Again in March, I printed an article on Searching for Alpha wherein I revisited the Invesco Most well-liked Portfolio ETF (PGX), certainly one of my favourite most popular inventory funds. Within the feedback part following the article, a number of readers expressed some concern in regards to the ETF’s heavy publicity to the monetary sector, given the uncertainty swirling round that sector within the wake of current regional financial institution failures. In response to their comprehensible trepidation, I reasoned that it may be time to revisit the VanEck Vectors Most well-liked Securities ex Financials ETF (NYSEARCA:PFXF) since it will allow ETF buyers to purchase into the popular inventory house with out having to fret as a lot in regards to the affect of a possible banking disaster affecting the share value.

I’ve coated PFXF for Searching for Alpha prior to now, and got here away with blended emotions in each of the articles wherein I mentioned the ETF. Within the first of these articles, I thought-about PFXF alongside two of its opponents. Within the second article, I took a better have a look at the fund by itself and noticed what, on the time, struck me as an intriguing alternative for buyers wanting so as to add a most popular inventory ETF to their portfolios. In the present day, I shall be re-evaluating PFXF as an funding possibility for fastened earnings buyers cautious of the financials sector.

Why Spend money on Most well-liked Inventory?

Earlier than continuing to a better have a look at PFXF, it’s a good suggestion to overview the distinctive qualities of most popular shares for readers who could also be unfamiliar with this explicit kind of funding. Most well-liked inventory is a somewhat uncommon kind of fairness which may finest be described as a hybrid funding car combining traits related each with bonds and customary inventory. Like bonds, most popular shares are likely to enchantment to income-oriented buyers searching for a gradual, predictable stream of money. Whereas most popular inventory can respect or depreciate, shares have a par worth that tends to stop them from buying and selling exterior of a relatively slender value vary. Thus, most popular inventory not often gives buyers a lot in the way in which of capital appreciation. As an alternative, it gives buyers a considerable yield, usually properly in extra of 5%. Moreover, most popular stockholders get pleasure from preferential remedy within the occasion of an organization’s monetary misery. If, for example, an organization should liquidate its property to pay its collectors, bondholders shall be paid first, adopted by most popular stockholders. Widespread stockholders will get no matter is left, if something. Equally, when an organization suspends or cuts its dividend to widespread shareholders, most popular stockholders will proceed receiving their checks. Lastly, most popular stockholders usually profit from certified dividends which are labeled as capital good points somewhat than unusual earnings.

Advertisement

Why Most well-liked Inventory Could Not Be Proper For You

As I discussed above, most popular inventory nearly by no means gives buyers important capital appreciation. Thus, in case you’re searching for progress, you’d finest look elsewhere. One other disadvantage to most popular inventory that buyers might need to take into account is the very actual risk that an organization will difficulty a share name. Like bonds, most popular inventory typically has a maturity date set a long time sooner or later. Nonetheless, after 5 years, an organization can name the excellent shares of its most popular inventory, which they are going to usually do whether it is financially advantageous for them to take action. They will pay you the present market value and you will have misplaced an earnings stream. A 3rd consideration buyers will need to remember earlier than shopping for most popular inventory is rate of interest sensitivity: when rates of interest go up, the enchantment of most popular inventory tends to weaken. In a rising curiosity surroundings, widespread inventory turns into extra interesting as a result of they will supply increased yields whereas the fastened yield of most popular inventory might even pull their share costs down–and costs can drop onerous. With the Fed slashing rates of interest this 12 months, this final consideration won’t appear all that urgent, however it’s properly price taking into consideration when taking a look at most popular inventory.

What Makes PFXF So Particular?

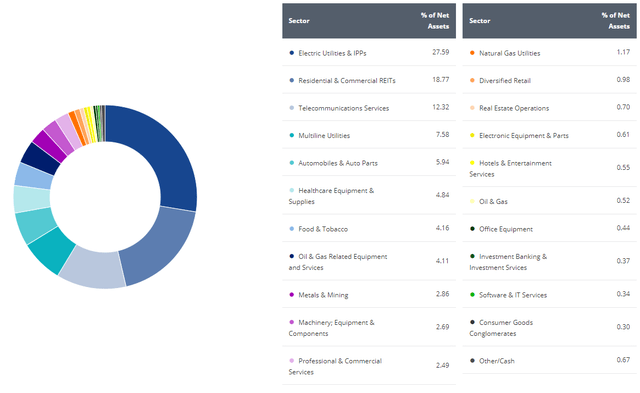

As a result of monetary establishments have a tendency to supply most popular inventory at a better fee than different corporations, most popular inventory ETFs regularly include very excessive concentrations of most popular inventory provided by banks. For buyers cautious of the monetary sector, they might need to keep away from ETFs that may be significantly vulnerable to disruption in that individual market sector. PFXF gives buyers a possibility to put money into most popular inventory with none publicity to the monetary sector in any respect. Monitoring the Wells Fargo Hybrid and Most well-liked Securities ex Financials Index, PFXF’s holdings are diversified throughout a number of market sectors:

VanEck

For buyers searching for publicity to the popular inventory market past the somewhat slender confines of the monetary sector, PFXF gives a compelling funding alternative. The biggest sector allocation, Electrical Utilities & IPPs, quantities to lower than 28% of the fund’s holdings whereas solely two different sectors (REITs and telecommunications) even surpass 10% of the fund’s holdings. The ETF’s remaining holdings, cut up amongst 18 different sectors, account for almost 40% of its weighting. For buyers seeing a properly diversified most popular inventory ETF whereas avoiding the monetary sector, PFXF seems to current an intriguing funding alternative.

Nonetheless…

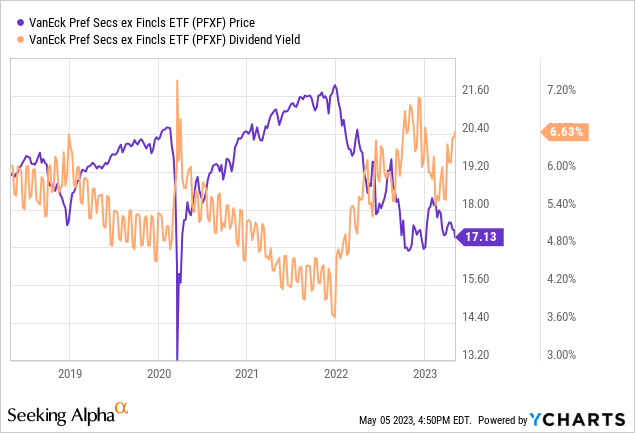

Whereas first look PFXF does look interesting, given its hefty yield north of 6.5%, the fund’s present value is decrease than it has been at any level within the final 5 years aside from a quick plunge on the peak of the Covid-19 lockdowns within the spring of 2020:

Advertisement

Information by YCharts

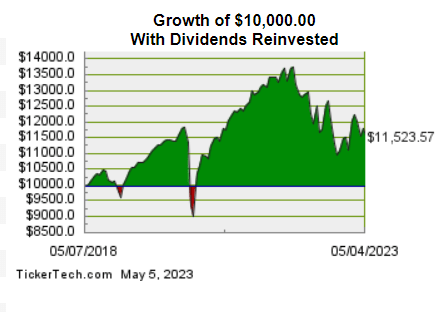

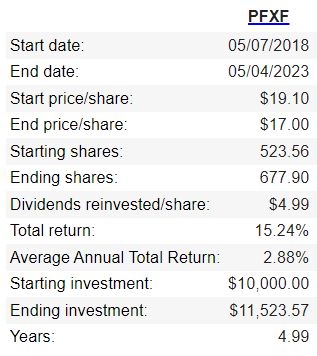

Thus, PFXF’s excessive yield corresponds with a loss in worth. Consequently, the ETF’s complete return over the previous 5 years has been disappointing. For example simply how uninspiring PFXF’s complete returns have been, we will have a look at how a lot a $10,000 funding made in Could 5 years in the past, with all dividends reinvested, can be price at present:

Picture created by creator with instruments at dividendchannel.com

With a beginning value of $19.10 per share and a value of $17.13 at present, that preliminary $10,000 funding can be price $8,968.59 in 5 years. With dividends reinvested, nonetheless, an investor can be within the inexperienced with $11,523.57, for a complete return of 15.24%:

Picture created by the creator with instruments at dividendchannel.com

Even with reinvested dividends, we discover that the present complete worth of that preliminary $10,000 funding can be underwhelming. Because it stands, PFXF’s common annual complete return is 2.88%, which is considerably decrease than the fund’s yield has been at each single level over that very same time span.

Advertisement

Then once more…

In fact, nobody ought to take into account shopping for most popular inventory ETFs for capital appreciation. Individuals purchase PFXF for a gradual stream of fastened earnings and it clearly has accomplished its job on that entrance. Whereas a median annual return south of three% is disappointing for widespread equities, buyers in VanEck’s ETF have loved a money stream that exceeded each excessive yield financial savings accounts and all however essentially the most beneficiant CDs over the previous 5 years. Presuming the businesses issuing the popular shares in PFXF’s basket stay wholesome, the fund’s payouts ought to proceed with none interruption.

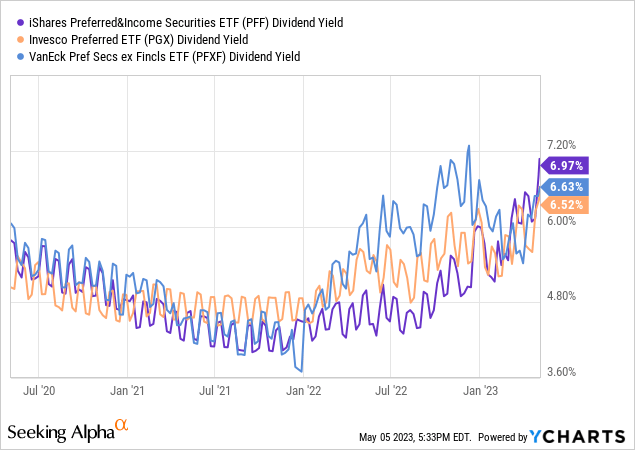

Moreover, given the fund’s deliberate avoidance of most popular shares issued by monetary establishments, PFF’s present yield is comparable with the 2 hottest most popular inventory ETFs within the financials sector, PGX and PFF:

Information by YCharts

Thus, PFXF gives considerably extra diversification than such in style ETFs as PGX and PFF whereas additionally providing a yield on par with these extra regularly traded funds.

One Final Consideration

Moreover, PFXF has a big disadvantage that the monetary sector-focused ETFs don’t: lower than 10% of its dividends are certified. In contrast with the aforementioned PGX and PFF, PFXF’s proportion of certified dividends is a fairly low at round 10%. As such, the overwhelming majority of the ETF’s present yield of 6.63% shall be taxed as common earnings, leading to even much less money on the finish of the day.

A second consideration buyers might want to remember when deciding if PFXF is the correct most popular inventory ETF for his or her portfolios is the fund’s somewhat excessive proportion of necessary convertibles. Not like PFF, which has about 11% of its holdings in necessary convertibles or PGX, which doesn’t have any such holdings, PFXF has almost one quarter of its holdings in necessary convertibles. As a result of these shares convert to widespread fairness, they inject a level of danger into PFXF that may end up in the type of volatility conservative fixed-income buyers consciously search to keep away from.

Advertisement

Concluding Ideas

For ETF buyers searching for publicity to most popular shares however feeling cautious of disruptions within the monetary sector, then PFXF could also be a good selection. The ETF’s yield is properly north of 6%, although provided that solely about 10% of PFXF’s dividends are certified, that yield will successfully be decrease after taxes are considered. At current, I fee PFXF a maintain, although at present value ranges I might not blame anybody for snatching up a number of shares to seize the excessive yield.

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

A St Petersburg court has seized over €700mn-worth of assets belonging to three western banks — UniCredit, Deutsche Bank and Commerzbank — according to court documents.

The seizure marks one of the biggest moves against western lenders since Moscow’s full-scale invasion of Ukraine prompted most international lenders to withdraw or wind down their businesses in Russia. It comes after the European Central Bank told Eurozone lenders with operations in the country to speed up their exit plans.

The moves follow a claim from Ruskhimalliance, a subsidiary of Gazprom, the Russian oil and gas giant that holds a monopoly on pipeline gas exports.

Advertisement

The court seized €463mn-worth of assets belonging to Italy’s UniCredit, equivalent to about 4.5 per cent of its assets in the country, according to the latest financial statement from the bank’s main Russian subsidiary.

Frozen assets include shares in subsidiaries of UniCredit in Russia as well as stocks and funds it owned, according to the court decision that was dated May 16 and was published in the Russian registrar on Friday.

According to another decision on the same date, the court seized €238.6mn-worth of Deutsche Bank’s assets, including property and holdings in its accounts in Russia.

The court also ruled that the bank cannot sell its business in Russia; it would already require the approval of Vladimir Putin to do so. The court agreed with Rukhimallians that the measures were necessary because the bank was “taking measures aimed at alienating its property in Russia”.

On Friday, the court decided to seize Commerzbank assets, but the details of the decision have not yet been made public so the value of the seizure is not known. Ruskhimalliance asked the court to freeze up to €94.9mn-worth of the lender’s assets.

Advertisement

The dispute with the western banks began in August 2023 when Ruskhimalliance went to an arbitration court in St Petersburg demanding they pay bank guarantees under a contract with the German engineering company Linde.

Ruskhimalliance is the operator of a gas processing plant and production facilities for liquefied natural gas in Ust-Luga near St Petersburg. In July 2021, it signed a contract with Linde for the design, supply of equipment and construction of the complex. A year later, Linde suspended work owing to EU sanctions.

Ruskhimalliance then turned to the guarantor banks, which refused to fulfil their obligations because “the payment to the Russian company could violate European sanctions”, the company said in the court filing.

The list of guarantors also includes Bayerische Landesbank and Landesbank Baden-Württemberg, against which Ruskhimalliance has also filed lawsuits in the St Petersburg court.

UniCredit said it had been made aware of the filing and “only assets commensurate with the case would be in scope of the interim measure”.

Advertisement

Deutsche Bank said it was “fully protected by an indemnification from a client” and had taken a provision of about €260mn alongside a “corresponding reimbursement asset” in its accounts to cover the Russian lawsuit.

“We will need to see how this claim is implemented by the Russian courts and assess the immediate operational impact in Russia,” it added.

Bayerische Landesbank and Landesbank Baden-Württemberg both declined to comment. Commerzbank did not immediately respond to a request for comment.

Italy’s foreign minister has called a meeting on Monday to discuss the seizures affecting UniCredit, two people with knowledge of the plans told the Financial Times.

UniCredit is one of the largest European lenders in Russia, employing more than 3,000 people through its subsidiary there. This month the Italian bank reported that its Russian business had made a net profit of €213mn in the first quarter, up from €99mn a year earlier.

Advertisement

It has set aside more than €800mn in provisions and has significantly cut back its loan portfolio. Chief executive Andrea Orcel said this month that while the lender was “continuing to de-risk” its Russian operation, a full exit from the country would be complicated.

The FT reported on Friday that the European Central Bank had asked Eurozone lenders with operations in the country for detailed plans on their exit strategies as tensions between Moscow and the west grow.

Legal challenges over assets held by western banks have complicated their efforts to extricate themselves. Last month, a Russian court ordered the seizure of more than $400mn of funds from JPMorgan Chase following a legal challenge by Kremlin-run lender VTB. A court subsequently cancelled part of the planned seizure, Reuters reported.

Additional reporting by Martin Arnold in Frankfurt

Prosecution of Binance held up as example of success.

Investment needed to train enforcement professionals.

The US Department of the Treasury this week released its 2024 report on illicit finance, examining threats of money laundering and terrorist financing and its strategies to combat them.

The Treasury cited professional money launderers, financial fraudsters, cybercriminals and those seeking to finance terrorism as ongoing threats to the US financial system.

The 44-page report said anti-money laundering/countering the financing of terrorism (AML/CFT) efforts must continue to adapt in order to be effective.

Among the vulnerabilities cited were obfuscation tools and methods such as mixers and anonymity-enhancing coins, AML/CFT compliance deficiencies at banks and complicit professionals who help facilitate illicit financial activity.

The Treasury cited the prosecution of Binance as an example of its success in supervising virtual asset activities.

Binance failed to prevent criminals, sanctioned entities, and other bad actors from laundering billions of dollars in dirty money, according to court papers. The company pleaded guilty and agreed to pay $4.3 billion in fines and restitution, DL News reported.

Advertisement

Additionally, Binance co-founder Changpeng Zhao was sentenced to four months in federal prison for violating US banking laws and fined $50 million.

The US must continue “to invest in technology and training for analysts, investigators, and regulators to develop further expertise related to new technologies, including analysis of public blockchain data,” the report said.

Join the community to get our latest stories and updates

Such expertise is crucial to the government’s ability to develop responses to new ways in which criminals misuse “virtual assets and other new technologies to profit from their illicit activity,” it said.

SAN BERNARDINO, Calif. (KABC) — The former finance director of the city of San Bernardino is alleging she was threatened and fired by the current city manager, after raising concerns about the potential cost of a project to renovate the old city hall building.

Barbara Whitehorn made the allegations during the public comment portion of the city council meeting on May 15.

“I came back from vacation today, and I was fired today,” said Whitehorn, at times tearing up while making her statement. “I am no longer in the employ of the city of San Bernardino after being threatened today (by the city manager) of having information damaging to my career released into the public domain.

“Then after saying, ‘Please do so, Mr. city manager, because you’ll have to fire me before doing that, he said, ‘Oh, then I’ll just fire you without cause.’”

Whitehorn alleges that the costs to retrofit the old city hall building are spiraling out of control. The building has sat empty since late 2016 after being vacated over concerns that it could collapse during a big earthquake.

Advertisement

“It’s a project that has expanded from $80 million to about $120 million and that number is nowhere to be seen on this (public) agenda. This city does not have that money,” she said.

A presentation was made to the city council in January 2024 outlining the process by which city hall would be retrofitted. City manager Charles Montoya said the city is currently incurring increasing costs for leasing space in separate buildings to maintain city services.

“If we don’t do this now, sooner or later that building is just going to become a gigantic door stop,” said Montoya during the meeting.

He acknowledged when asked by city council members that there is no projected final cost for the project yet.

“The reason we’re doing it this way is speed, to get this thing done. Our lease in the city building is up in two years; we don’t want to sign another lease where we’re just throwing money out the window.”

Advertisement

Two days after her appearance before the council, the city released a statement in response to Whitehorn’s remarks.

The statement claimed Whitehorn was fired for reasons unrelated to the city hall project and disputed some of her other claims.

“However, contrary to Whitehorn’s claims, the renovation project has yet to be designed, and construction costs have yet to be determined,” read the statement, attributed to Public Information Officer Jeff Kraus. “Construction cost estimates and project financing options will be presented to the Council during future meetings.”

“The City of San Bernardino has confirmed that Whitehorn was an at-will employee and was terminated for cause involving financial issues that were unrelated to the City Hall project.”

The statement also said discussion of the city hall project was postponed from that night’s council agenda because there was not enough time to consider the matter and hear from the public.

:quality(70)/cloudfront-eu-central-1.images.arcpublishing.com/dlnews/J3B5VUB4AJBETGDNWVTTBSEACE.jpg)