Business

Column: How a smart approach to stimulus saved the U.S. economy from the pandemic

When a monetary and financial disaster strikes, policymakers have solely two choices.

One is to guard the monetary system — slicing rates of interest, pumping reserves into the banking sector, stopping huge monetary firms from collapsing. That’s identified typically as financial stimulus.

The opposite is to guard folks — pumping cash into family budgets, strengthening security internet packages resembling unemployment insurance coverage, permitting the federal government to step in because the supply of household revenue when employers abandon them via layoffs and shutdowns. That’s fiscal stimulus.

Members of Congress, opinion leaders, and finally voters determined that the ‘disaster’ of rising public debt represented a extra urgent problem to the nation than hovering long-term unemployment.

Gary Burtless, Brookings Establishment, on the failings of post-Nice Recession stimulus

For many years, economists and politicians have debated which is healthier.

The talk is over. COVID-19 delivered the reply.

Publication

Get the most recent from Michael Hiltzik

Commentary on economics and extra from a Pulitzer Prize winner.

You might often obtain promotional content material from the Los Angeles Occasions.

The U.S. authorities’s $4-trillion outlay to maintain People complete throughout the depths of the pandemic has resulted in a spectacular restoration — certainly, the quickest jobs restoration from the bottom nadir of the 12 American recessions since World Struggle II.

What’s significantly telling is the distinction between the course of this downturn and the final one, the Nice Recession of 2008-09, which on the time was essentially the most extreme recession for the reason that struggle.

In the present day, two years for the reason that U.S. economic system was successfully frozen to struggle a novel coronavirus, nonfarm employment has virtually returned to its degree in February 2020.

Authorities statistics present that on a seasonally-adjusted foundation, employment has reached 150.4 million, about 2.1 million under the 152.5 million degree of two years in the past, a deficit of about 1.4%. That’s a record-shattering restoration from the underside of the freeze in April 2020, when employment abruptly fell by 22 million jobs, or 14.4%, to 130.5 million.

That was the steepest collapse in employment of the postwar period, simply outpacing the 6.3% employment loss from January 2008 to February 2010. Two years into the Nice Recession, nonetheless, employment was nonetheless falling; it wouldn’t return to its pre-recession degree till Could 2014, or about 76 months after the recession started. That was the worst job loss since 1948, and the slowest, longest jobs restoration.

What accounts for the distinction within the two rebounds?

A few of the clarification actually belongs to the distinction between the pandemic stoop and people who got here earlier than it.

Insufficient fiscal stimulus made the post-2007 restoration the longest and slowest of the postwar period, as proven by the variety of months wanted to revive jobs to pre-recession ranges. Potent fiscal stimulus produced a V-shaped restoration from the pandemic lockdowns.

(calculatedriskblog.com)

The Nice Recession started with a collapse within the overheated U.S. housing market, which metastasized all through the worldwide monetary system. The 2020 recession was triggered not by a seizure within the monetary markets, however by a deliberate effort to restrict the type of private contacts identified to contribute to COVID’s unfold, resembling college courses, leisure and journey.

That urged that the downturn might be quick and amenable to authorities motion to restart enterprise as quickly as the specter of the virus handed.

However one other distinction was the character of the federal government response. Drawing on classes discovered from the Nice Despair, policymakers tended to favor financial response in 2008, particularly at first.

The Federal Reserve and different central banks flooded the monetary markets and banks with capital and liquidity. After the collapse of Lehman Bros. in September 2008, they publicly promised that no different main monetary establishment could be allowed to fail.

“Coverage-makers congratulated themselves that that they had averted one other Nice Despair,” noticed UC Berkeley economist Barry Eichengreen for a lecture sequence in 2014.

The restoration effort didn’t precisely lack for fiscal stimulus. The American Restoration and Reinvestment Act, signed by President Obama in February 2009, initially offered $787 billion in funding for will increase within the dimension and length of unemployment advantages, a middle-class tax reduce, and infrastructure building.

Advantages of security internet packages resembling meals stamps have been elevated and expanded, and state governments acquired grants to guard schooling and transportation spending.

But even on the time, economists argued that the funding was too meager to deliver the economic system all the best way again. Issues solely acquired worse from there, because the U.S. and Europe veered towards austerity.

In 2011, Obama agreed to spending cuts of $1.2 trillion over 10 years. In 2013, Obama and a Republican Congress resolved a battle over the federal debt restrict, the Inexpensive Care Act and the specter of a authorities shutdown by enacting the “sequester,” an economically catastrophic legislative maneuver to power an 8.5% reduce in federal spending. “All this took an enormous chunk out of spending, combination demand, and financial development,” Eichengreen wrote.

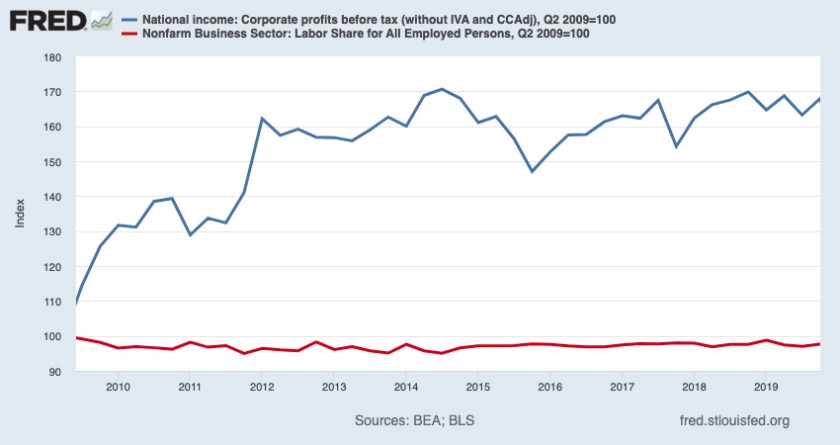

The financial stimulus in place after the Nice Recession helped pump up company earnings (blue line) however left employees’ share of the economic system (crimson line) to stagnate.

(Bureau of Financial Evaluation, through Federal Reserve Financial institution of St. Louis)

The political pushback had begun in 2010, which gave Republicans majority management of the Home and elevated its footprint within the Senate (albeit nonetheless a minority). The final word outcome was a untimely unwinding of fiscal stimulus, which started to be withdrawn effectively earlier than the economic system had recovered.

“This was the one worst error in macroeconomic policymaking following the monetary disaster,” Brookings Establishment economist Gary Burtless wrote, an oft-quoted conclusion.

“For causes which will appear mysterious to future financial historians,” Burtless added, “members of Congress, opinion leaders, and finally voters determined that the ‘disaster’ of rising public debt represented a extra urgent problem to the nation than hovering long-term unemployment and the underutilization of U.S. productive capability.”

Trying again, the financial stimulus might have been too profitable. As soon as the banking system was stabilized in mid-2009, the urgency for additional financial help ebbed. Your complete program was caricatured as a bailout of banks and mortgage debtors, contributing to the rise of the Tea Get together and different conservative critics.

However the classes of the Nice Recession restoration weren’t ignored by policymakers confronting the following disaster. One lesson was that financial stimulus might be very efficient, however for a comparatively slender slice of America. The Federal Reserve’s slashing of rates of interest successfully to zero produced spectacular development in company earnings and inventory market returns within the succeeding dozen years or so.

“A largely financial stimulus left behind a lot of the American inhabitants,” observes funding supervisor and monetary commentator Barry Ritholtz. “The highest 10% of America owns 89% of the general public traded equities; there are 82.51 million owner-occupied houses. Which means that the Federal Reserve response benefited someplace between the highest 10 and prime 25% of People.”

He’s proper. The individuals who have been left behind have been rank-and-file employees. Company earnings have been turbocharged by the low value of capital and debt bestowed on them by the Fed’s rescue of the monetary system, gaining practically 70% from mid-2009 via late 2019. These positive aspects weren’t handed on to employees; labor’s share of the economic system really fell by practically 2% over the identical interval, in response to the federal government’s Bureau of Financial Evaluation.

The construction of the pandemic rescue could be very completely different from that of the Nice Recession. Partly that displays the completely different circumstances: As a result of the pandemic recession isn’t a disaster of the monetary system, financial stimulus is much less wanted. In any occasion, the Federal Reserve used up a lot of its financial ammunition within the Nice Recession that it had little or no left.

It additionally factors to how the sluggish post-2008 restoration rewrote the political texts on financial stimulus. Extra exactly, it revived the orthodoxy that had ruled U.S. financial coverage from the New Deal via the Nineteen Sixties, ending with Reagan conservatism within the Seventies — that authorities has the duty to take care of the economic system, particularly by supporting spending by households, when enterprise withdraws.

Fed Chairman Jerome H. Powell made that very level in testimony to the Senate Banking Committee in December 2020. “Some fiscal help now would actually assist transfer the economic system alongside,” he mentioned then, urging the Senate to go huge: “The danger of overdoing it’s lower than the danger of underdoing it.”

Congress understood. Beginning in March 2020, it handed three fiscal stimulus packages that have been signed into regulation by President Trump and a fourth signed by President Biden, totaling greater than $5 trillion in outlays.

The key packages included the $2.2-trillion CARES Act of March 2020, which included money funds of $1,200 per particular person or extra for many households, a rise in unemployment advantages of $600 every week and loans for small companies —the most important stimulus bundle in American historical past.

That was adopted by a $900-billion bundle in December 2020 that offered $600 money funds to most People and a continuation of the unemployment compensation advantages at $300 every week, after which by the $1.9-trillion American Rescue Plan, signed by Biden in March 2021.

The ARP continued the $300 weekly bump-up in unemployment advantages via the start of September, $1,400 in stimulus funds for many People, a continuation of elevated meals stamp advantages, and a toddler tax credit score of $3,000 per little one youthful than 18 and $3,600 per little one as much as age 6.

The important thing to passing these historic measures might have been their enactment whereas concern of the pandemic and its potential financial influence dominated political discourse.

Because it occurs, additional aid has been inconceivable to move within the present environment of complacency in regards to the pandemic. A $15.6-billion measure aimed toward rising U.S. provides of vaccines, therapies and assessments and battling the illness world wide seems to be headed for extinction by the hands of a recalcitrant Senate.

However the heavy lifting has been executed, and it might effectively present a template for the following financial disaster. The unemployment fee of three.8% is sort of again to the pre-pandemic fee of three.5%, thought-about to be near “full employment.” Retail gross sales surged late final 12 months and in January.

People’ urge for food for items, together with the wherewithal to pay for them, has contributed to shortages and transport logjams which have pushed inflation to a 40-year excessive. Which may be consuming away on the wage positive aspects that American employees have been receiving in current months, nevertheless it’s additionally a sign of a sturdy economic system.

Had the austerity hawks of the final recession been working the restoration this time round, People could be in a lot worse form. Had policymakers had the energy of conviction of at this time’s leaders again in 2009, America would have been even higher positioned to maintain itself via the pandemic, and the price of stimulus might need been a lot decrease.

Let’s hope the teachings of this downturn and the final one are etched in stone, to allow them to present a customers guide for the following one.

Paul F. Oreffice, who as the pugnacious head of Dow Chemical grew and diversified the company at the same time that he rebuffed Vietnam veterans over Agent Orange, argued that the chemical dioxin was harmless and oversaw the manufacturing of silicone breast implants that were known to leak, died on Dec. 26 at his home in Paradise Valley, Ariz. He was 97.

His family confirmed his death.

Mr. Oreffice (pronounced like orifice) spoke in staccato, fast-paced sentences, and they were often deployed in pushing back against environmentalists, politicians and journalists during an era, the 1970s and ’80s, when the environmental movement was gaining force by focusing on toxic chemicals in the air and water.

Under his 17-year leadership, which included the titles of president, chief executive and chairman, Mr. Oreffice weathered intense controversies.

His public relations instinct was for confrontation, not conciliation. He had an intense dislike for what he perceived as government meddling in business, which he traced to his having grown up in Italy under Mussolini. “I’ve seen what overgoverning can do,” he told The New York Times in 1987. “I was born under a Fascist dictatorship, and my father was jailed by it.”

Mr. Oreffice took the reins of the Dow USA division in 1975, when its public image was tainted from campus protests of the 1960s that had vilified the company as a maker of the incendiary agent napalm, which was widely used in Vietnam.

When Dow pulled out of apartheid South Africa in 1987 under pressure from shareholders, Mr. Oreffice said: “I’m not proud of it. I think we should have stayed and fought.”

In 1977, when Jane Fonda lacerated Dow in a speech at Central Michigan University, not far from Dow headquarters, in Midland, Mich., Mr. Oreffice canceled the company’s donations to the school, writing its president that he could not support Ms. Fonda’s “venom against free enterprise.”

Instead, Mr. Oreffice financed the campaigns of anti-regulation politicians. And he sued the Environmental Protection Agency for surveilling Dow’s sprawling Midland plants from the air when the company refused an on-site inspection.

The case made its way to the United States Supreme Court, which in 1986 ruled against the company, at the time the No. 2 American chemical maker after DuPont. (The companies merged in 2017, then split into three companies.)

In 1983, Rep. James H. Scheuer, Democrat of New York, disclosed that Dow had been allowed to edit an E.P.A. report on the leakage of dioxin, one of the most toxic substances ever manufactured, from the Midland plants into the Tittabawassee and Saginaw Rivers and Saginaw Bay.

E.P.A. regional officials told Congress that their superiors in the Reagan administration ordered the changes to comply with demands made by Dow. Mr. Oreffice, appearing on NBC’s “Today” show, offered a sweeping dismissal.

“There is absolutely no evidence of dioxin doing any damage to humans except for causing something called chloracne,” he said. “It’s a rash.”

His statement brushed aside evidence that dioxin was extremely hazardous to laboratory animals and had been shown in some research to be linked with a rare soft-tissue cancer in humans.

One former Dow president, Herbert Dow Doan, a grandson of the company founder, told a public relations publication, Provoke Media, in 1990 that Mr. Oreffice’s style was not one fine-tuned to mollify critics. “The reason is part ego, part pride,” he said. “Paul is inclined to push his line to the point where some people say he is arrogant.”

There is no question that Mr. Oreffice’s strength of will also uplifted Dow’s businesses, which through the 1970s were overly dependent on basic chemicals like chlorine. When a glut of low-priced petrochemicals flooded the global market in the early 80s, he aggressively reshaped Dow by diversifying into consumer products, such as shampoos and the cleaning fluid Fantastik, and by moving into foreign markets. By 1987, Dow posted a record profit of $1.3 billion (about $3.5 billion in today’s currency).

At the same time, a class-action lawsuit on behalf of 20,000 Vietnam veterans and their families against Dow and other makers of Agent Orange was further tarnishing the company’s image. The suit, filed in 1979, charged that dioxin in Agent Orange led to cancer in combat veterans and genetic defects in their children.

Dow argued that it had made Agent Orange at the request of the government and was not responsible for how it was used. But in 1984, the company and other makers of Agent Orange, without admitting liability, settled the lawsuit for $180 million, with the proceeds going to veterans and their families.

In another controversy, Dow Corning, a joint venture between Dow Chemical and Corning Inc., released documents in February 1992 showing that it had known since 1971 that silicone gel could leak from breast implants it made.

Tens of thousands of women had sued the company, claiming their implants had given them breast cancer and autoimmune diseases. Dow Corning agreed to a $3.2 billion settlement after the company had been driven to file for bankruptcy protection.

In 1999, an independent review by an arm of the National Academy of Sciences concluded that silicone implants do not cause major diseases.

Paul Fausto Orrefice was born Nov. 29, 1927, in Venice. His parents, Max and Elena (Friedenberg) Oreffice, moved the family to Ecuador in 1940 as Mussolini declared war on Britain and France. Paul came to the U.S. in 1945, entering Purdue University with fewer than 50 words of English at his command.

He graduated with a B.S. in chemical engineering in 1949, became a naturalized citizen, and after two years in the Army went to work for Dow in 1953.

“When I walked into Midland, Mich., this was ‘WASP’ country, and I was a ‘W’ but I wasn’t an ‘ASP,’” he told The Washington Post in 1986. “I spoke with an accent and combed my hair straight back, which just wasn’t done.”

Mr. Oreffice represented Dow in Switzerland, Italy, Brazil and Spain before being called back to the Midland headquarters in 1969 and appointed the company’s financial vice president. He became president of Dow Chemical U.S.A. in 1975 and was then promoted to president and chief executive of the parent Dow Chemical Company in 1978. In 1986, he added the title of chairman.

To the astonishment of many observers, Dow poured millions of dollars in the mid-1980s into a public-relations campaign to improve its image, including a new slogan, “Dow let’s you do great things.”

Under company rules, when he reached age 60, Mr. Oreffice stepped down as president and chief executive in 1987. He retired as chairman in 1992.

He is survived by his wife of 29 years, Jo Ann Pepper Oreffice, his children Laura Jennison and Andy Oreffice, six grandchildren and one great-granddaughter.

In retirement, Mr. Oreffice pursued a passion for thoroughbred racehorses, investing in Kentucky Derby starters and spending summers at a home in Saratoga Springs, N.Y. He was a partner in a Preakness Stakes winner, Summer Squall, and a Belmont Stakes winner, Palace Malice.

In 2006, he published a memoir about rising from an immigrant with little English to a corporate titan, titling it “Only in America.”

As an enormous plume of dark gray smoke rose hundreds of feet from the nearby Palisades fire on Wednesday afternoon, obscuring the sun and turning everything in the north end of Santa Monica an apocalyptic shade of orange, a small army of hired hands went about their business as if it were just another day on the job.

Amid the tension and anxiety in this normally cozy seaside enclave — Santa Monica looks and feels like an extremely prosperous Midwestern suburb plunked on a cliff overlooking the Pacific Ocean — landscapers kept trimming, builders kept building, and delivery trucks steered around electric cars packed with fleeing residents.

The weather was “fine for trimming trees,” said Adrian Rodriguez, as he tossed a coiled garden hose into the back of an ancient Nissan pickup. “The sparks aren’t falling yet.”

It was 3 p.m., and Rodriguez, who lives in Los Angeles but is originally from Querétaro, Mexico, had already put in an eight-hour day as one of the worst natural disasters in California history raged around him.

Most of his labor was a little farther from the fire line, he stressed.

And that’s how it goes this awful week in west Los Angeles, normally a dreamscape of gorgeous beaches and breathtaking sunsets. Those who seem to have everything you could possibly ask for are justifiably terrified of losing it. Those who don’t must keep working to get by.

A couple of blocks closer to the ocean, on Palisades Avenue, David Salais and an entirely Spanish-speaking crew of construction workers reluctantly pulled their tools from a $13-million (according to Zillow) home. They were loading the stuff into their trucks as a Santa Monica Police Department cruiser rolled by, repeating a mandatory evacuation order from the loudspeaker.

“We work wind, rain, fire, natural disaster. We don’t stop. We just keep on going until the cops kick us out,” Salais said, leaning on his 6-foot-long carpenter’s level and nodding in the direction of the police car.

Salais, from Santa Paula, said he was born in the U.S. and is “half Mexican.” He was the only person in the stream of workers sauntering out of the house who was willing to be interviewed in English, mostly.

Mexicans are wired differently, he joked, gesturing to the guys around him. “Tienen ganas pa trabajar — they really want to work!”

A few blocks south, as residents struggled to shuttle precious keepsakes from their elegant homes — financial documents, irreplaceable family photos, an enormous stand-up double bass — to cars waiting in the street, Marvin Altamirano steered his UPS delivery truck between them.

With a sun visor on backward and a pen stuck in the elastic band, he patiently removed one of his earbuds to better hear a reporter ask why he was still making deliveries.

“We gotta pay bills,” he said. “It’s not like they’re gonna pay us to stop working and leave.”

He had been making deliveries in Pacific Palisades on Tuesday, during the worst of the fire, but hadn’t gotten too close, he said. The smell of smoke was worse in Santa Monica at 3 p.m. Wednesday, he said.

Would he make a delivery if the street were on fire?

“Depends,” he said, with a laugh. “Like, how close is it, really? If it was down the street, yeah, I’d drop it and go.”

Just before the evacuation order reached their worksite, on Marguerita Avenue near Ocean Avenue, a construction crew calmly repaired a damaged balcony at an apartment building, the team’s ladder lashed to the structure to help brace it in the howling wind.

“We have to survive; that’s why we’re still here,” said Josue Curiel, who lives in Inglewood and is originally from Jalisco, Mexico. Everyone on his crew of about half a dozen were also born south of the border.

“If you’re a worker, you’re hungry, so that’s what it is.”

When art works fetch spectacular auction prices, like the record $450.3 million for Leonardo da Vinci’s “Salvator Mundi” in 2017, the world’s focus turns for a moment to the arcane goings-on of the international art trade. But with the market in a downturn for the last two years, there have been few attention-grabbing sales at the world’s two biggest and oldest auction houses, Sotheby’s and Christie’s.

An exception came at November’s marquee auctions of modern and contemporary art in New York, when the world’s media — and social media in particular — were momentarily enthralled by the seeming absurdity of a cryptocurrency investor spending $6.2 million at Sotheby’s for a duct-taped banana. But there is a big difference between $6.2 million and $450.3 million.

Sales at Sotheby’s and Christie’s were down for the second year in a row in 2024, according to preliminary figures released by the companies in December. With both supply and demand for big-ticket art in a slump, the auction houses are making major bets on selling luxury goods and niche experiences to make up the shortfall.

Sotheby’s estimated it would have turned over about $6 billion in auction and private sales by year-end, a decline of 24 percent on 2023. Christie’s announced projected aggregate sales of $5.7 billion, down 6 percent year-on-year. Back in 2022, Sotheby’s and Christie’s posted annual turnover of $8 billion and $8.4 billion.

“The auction houses have major problems,” said Christine Bourron, the chief executive of the London-based company Pi-eX, which analyzes art sale results. “They really need to do some thinking about how they can bring some life into their auction business. People who have an interest in art want to have an experience,” added Bourron, who, like many followers of the auction market, finds both Sotheby’s and Christie’s live and online sales increasingly predictable.

Sotheby’s is owned by the French-Israeli telecoms magnate Patrick Drahi, whose beleaguered Altice group is burdened with $60 billion of debt. Sotheby’s deteriorating performance led the auction house to reach out to Abu Dhabi’s sovereign wealth fund, A.D.Q., for a $1 billion cash-for-equity bailout and to lay off more than 100 employees in December. This followed some costly infrastructure decisions: Sotheby’s $100-million purchase of the Breuer Building in New York’s Madison Avenue, the opening of a new headquarters in Paris and the development of a futuristic exhibition and retail space in Hong Kong.

Sotheby’s website now abounds with opportunities to buy pre-owned luxury items at auction or by “instant purchase,” as if in a store, ranging from real estate, classic cars and dinosaur fossils, to smaller prestige collectibles like designer handbags, jewelry, fine wines and game-worn N.B.A. jerseys.

Josh Pullan, Sotheby’s global head of luxury, said sales of such goods draw in wealthy clients who may, in time, start to buy high-end art. “Luxury categories are for us a vital gateway for new, often younger, collectors,” he added.

Last year, luxury generated about 33 percent of sales at Sotheby’s, compared with 16 percent at Christie’s, according to the companies’ communications teams. But the category attracted more buyers than art did.

Guillaume Cerutti, the chief executive of Christie’s, spoke to reporters last month during an end-of-year media call. “Luxury has an advantage, because of the model and the price points,” he said. “Luxury and art will merge with each other,” he added, hinting at future synergies of presentation and categorization.

Christie’s is owned by the luxury goods billionaire François-Henri Pinault, whose Kering conglomerate has also been hit by flagging sales. After introducing handbag auctions back in 2014, Christie’s is now having to catch up with Sotheby’s offering of luxury items and trophy collectibles, like dinosaur skeletons. In September, Christie’s announced that it had reached an agreement to acquire the California-based classic car auctioneers Gooding & Co., setting up a rivalry with Sotheby’s car business, RM Sotheby’s, which last year turned over $887 million in classic auto sales.

“The luxury resale market presents a compelling opportunity for auction houses,” said Daniel Langer, a professor of luxury strategy at Pepperdine University in Malibu, Calif. “Storytelling is a critical success factor in the luxury industry. Auction houses excel in this area — take the recent banana auction as an example,” he added. Sotheby’s marketing, like that of a luxury brand, had skilfully woven a narrative around the sensation that the banana sculpture, by the Italian artist Maurizio Cattelan, created when first exhibited at the Art Basel Miami Beach fair in 2019.

However, this opportunity comes with “significant challenges,” according to Langer. He pointed out that unlike luxury brands, auction houses don’t produce and price all of their own inventory; profit margins on new luxury items are often much higher than their resold equivalents; and unlike conglomerates such as LVMH and Kering, auction houses can’t scale their transactions through a network of retail outlets. These disparities between retail and resale “could limit the overall financial impact of luxury for auction houses,” he said.

Changing spending patterns among the wealthy could also affect demand.

Global sales of luxury flatlined in 2024 for the first time since 2008 (excluding 2020, during the coronavirus pandemic), according to a recent report by the management consultants Bain & Co. The report’s authors said consumers were prioritizing “experiences over products” in these uncertain times and that the luxury goods market, rather like the art market, is suffering from buyer fatigue.

“The super-wealthy in their 30s, 40s and 50s are spending their money on luxury experiences,” said Doug Woodham, a former Christie’s executive who now advises on art-related finance. “That’s money that isn’t being spent on a Matisse drawing,” he added.

“With superluxury experiences, the social cache is so much higher,” said Woodham, who pioneered handbag sales at Christie’s in 2014. “For half a million dollars I can have my 10 best friends on a lavish yacht. They will remember that more than sitting in my house with a Rothko on the wall.”

The global luxury yacht charter market grew to an all-time high of $16.3 billion in 2024, a 6 percent increase on the previous year, according to the Business Research Company. It said that growth has been driven by the popularity of “exclusive and exotic travel destinations” and the “ongoing trend towards experiential luxury.”

In September, Sotheby’s collaborated with the Marriott International hotel chain and the fashion house Alexander McQueen to offer a sealed bid auction, in which bidders can’t see the rival offers. The winner got a two-night stay one of the group’s 5-star London sites as part of an experience that the Sotheby’s website said would “transport guests to where a teenaged McQueen first learned the art of tailoring.” Also included were a five-course fine-dining meal for two, a bespoke tour of London with a private visit to the Victoria & Albert Museum and a personalized photo session with Ann Ray, a longtime McQueen collaborator. Classifying the auction as a private sale, Sotheby’s declined to reveal how much the winning bidder paid for this unique luxury experience, but the presale estimate was $12,000 to $18,000.

Could selling memories, instead of art, be the future of the auction business?

The Bunny Museum, destroyed by Eaton fire, vows to return

Supreme Court turns down Trump plea to block New York sentencing for hush money conviction

Rams wide receiver Demarcus Robinson charged in DUI case

Falling Chinese bond yields signal concern with deflation

‘Much more persecution’: Venezuela braces for Nicolas Maduro’s inauguration

Colorado Rockies game no. 116 thread: Zac Gallen vs José Ureña

Why Marjorie Taylor Greene was ‘kicked out’ of the Freedom Caucus according to Rep. Buck

See it: Tesla crashes into Columbus convention center at 70 mph

Fox News Politics: Georgia the whole day through

Death of missing Oregon girl found in stream ruled homicide

‘Much more persecution’: Venezuela braces for Nicolas Maduro’s inauguration

Mondale and Ford’s eulogies written for Carter read by sons at funeral

Elon Musk Downplays the Role of Climate in L.A. Fires, Scientists Say

Did moderate Democrats get religion with embrace of Laken Riley Act?

Ramstein: Germany pledges tanks, missiles, and air defence for Ukraine

-

Business1 week ago

Business1 week agoThese are the top 7 issues facing the struggling restaurant industry in 2025

-

Culture1 week ago

Culture1 week agoThe 25 worst losses in college football history, including Baylor’s 2024 entry at Colorado

-

Sports1 week ago

Sports1 week agoThe top out-of-contract players available as free transfers: Kimmich, De Bruyne, Van Dijk…

-

Politics1 week ago

Politics1 week agoNew Orleans attacker had 'remote detonator' for explosives in French Quarter, Biden says

-

Politics7 days ago

Politics7 days agoCarter's judicial picks reshaped the federal bench across the country

-

Politics5 days ago

Politics5 days agoWho Are the Recipients of the Presidential Medal of Freedom?

-

Health4 days ago

Health4 days agoOzempic ‘microdosing’ is the new weight-loss trend: Should you try it?

-

World1 week ago

World1 week agoIvory Coast says French troops to leave country after decades