Business

Verizon is bringing back unlimited data

Verizon (VZ) is bringing again an infinite knowledge plan.

Beginning Monday, Verizon prospects can get limitless knowledge, discuss and textual content for $80.

The corporate says the brand new introductory plan additionally consists of as much as 10 GB of cellular hotspot utilization, in addition to calling and texting to Mexico and Canada. It is going to additionally enable prospects to stream limitless HD video, thumbing its nostril at T-Cellular’s controversial follow of reducing video high quality for a few of its limitless knowledge prospects.

Though the brand new Verizon plan guarantees “quick LTE speeds,” these utilizing quite a lot of knowledge could undergo. The corporate stated that after a buyer makes use of 22 gb of knowledge on a line throughout any billing cycle, it “could prioritize utilization behind different prospects within the occasion of community congestion.” That has turn out to be customary follow on all networks that provide limitless knowledge plans.

Associated: T-Cellular and Dash provide new ‘limitless’ knowledge plans — kind of

Verizon first eradicated its model of an infinite utilization plan in 2011, following comparable choices by different main wi-fi carriers.

However corporations have been steadily reviving such plans.

Verizon first overhauled its data-usage plans final summer time when it launched a brand new “Security Mode” plan. That technically gave prospects entry to limitless knowledge, however they had been subjected to slow-as-molasses speeds after they went over their allotted knowledge.

AT&T equally eradicated overage charges for purchasers in September. Like Verizon, AT&T throttles prospects speeds as soon as they attain the info restrict on their plans. The corporate introduced again limitless plans earlier final 12 months, however it is just accessible for properties with each AT&T’s wi-fi telephone service and both DirecTV or U-Verse TV.

In the meantime, opponents T-Cellular (TMUS) and Dash (S) made their very own bids to draw prospects searching for “limitless knowledge” plans.

Almost all NYC subways get cell service

Final August, Dash started providing a plan to offer prospects limitless discuss, textual content and high-speed knowledge for $60 for the primary line, $40 for the subsequent, and $30 for every extra as much as 10.

The T-Cellular plan, introduced the identical day as Dash’s, charged $70 a month for the primary line, the second at $50 and extra traces are solely $20, as much as eight traces.

CNNMoney (New York) First printed February 12, 2017: 7:03 PM ET

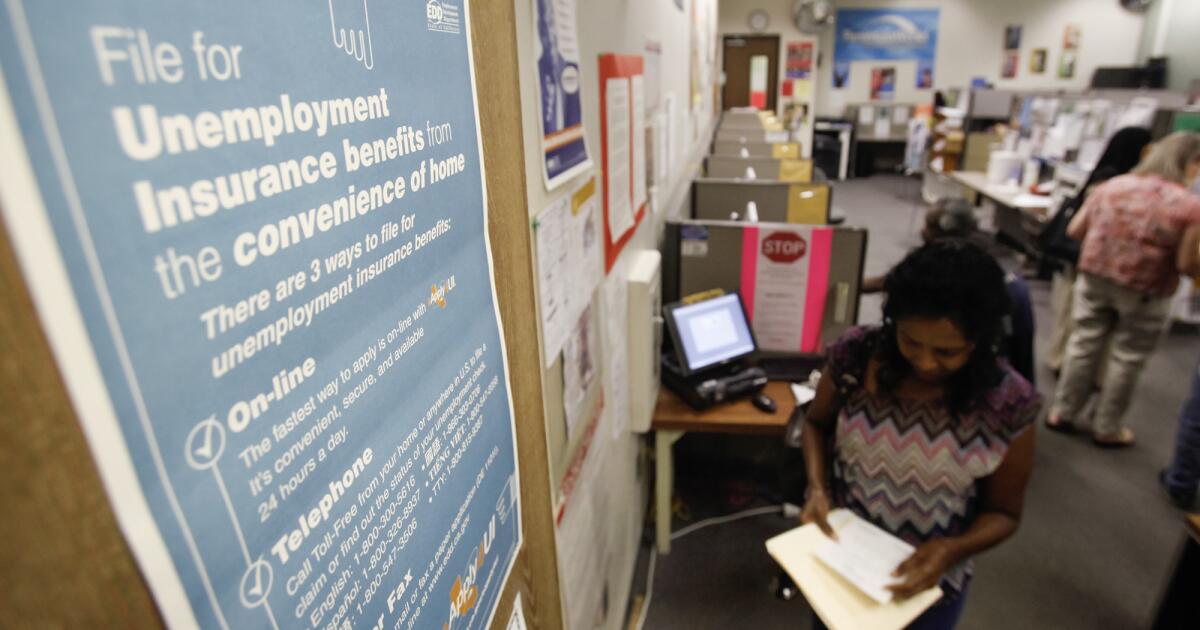

California posted another month of anemic job growth in April, keeping the state’s unemployment rate the highest in the country, 5.3%, the government reported Friday.

Statewide, employers added a net of just 5,200 jobs in April, down from 18,200 in March, according to California’s Employment Development Department.

Nationwide, employers added 175,000 jobs in April and 315,000 in March. The U.S. unemployment rate in April was 3.9%.

Major sectors of California’s economy — including manufacturing, information and professional and business services — showed job losses last month, and job opportunities aren’t as plentiful as before, even as the number of unemployed workers in the state has risen by 164,000 over the last 12 months.

In California, there were 140 unemployed workers for every 100 job openings in March, according to federal statistics released Friday. Less than two years ago, there were about two openings for every jobless person.

Carol Jackson, an unemployed worker in South Los Angeles, says she has been pounding the pavement for months, hoping to make use of her recently minted associate degree in web management and database administration. But despite sending her resume to at least 100 employers, she has not had a single interview.

“I can tell you that California is pretty brutal now,” said Jackson, 57.

Hiring in California has been lagging behind national trends, with one notable exception. The state’s healthcare and social assistance sector added 10,100 jobs last month, bringing the gains over the last 12 months to about 155,000. That’s 75% of all new jobs added since April 2023.

Hospitals and doctors’ offices have been bulking up, but the fastest growth has been at outpatient centers, home healthcare firms, nursing facilities and, especially, social assistance, which includes vocational rehabilitation and child day-care services.

“Healthcare is the big gorilla in the room; it dominates everything,” said Mark Schniepp, director of the California Economic Forecast in Santa Barbara, adding that it’s likely to keep growing robustly with new and expanded medical facilities across the state.

Leisure and hospitality businesses added 3,100 jobs last month. The gains included employment at hotels and restaurants — despite the added stress employers are feeling from a minimum wage increase to $20 an hour for fast-food workers that went into effect April 1.

While there are fears of layoffs as the food industry adopts technology to replace workers, California’s restaurants are getting a lift from a pickup in tourism. The leisure sector overall is close to fully recovering from the deep losses caused by the COVID-19 pandemic.

Public-sector payrolls also held up well last month, increasing by 2,600. Thus far, state and local government jobs seem to be showing little effects from California’s massive budget deficits.

“But clearly that will be another factor,” said Sung Won Sohn, economics professor at Loyola Marymount University in Los Angeles.

Sohn and other economists worry that there are national, cyclical and state-specific threats to California’s employment and broader economic outlook.

Key pillars of the state’s economy continue to struggle.

Motion picture producers and other employers in the information sector show few signs of breaking out of the hiring doldrums, despite the film industry’s resolution of labor strikes last fall. Los Angeles’ motion picture and recording studio industries were down by 13,400 employees, or 12%, in April compared with the same month a year earlier. And many workers in the industry say conditions do not appear to be improving.

Large parts of the farm economy in the Central Valley remain sluggish, in part due to rising costs, tighter financial conditions and ongoing climate challenges.

Despite strong investments in artificial intelligence, layoffs have persisted at high-tech firms in the Bay Area and elsewhere. Scientific and technical companies shed jobs last month, and employment at computer systems design work and related services has been gradually declining.

Nationally, economists expect job growth to slow in the coming months, the result of persistently high interest rates and an expected pullback from consumers. The outlook is particularly dim in California.

“On the ground, there are several signs of even more slowdowns,” said Michael Bernick, an employment lawyer at Duane Morris in San Francisco and former director of the state’s EDD. Among them, he said, “small businesses continue to struggle statewide with higher prices and tightened consumer spending.”

He and other experts have a similar refrain about what ails the state: high costs, excessive regulation and unaffordable home prices, among other factors.

“We just have real challenges here in California that other states don’t face,” said Renee Ward, founder of Seniors4Hire.org, a Huntington Beach-based organization that helps older workers find employment.

She said the number of job seekers registered with her service has jumped 26% so far in 2024 from a year ago.

A New Mexico judge is weighing whether to dismiss involuntary manslaughter charges against Alec Baldwin for his alleged role in the 2021 shooting death of the “Rust” movie cinematographer.

Baldwin’s attorneys argued during a court hearing Friday that special prosecutor Kari T. Morrissey had abused her power by allegedly withholding “significant evidence,” including witnesses favorable to Baldwin, during a January grand jury proceeding.

The 66-year-old actor‘s lawyers said he was a victim of an “overzealous prosecutor” who steered grand jury proceedings in an effort to win an indictment in the high-profile case. At issue is whether the grand jury had been fully advised that they could hear from Baldwin’s witnesses during the proceedings. The grand jurors spent a day and a half questioning witnesses who were introduced by the prosecutors.

“The fix was in,” Baldwin attorney Alex Spiro told the judge Friday.

The grand jury indicted Baldwin on an involuntary manslaughter charge in the shooting death of Halyna Hutchins, the 42-year-old cinematographer, who was rehearsing a scene with Baldwin on Oct. 21, 2021. Baldwin has pleaded not guilty.

At the conclusion of Friday’s hearing, New Mexico First Judicial District Judge Mary Marlowe Sommer said she would issue her ruling next week. Should she dismiss the case, it would mark the second time that the felony charges against Baldwin were dropped.

Marlowe Sommer’s decision is expected less than two months before Baldwin is scheduled to go on trial in a Santa Fe courtroom.

During the hearing, which was conducted virtually, Morrissey denied that she had acted in bad faith. She said she didn’t prevent jurors from getting answers to their questions or from seeking additional information. She told the judge that grand jurors had been given written instructions that outlined their ability to quiz other witnesses, including those favorable to the defense.

But because the jurors didn’t ask to hear from the witnesses who were on a list supplied by Baldwin’s lawyers, several key figures in the tragedy, including film director Joel Souza, property master Sarah Zachry and assistant director David Halls, were not called to testify. Instead, jurors heard from police officers, a crew member who was in the church and expert witnesses hired by prosecutors.

On the day of the shooting, Hutchins, Baldwin, Souza and about a dozen other crew members were gathered in an old wooden church at Bonanza Creek Ranch, south of Santa Fe, preparing for a scene. Hutchins, according to the actor, told him to pull his Colt .45 revolver from his holster and point it at the camera for an extreme close-up view. That’s when the gun went off.

Hutchins died from her wounds. Souza was injured and recovered.

Last month, Marlowe Sommer sentenced the film’s armorer, Hannah Gutierrez, to 18 months in a New Mexico women’s prison for her role in the shooting. Morrissey argued that Gutierrez was criminally negligent by allegedly bringing the live ammunition to the movie production and unwittingly loading one of the lead bullets into Baldwin’s gun. Gutierrez denies bringing the ammunition on set.

Baldwin’s prosecution has long been fraught.

Morrissey and her law partner Jason J. Lewis joined the case last year after the first team of prosecutors was forced to step down due to missteps, including trying to charge Baldwin on a penalty enhancement that wasn’t in effect at the time of the tragedy.

“The government looked a little sophomoric and unprofessional when they charged him for a crime that wasn’t a crime at the time,” said Los Angeles litigator Tre Lovell, who is not involved in the “Rust” shooting matter. “That was embarrassing.”

The original prosecutors also displayed bluster in media interviews, making statements about the need to hold Baldwin responsible for his actions. Defense attorneys have argued that such commentary was out of line and prejudicial against the actor.

Shortly after Morrissey and Lewis joined the case, they dropped the charges against Baldwin. At the time, they said they needed more time to review evidence and address issues raised by Baldwin’s team. Morrissey and Lewis reserved the right to refile the charges.

Immediately after the charges were dropped, Baldwin traveled to Montana to finish the filming of “Rust.”

On Friday, Morrissey said last year’s decision to drop the charges was made at the request of Baldwin’s lead attorney, Luke Nikas, who had presented evidence that the gun Baldwin was using had been modified. Subsequent tests showed the gun was functional that day, but during FBI testing in 2022, the gun was broken by forensic analysts who wanted to see how much pressure needed to be applied for the hammer to drop.

The damaged gun is one of several complications that prosecutors are facing. Legal experts have said that winning a conviction in Baldwin’s case is expected to be more difficult than in the trial of Gutierrez, whose job was to make sure the weapons were safe.

Baldwin was handed the prop gun that day and was told that it was “cold,” meaning there was no ammunition inside. In reality, the chamber of the revolver contained six rounds — five so-called dummies and the lead bullet that killed Hutchins.

“The state has not even alleged that Baldwin had a subjective awareness of a substantial risk that the firearm held live ammunition,” Nikas argued in the motion to dismiss the charges. “Without a subjective awareness, he could not have committed the crime of involuntary manslaughter, which requires that the defendant consciously disregarded a substantial and unjustifiable risk that his actions could cause another person’s death.”

Baldwin has argued, with support from Hollywood’s performers’ union SAG-AFTRA, that it wasn’t his job to be the gun safety officer on set.

The actor has said he was relying on other professionals to do their jobs to ensure a safe production.

Prosecutors have an obligation to present evidence in a “fair and impartial manner,” Baldwin’s attorneys said.

The judge grilled Morrissey on her thinking at the time, including an instance when she had interrupted a sheriff’s deputy and prevented her from answering a question about gun safety measures on set. Morrissey said that deputy was not an expert in film set protocols and that she instead wanted jurors to get “the most accurate information,” which would come from a veteran film crew member who was an expert witness.

Baldwin’s attorneys were also sharply critical of Morrissey for divulging during a media interview the date the grand jury was expected to meet. Morrissey said she took responsibility for providing to a reporter the initial date, which had been scheduled for mid-November. However, the matter was postponed, and the case wasn’t brought before the grand jury until two months later, in mid-January.

Lovell, the L.A. entertainment attorney, said he believes the case will go to trial and that efforts to throw out the indictment will be unsuccessful.

“Courts are really reluctant to dismiss cases brought by a grand jury,” Lovell said. “Courts have limited ability to review what goes to a grand jury unless it was provided in bad faith.”

In an effort to stave off bankruptcy, electric-vehicle maker Fisker Inc. is closing its Manhattan Beach headquarters and has secured a $3.5-million lifeline as it continues to explore an acquisition or other strategic alternative.

The troubled company, which had about 300 employees in the 72,000-square-foot offices at the end of March, is moving its remaining workers to an engineering and distribution facility in La Palma in Orange County, said a person familiar with Fisker’s operations who was not authorized to comment.

In all, the company had roughly 1,135 employees as of mid-April, following an announced 15% cut to its workforce.

Fisker has been attempting to avoid bankruptcy since March, when it announced that talks over a strategic alliance with a major automaker had ended, squelching a deal that would have given it $150 million in new financing.

That caused its shares to collapse to pennies, prompting the New York Stock Exchange to delist the stock, which violated another debt agreement the company struck with an investor last year, according to a regulatory filing.

A major automaker, said to be Nissan, was reportedly in talks to invest in Fisker. Nissan was considering making the Fisker Alaska truck at a U.S. plant — a deal that would come with a $400-million investment, Reuters first reported. Fisker did not confirm the reports.

Fisker announced this week that it secured a $3.5 million short-term loan, as it continues to operate and sell its midsize Ocean SUV. The note is due June 24 and has the potential to increase to $7.5 million.

The Ocean, a competitor to Tesla’s Model Y, was released last year to mixed reviews; some praised its build and styling, but the car has been plagued by software glitches.

The National Highway Traffic Safety Administration has four investigations into the vehicle, including one opened this month after complaints that the SUV’s automatic emergency braking system randomly triggered.

Other probes are looking into reports that a door on the Ocean will not open and complaints about a loss of braking performance. The company has said it is working with the regulator.

Fisker said this week that it had added three dealers to its networks in California and New Jersey, which it began building after a plan to sell direct to consumers — like Tesla does — didn’t pan out. It also announced additional price cuts on some Ocean models.

In March, Fisker slashed the price on its entire lineup of 2023 Oceans by more than 30%. The company also said that it had paused production at its contract manufacturing plant in Austria, which produced about 10,200 Oceans last year.

Fisker was founded in 2016 by noted car designer Henrik Fisker, who has said the Ocean was inspired by California. The SUV features a full-length solar roof, an interior composed of “vegan” recycled plastic and a drop-down rear window that can fit a surf board.

Fisker is not the only startup that has been struggling amid a slowdown in the domestic market for electric vehicles and a rise in interest rates.

Rivian Automotive, an Irvine maker of electric trucks, has informed state officials it will lay off more than 120 employees beginning in June. In February, the company announced it was cutting 10% of its workforce. The company’s shares have lost more than half of their value since last year.

Countries wooing corporate digital nomads hope to make them stay

Sanchez: “I will recognise the Palestinian state next Wednesday”.

Boeing's troubled Starliner spacecraft launch is delayed again

Riley Gaines unleashes on red state Dem candidate after footage reveals 'ignorant' stance on school sports

Missouri Sen. Josh Hawley defends 'friend' Harrison Butker after 'out of touch' left's 'absurd meltdown'

See it: Tesla crashes into Columbus convention center at 70 mph

Colorado Rockies game no. 116 thread: Zac Gallen vs José Ureña

Fox News Politics: Georgia the whole day through

Death of missing Oregon girl found in stream ruled homicide

At least 2 dead as tornadoes hit Alabama, damage homes across Southeast

Sanchez: “I will recognise the Palestinian state next Wednesday”.

Boeing's troubled Starliner spacecraft launch is delayed again

London mayor urges foreign leaders to condemn Trump as racist, sexist, homophobic

Russian court seizes two European banks’ assets amid Western sanctions

Six-month-old baby shot repeatedly during Arizona standoff with child’s father

-

Politics1 week ago

Politics1 week agoOhio AG defends letter warning 'woke' masked anti-Israel protesters they face prison time: 'We have a society'

-

Finance1 week ago

Finance1 week agoSpring Finance Forum 2024: CRE Financiers Eye Signs of Recovery

-

Politics1 week ago

Politics1 week agoBiden’s decision to pull Israel weapons shipment kept quiet until after Holocaust remembrance address: report

-

World7 days ago

World7 days agoIndia Lok Sabha election 2024 Phase 4: Who votes and what’s at stake?

-

News1 week ago

News1 week agoThe Major Supreme Court Cases of 2024

-

News1 week ago

News1 week agoTornadoes tear through the southeastern U.S. as storms leave 3 dead

-

World1 week ago

World1 week agoA look at Chinese investment within Hungary

-

Politics1 week ago

Politics1 week agoTales from the trail: The blue states Trump eyes to turn red in November