Alaska

Alaska Air Stock: Poised To Regain Financial Leadership (NYSE:ALK)

Bradley Caslin /iStock Editorial by way of Getty Pictures

Alaska Air Group (NYSE:ALK) has not too long ago supplied buyers with optimism that the Seattle-based airline is about to guide the {industry} not simply in rebuilding post-Covid but additionally in restoring Alaska’s place of economic management within the {industry}, a place ALK had for years however misplaced pre-Covid. ALK’s not too long ago introduced 1Q2022 GAAP web lack of $143 million ($1.14/share), which was higher than expectations, was a part of industry-wide income optimism and expectations for a return to monetary normality for the beleaguered airline {industry}. Whereas the week by which ALK introduced its monetary outcomes resulted in airline {industry} shares outperforming the broader market, many buyers are questioning how sustainable airline earnings are – and if airways is perhaps a uncommon {industry} that may outperform anticipated broader market challenges over the following few quarters. Certainly, to this point this week, ALK and most different airline shares have given up vital good points. On this article, we’ll take a look at ALK’s place within the {industry} and historical past in addition to how Alaska compares to different airways and its expectations within the close to to medium time period. Alaska’s current investor presentation earlier than its earnings launch and its 1Q2022 monetary outcomes gives perception into the corporate’s efficiency and potential.

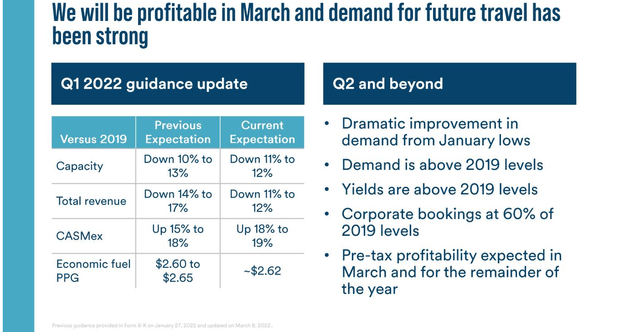

ALK 2Q2022 steerage (Alaska Airways investor presentation)

Strategic Stability

The strongest attribute that Alaska Airways has at this level is that it’s steady and is perfecting its methods at the same time as different airways proceed to attempt to discover their optimum post-covid methods. ALK’s dedication to its strategic plans has been refined by its December 2018 merger/acquisition of Virgin America, Richard Branson’s stylish low-cost home airline that was decided to enhance the standard of air journey. The Virgin America merger by no means produced the outcomes that Alaska at the very least publicly acknowledged would happen. Alaska gained a bidding battle with JetBlue (JBLU) to amass Virgin America and lots of conjectured that Alaska was extra inquisitive about defending its place on the west coast from an east coast interloper than in constructing on the community that Virgin America had constructed. In actuality, JetBlue was extra carefully aligned from a product standpoint with Virgin America than Alaska, which nonetheless solely affords a standard home first-class cabin. Quickly after ALK acquired Virgin America, it started to transform the recliner premium cabins on Virgin America’s A319s and A320s to straightforward home first-class cabins. DOT knowledge confirmed that Alaska rapidly moved to the place of getting the bottom fares within the transcontinental markets the place Virgin America beforehand operated, primarily from Los Angeles and San Francisco to main east coast markets. Premium cabins matter on coast-to-coast routes however ALK determined the operational complexity of getting a subfleet devoted to these routes was not price it. Alaska used the Covid pandemic to complete the termination of most of the remaining Los Angeles to east coast markets it took over as a part of the merger, with the variety of San Francisco markets dramatically lowered. Though Alaska has by no means stated how a lot they misplaced on the transcontinental markets, it’s sure it was a major quantity and contributed to ALK’s monetary underperformance that lasted for a number of years even earlier than the Covid pandemic started.

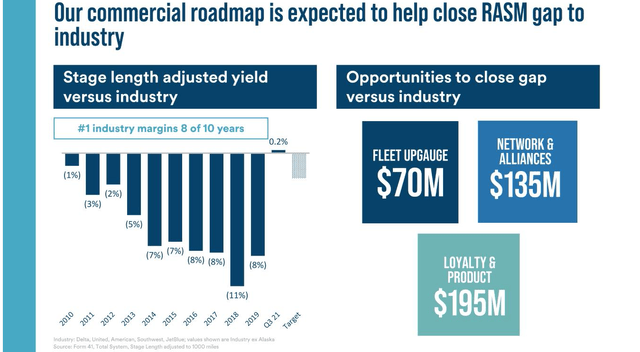

ALK’s margin & RASM (unit income) hole (ALK investor presentation)

Alaska’s strategic stability comes as a result of it has moved previous the Virgin America merger which didn’t do a lot to diversify its community past the Pacific Northwest the place the corporate has lengthy been closely concentrated – but additionally the place it obtains its earnings. California has lengthy been a extremely aggressive market and various a lot bigger airways have struggled to develop their networks on account of acquisitions of airways with a powerful California presence; it actually isn’t a shock that ALK has confronted the identical destiny. Maybe the most effective factor that may be stated in regards to the Virgin America acquisition from the angle of ALK shareholders is that it’s behind the corporate.

The power of Alaska Airways, particularly proper now, is that it has a confirmed, financially viable technique in an {industry} that’s nonetheless very a lot within the means of recovering from the Covid pandemic and the next discount in demand. ALK’s main power is its dominance of the Pacific Northwest together with site visitors to/from and inside the State of Alaska. Regardless of journey modifications within the tech {industry} on account of the pandemic and the shift to distant work, Seattle is benefitting from migration of Californians to the Pacific Northwest and the higher mountain states the place ALK has a powerful presence. Alaska Airways’ main power in each Portland and Seattle is that each have solely a single industrial airport and neither airport has a major quantity of progress capability both as a consequence of bodily restraints on the airport itself or out there these airports assist, leading to pretty sturdy pricing energy for ALK relative to different metro areas. The draw back is that ALK’s power within the PNW signifies that it has to attach practically the entire passengers it carries by itself tools over Seattle and Portland, resulting in circuitous or out-of-the-way connections in some markets. Nevertheless, the Pacific Northwest is “on the way in which” to some main U.S. markets, together with from a lot of the continental U.S. to Alaska the place ALK gives practically the entire giant jet companies inside the state, once more leading to sturdy pricing energy.

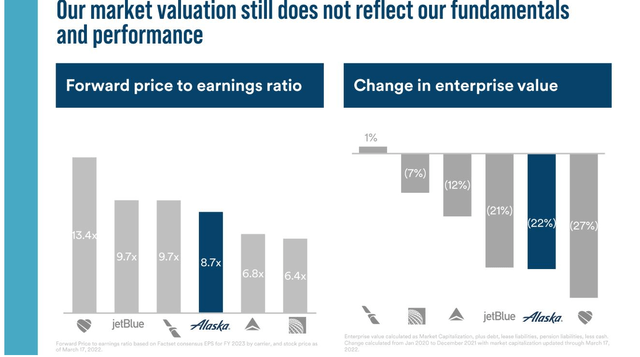

ALK vs. {industry} valuation (ALK investor presentation)

ALK’s best strategic profit proper now’s that it doesn’t must be engaged in a merger even because the middle-tier of the airline {industry} contemplates the acquisition of ultra-low-cost provider Spirit Airways (SAVE) with both ultra-low-cost provider Frontier which initiated a cope with Spirit, or New York Metropolis-based JetBlue. Not one of the three carriers is especially sturdy within the PNW so the direct impression to ALK will likely be minimal though lowered capability and a extra consolidated {industry} will definitely result in greater fares on a nationwide foundation; greater fares will likely be a certainty given the probability of upper labor and gasoline prices that may persist for years, limiting the power of the {industry} to supply the deeply discounted fares that stimulated a lot site visitors pre-Covid. As a result of ALK is a low-cost provider with unit prices which might be effectively beneath the massive 4 (American (AAL), Delta (DAL), Southwest (LUV), and United (UAL)), it would compete efficiently for a few of the site visitors that in any other case can be carried on the consolidated carriers, even when that site visitors is perhaps at greater fares than ALK beforehand carried. ALK’s 1Q2022 CASM-ex (unit prices excluding gasoline and specials) was 10.61 cents/obtainable seat mile in comparison with AAL’s 13.38 and DAL’s 13.24.

Countering its focus within the PNW, Alaska Airways has chosen to hitch the Oneworld alliance, which is led within the U.S. by American Airways. American has struggled to construct itself within the Northern California and PNW markets and dismantled a lot of its long-haul worldwide flying at Los Angeles (LAX). Whereas ALK is the fifth largest airline at LAX, AAL and ALK do provide synergies on the nation’s largest airport as outlined by the worth of the native market, notably up and down the west coast. Though ALK companions with practically each worldwide airline at Seattle apart from Delta, the partnership with Oneworld raises ALK’s profile globally, permitting ALK to supply and obtain deeper advantages that come from being part of an airline alliance. ALK can also use AAL’s community to distribute passengers all through the jap a part of the U.S. the place Alaska is competitively weaker. Certainly, a part of ALK’s progress plan is to extend its presence in transcontinental markets. Whereas ALK is just not prone to attempt to reinstate markets comparable to LAX to main airports within the NE U.S., it is rather attainable that they may add extra flights to AAL hubs to extend their competitiveness from a schedule standpoint. With a worthwhile and outlined community and progress technique, ALK is in an enviably steady place.

ALK progress alternatives by area (ALK investor presentation)

Aggressive rationality

In an {industry} that’s typically destructively aggressive, Alaska Airways is lucky to have rational rivals in its largest markets. ALK’s most direct competitor is Delta Air Strains which is the twond largest airline at Seattle due to its personal Pacific Northwest (PNW) hub and in addition the 2nd largest airline in Alaska. DAL and former merger associate Northwest Airways had relationships with ALK, and DAL sought to deepen that relationship as Delta started planning ten years in the past to restructure its Pacific community, shifting from a hub in Tokyo to at least one within the PNW. DAL had beforehand operated a small Asia hub at Portland so knew it needed to be within the bigger Seattle market and construct a bigger hub to ensure that the Asia flights to achieve success. DAL reportedly requested ALK to be its unique worldwide associate from Seattle partly as a result of DAL purportedly couldn’t get sufficient seats on ALK flights beneath the partnership on the time to fill DAL’s Asia flights. ALK selected to not develop an unique partnership and DAL started to construct its personal hub at Seattle which now has roughly half of the flights than ALK has however is extra international in nature (though a lot of DAL’s Asia flights haven’t returned to regular schedules even when its Europe flights have) and in addition stronger within the jap U.S. pre-Covid, DAL acquired about 70% of the native Seattle market income that ALK acquired, indicating each the longer common passenger lengths from Seattle, Delta’s system income premiums to the {industry}, and the truth that DAL doesn’t want to hold as a lot lower-yielding connecting site visitors by way of Seattle because it has different hubs together with Salt Lake Metropolis which might be extra environment friendly in serving that objective. DAL is vying with American for the title of the biggest airline at LAX by income and can be the twond largest provider to/from the state of Alaska, once more benefitting from its hubs within the Midwest and Japanese U.S.

Southwest Airways has given up vital share – together with United – as Delta expanded within the Seattle market however LUV stays the biggest airline for site visitors inside California, together with within the large Bay to Basin market which ALK hoped to penetrate with the Virgin America merger. Whereas ALK is the dominant airline from California to the PNW, LUV is a major challenger from the PNW to main markets within the west comparable to Las Vegas, Phoenix, and Denver in addition to to secondary California cities, together with San Jose and Oakland. LUV has additionally aggressively expanded its presence from the western U.S. to Hawaii, stepping on ALK’s toes because the Texas-based airline makes an attempt to achieve share. LUV doesn’t serve the state of Alaska and may not, given the very completely different operational dynamics in contrast with a lot of the remainder of the U.S. however, ought to LUV select so as to add service to The Final Frontier, there may very well be vital monetary implications to the state’s namesake airline.

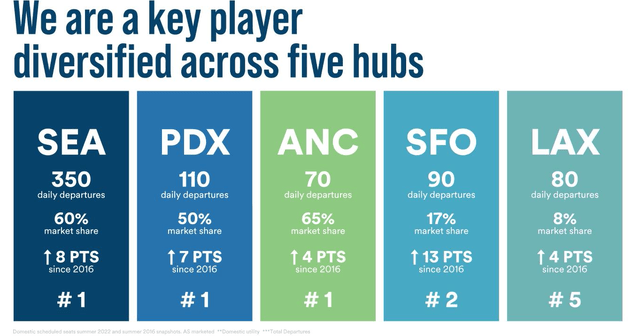

Alaska Airways hubs (ALK investor presentation)

Whereas Delta is concentrated on having a presence in main ALK-competitive markets, Southwest seems extra intent in not permitting its market share to be eroded in its remaining markets to/from the PNW even because it grows to/from Hawaii. Each rivals be part of ALK on the record of the best-run airways within the U.S. with all three main the {industry}’s monetary restoration post-Covid. All three even have higher than common steadiness sheets for his or her segments of the {industry}. Alaska, Delta, and Southwest are all intensely aggressive together with with one another, however all of them know when competitors turns into harmful and when it’s time to concentrate on methods that don’t hurt themselves. Whereas the {industry} stays extremely aggressive, a part of ALK’s structural benefit is that it competes with airways that financially carry out on the high of the {industry} each doing solely what is smart financially for them to do and in addition by refraining from what is going to hurt itself even when one other airline will undergo extra.

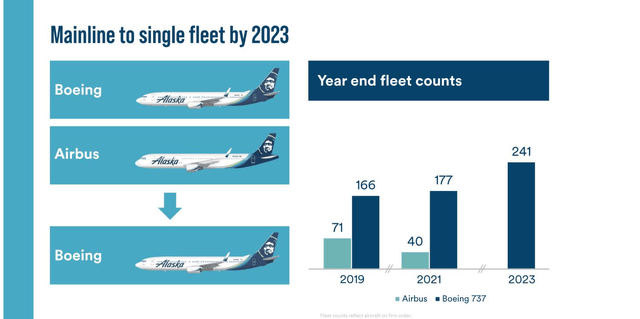

ALK’s mainline fleet transition (ALK investor presentation)

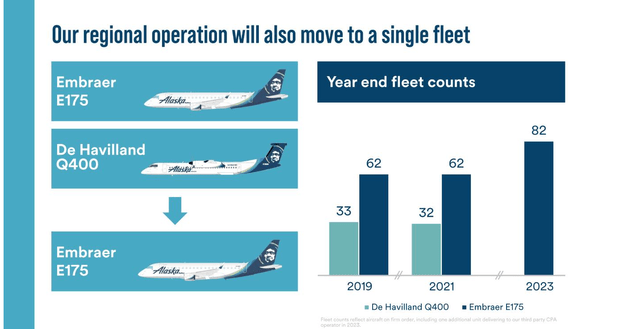

ALK’s regional plane fleet transition (ALK investor presentation)

Monetary Power

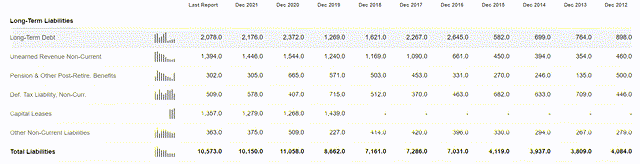

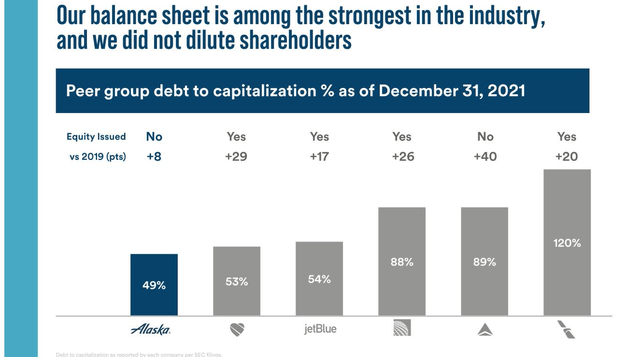

ALK’s best power is that of its funds. The corporate has lengthy been financially conservative with low debt ranges, has been on the high-end of the {industry} in profitability, and has not diluted its shareholders through the pandemic. ALK’s debt ranges are notable in that it has much less long-term debt now than it had instantly after its merger with Virgin America. Only a few US airways are beneath their pre-pandemic debt ranges but though most are starting to chip away on the debt they accrued through the pandemic.

ALK long-term liabilities (Looking for Alpha)

ALK vs {industry} debt to cap (ALK investor presentation)

As well as, ALK has a protracted observe file of producing double-digit web revenue margins, one thing it expects to have the ability to do later this yr. Of the airways which have reported to this point, Delta has stated that it expects to have the ability to obtain that purpose and Southwest is prone to as effectively.

ALK 10-year web revenue margins (Looking for Alpha)

Lastly, Alaska is likely one of the few U.S. airways that didn’t situation inventory through the pandemic with the intention to permit stockholders to completely take part within the upside the corporate experiences this yr. (DAL additionally didn’t situation shares through the pandemic).

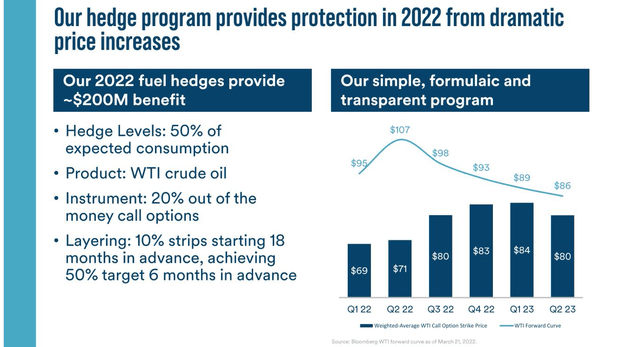

Along with its sound fundamentals, Alaska is likely one of the few airways that has a gasoline hedging technique in place, which lowered the corporate’s gasoline invoice by as a lot as 10% in comparison with different airways within the first quarter. Jet gasoline is historically costlier within the Pacific Northwest and different main ALK markets than the nationwide common, so Alaska’s capability to pay lower than its rivals with broad nationwide networks is critical. Within the 2nd quarter of 2022, ALK’s gasoline hedging is anticipated to yield an analogous value as DAL which has the good thing about a refinery which is producing advantages vs. unhedged carriers, and DAL is extra closely concentrated in components of the nation with decrease gasoline prices. Southwest is prone to report even bigger advantages from its hedging program than both ALK or DAL however the truth that ALK has a functioning gasoline price discount technique will likely be one of many key components in aiding its monetary restoration.

ALK gasoline hedging (ALK investor presentation)

ALK has laid out sound methods to cut back its prices together with by accelerating its retirement of Airbus A320 household plane in favor of an all Boeing 737 fleet, together with the biggest variations of the 737 MAX household. As well as, ALK is poised to shift to an all-Embraer E-Jet regional airliner fleet, ensuing within the retirement of its giant turboprop plane. As with many airways, ALK is growing the gauge (common plane measurement) of its fleet and can achieve advantages each from the bigger plane and from much less complexity of its fleet.

Alaska does face a number of vital challenges – however maybe not more than different airways. ALK has lengthy had decrease labor prices partly as a result of it pays lower than different airways for comparable positions. Airways all through the U.S. are aggressively hiring however the greatest airways look like finest positioned to persuade pilot candidates to work for them; the prospect of upper paying widebody worldwide flying is a draw that the massive 3 (AAL, DAL, and UAL) have which different carriers can’t match.

As a result of ALK has discovered itself quick staffing, leading to occasional operational shortfalls, the corporate has determined to cut back capability as much as 4% into the summer time. Staffing shortages are requiring airways together with ALK to jettison their least worthwhile routes. Not solely are staffing shortages lowering capability in a high-demand surroundings, which is for certain to spice up yields, but additionally is resulting in a culling of much less worthwhile routes. ALK is prone to profit from the very staffing shortages that it’s being pressured to handle.

Conclusion

All airways are reporting sturdy demand developments which can result in a return to profitability for many if not the entire {industry} by the second quarter. Due to sharpening its strategic focus through the pandemic, Alaska Airways may effectively retake its place as one of many U.S. airline {industry}’s most worthwhile gamers as a consequence of its strategic stability, favorable aggressive surroundings, and robust underlying funds.