So that’s the energy crisis sorted, right?” Not so fast.” A combination of damage to wider infrastructure and the continued closure of the Strait of Hormuz has meant roughly 12 million fewer barrels of oil have been produced each day. And they “won’t magically reappear on the market even if the pact holds”.

Advertisement

Will this continue?

The “first big test” of the deal will be whether shipping companies will have enough “confidence” to return the use of the strait to pre-war levels, said The New York Times. If successful, this will free the 250 tankers and 330 cargo ships trapped in the Gulf, according to the BBC, and transport oil around the world. Oil and gas producers in the Gulf nations would then need to re-establish “wells, refineries and other infrastructure”.

Join 350,000+ subscribers and keep yourself informed with a selection of

The Week’s most interesting, enlightening and entertaining stories – plus daily puzzles.

Even if all of that were to materialise, European and Asian countries who have historically depended on oil from the region “will face a long wait”. Processing oil takes considerable time. “It is unlikely that the prices of gasoline, diesel and other fuels will return to pre-war levels anytime soon.”

What about inflation?

Despite air fares “surging” and fuel costs “tipping higher”, UK inflation remained at 2.8% in May, said The Independent. This was a “surprise” to economists, who had widely predicted a rise to 3% and “perhaps even beyond” due in part to the war in Iran.

Remaining at this level could imply that the “cost-of-living squeeze will not play out as badly as had been anticipated” earlier this year, even if the “Iran war sent energy costs spiralling”. However, prices are set to rise again later in 2026, leaving savers to make sure their investments are earning an interest rate “well above the rate of inflation”.

Advertisement

What does this mean for consumers?

Food prices in the UK look to be rising more slowly. Should the Strait of Hormuz open freely, fertiliser, which has “soared in costs” and put pressure on farmers, could fall substantially, said the BBC. Jet fuel has already seen a “small fall in price”, with Northwest Europe jet fuel trading at $1,033 (£780) per tonne, compared with $831 pre-conflict and around $1,840 at its peak.

How will businesses be affected?

Beneath the “encouraging headlines” about inflation control, there is a “hidden crisis for businesses”, said The Telegraph. The Iran war triggered one of the largest energy shocks in history, meaning businesses were “swallowing soaring costs to spare shoppers”.

“Input rises” for producers climbed by “8.7% year on year in May”, larger than the 7.9% in April and the highest in more than three years. On the bright side, this means the economy may avoid a dreaded “wage-price spiral”, but conversely lower margins could lead to increased pressure on the employment market.

Hong Kong graduates believe the city’s finance industry is its most attractive and stable sector, making them more optimistic about career opportunities than their global peers, according to a study by the CFA Institute, which trains investment managers.

The US-based institute’s “2026 Graduate Outlook Survey”, released on Wednesday, found that 71 per cent of Hong Kong graduates rated their career prospects between eight and 10 out of 10. The global average for that level of optimism was 59 per cent.

The graduates’ view of careers in finance reflected “both the sector’s resilience and Hong Kong’s continued strength as an international financial centre, which ranks third worldwide and first in Asia-Pacific”, the institute said in a statement.

The findings also indicated that young people were confident about Hong Kong’s role as an international financial centre, resilient amid global uncertainties, and strategically focused on improving skills, it said.

That confidence was “deeply grounded”, it said, with nearly 90 per cent believing they had the skills to succeed and clearly understood what employers were looking for, notwithstanding the wider adoption of artificial intelligence in the city.

“Rather than viewing AI as a threat, 38 per cent of Hong Kong graduates believe it has no negative impact on their job hunting, and 37 per cent believe it makes securing a job easier,” the institute said. “Three quarters are already actively using AI tools in their job applications, demonstrating a proactive, tool-first mindset.”