News

Xi Jinping’s third term is a tragic error

Xi Jinping will shortly be confirmed for a 3rd time period as common secretary of the Communist occasion and head of the navy. So, is his achievement of such unchallengeable energy good for China or for the world? No. It’s harmful for each. It might be harmful even when he had confirmed himself a ruler of matchless competence. However he has not accomplished so. As it’s, the dangers are these of ossification at house and rising friction overseas.

Ten years is all the time sufficient. Even a first-rate chief decays after that lengthy in workplace. One with unchallengeable energy tends to decay extra rapidly. Surrounded by individuals he has chosen and protecting of the legacy he has created, the despot will turn into more and more remoted and defensive, even paranoid.

Reform halts. Choice-making slows. Silly selections go unchallenged and so stay unchanged. The zero-Covid coverage is an instance. If one needs to look exterior China, one can see the insanity induced by extended energy in Putin’s Russia. In Mao Zedong, China has its personal instance. Certainly, Mao was why Deng Xiaoping, a genius of frequent sense, launched the system of time period limits Xi is now overthrowing.

The benefit of democracies shouldn’t be that they essentially select clever and well-intentioned leaders. Too usually they select the other. However these may be opposed with out hazard and dismissed with out bloodshed. In private despotisms, neither is feasible. In institutionalised despotisms, dismissal is conceivable, as Khrushchev found. However it’s harmful and the extra dominant the chief, the extra harmful it turns into. It’s merely lifelike to anticipate the following 10 years of Xi to be worse than the final.

How dangerous then was his first decade?

In a latest article in China Management Monitor, Minxin Pei of Claremont McKenna Faculty judges that Xi has three primary targets: private dominance; revitalisation of the Leninist party-state; and increasing China’s international affect. He has been triumphant on the primary; formally profitable on the second; and had combined success on the final. Whereas China is at present a recognised superpower, it has additionally mobilised a robust coalition of anxious adversaries.

Pei doesn’t embrace financial reform amongst Xi’s principal aims. The proof suggests that is fairly appropriate. It’s not. Notably, reforms that would undermine state-owned enterprises have been averted. Stricter controls have additionally been imposed on well-known Chinese language businessmen, corresponding to Jack Ma.

Above all, deep macroeconomic, microeconomic and environmental difficulties stay largely unaddressed.

All three have been summed up in former premier Wen Jiabao’s description of the financial system as “unstable, unbalanced, uncoordinated and unsustainable”.

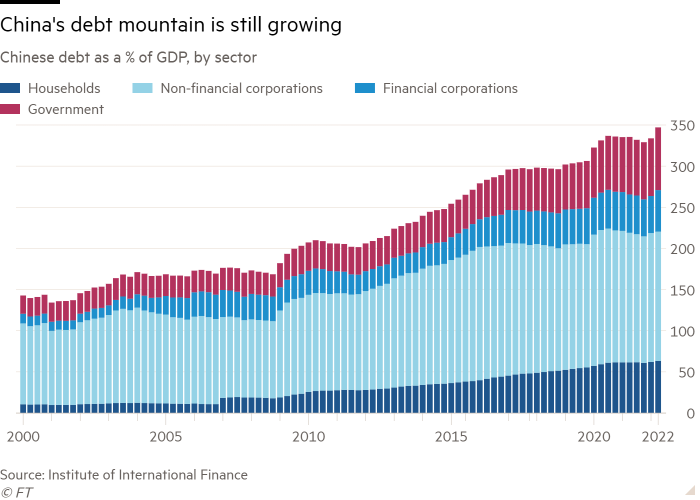

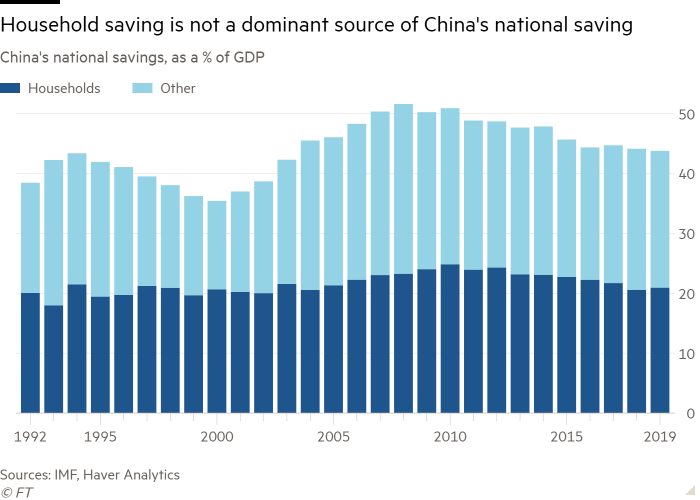

The basic macroeconomic issues are extra financial savings, its concomitant, extra funding, and its corollary, rising mountains of unproductive debt. These three issues go collectively: one can’t be solved with out fixing the opposite two. Opposite to extensively shared perception, the surplus saving is barely partly the results of an absence of a social security internet and consequent excessive family financial savings. It’s as a lot as a result of family disposable revenue is such a low share of nationwide revenue, with a lot of the remainder consisting of earnings.

The result’s that nationwide financial savings and funding are each above 40 per cent of gross home product. If the funding weren’t that top, the financial system could be in a everlasting hunch. However, as development potential has slowed, a lot of this funding has been in unproductive, debt-financed development. That may be a short-term treatment with the opposed long-term unintended effects of dangerous debt and falling return on funding. The answer shouldn’t be solely to cut back family financial savings, however elevate the family share in disposable incomes. Each threaten highly effective vested pursuits and haven’t occurred.

The basic microeconomic issues have been pervasive corruption, arbitrary intervention in personal enterprise and waste within the public sector. As well as, environmental coverage, not least the nation’s big emissions of carbon dioxide, stays an unlimited problem. To his credit score, Xi has recognised this challenge.

Extra just lately, Xi has adopted the coverage of maintaining at bay a virus circulating freely in the remainder of the world. China ought to as an alternative have imported one of the best international vaccines and, after they have been administered, reopened the nation. This could have been smart and likewise indicated continued perception in openness and co-operation.

Xi’s programme of renewed central management isn’t a surprise. It was a pure response to the eroding impression of better freedoms on a political construction that rests on energy that’s unaccountable, besides upwards. Pervasive corruption was the inevitable consequence. However the worth of making an attempt to suppress it’s threat aversion and ossification. It’s exhausting to consider {that a} top-down organisation below one man’s absolute management can rule an ever extra refined society of 1.4bn individuals sanely, not to mention successfully.

It’s not shocking both that China has turn into more and more assertive. Western unwillingness to regulate to China’s rise is clearly part of the issue. However so has been China’s open hostility to core values the west (and plenty of others) maintain expensive. Many people can not take significantly China’s adherence to the Marxist political beliefs which have demonstrably not succeeded in the long term. Sure, Deng’s sensible eclecticism did work, no less than whereas China was a creating nation. However reimposition of the outdated Leninist orthodoxies on at present’s extremely advanced China should be a useless finish at greatest. At worst, as Xi stays indefinitely in workplace, it may show one thing much more harmful than that, for China itself and the remainder of the world.

martin.wolf@ft.com

Comply with Martin Wolf with myFT and on Twitter