Crypto

Avalanche: More Pain Ahead? (Cryptocurrency:AVAX-USD)

bin kontan

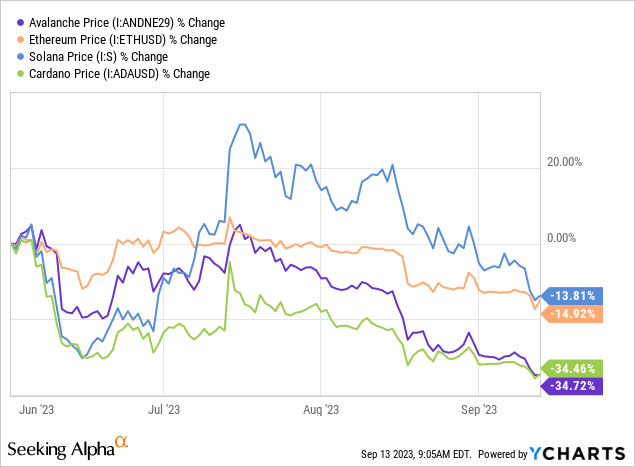

When I last covered the Avalanche (AVAX-USD) blockchain in early June, I gave the native coin of the network a “bullish” call and noted what I viewed as a divergence between the AVAX price and the blockchain’s usage. Since that article, it’s been essentially nothing but pain for AVAX holders as the coin has declined by roughly 35% and has lagged notable smart contract network peers like Ethereum (ETH-USD) and Solana (SOL-USD):

My frustrations with the coin’s performance aside, I think it’s important to re-examine many of the factors that ultimately led me to go long AVAX in the first place to see if those setups still warrant a bullish position.

Network Activity

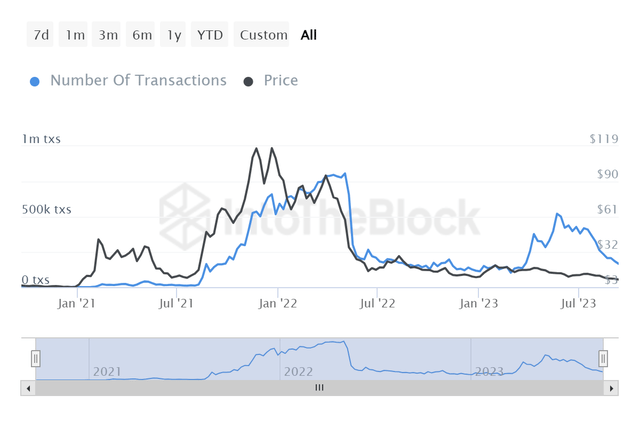

Back in June, I looked at daily transactions, daily active users, and NFT sales. Each of which were surging through April and May. That is no longer the case as we move through September.

IntoTheBlock

After topping out at over 500k transactions back in late May, it has been a slow decline back to trend for Avalanche transactions in the subsequent months. More importantly though, the surge in chain usage never impacted the AVAX price the way it did back in late 2021 and early 2022.

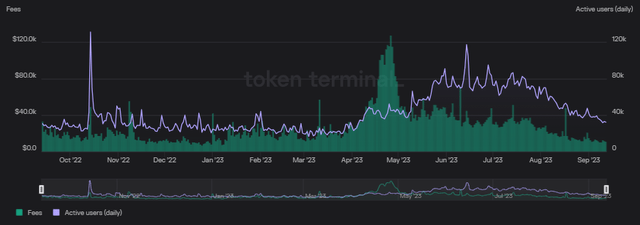

Avalanche DAUs (Token Terminal)

Daily active users on the network have fallen about 75% from the mid-June peak of 117k to the more recent level of 31-35k. When smoothing the figure out to a monthly average for DAUs, at 36k, so far September is the third consecutive monthly decline from 78k in June. As one might imagine, a large part of this decline in usage appears to be due to the declines in NFT activity on the network.

Month

Sales (USD)

Unique Sellers

Unique Buyers

Total Txns Avg Sale (USD)

September 2023

$75,171.39

1,546

4,926 12,003

$6.26

August 2023

$353,144.99

5,209 14,263

46,583

$7.58

July 2023

$461,909.51 16,789

19,159

81,675

$5.66

June 2023 $593,548.85

16,409

11,875

63,899

$9.29 May 2023

$774,626.36

11,089

5,888

35,685 $21.71

April 2023

$1,082,286.65

2,942

5,764 30,104

$35.95

Source: CryptoSlam

There were over $1 million in USD-denominated NFT sales on Avalanche in April and the average sale price of those NFTs was over $35 per item. Fast-forward to August and the average price of NFT sales fell below $8. On one hand, this is an indication that Avalanche can indeed be used for lower-value transactions. Which is something Ethereum has yet to be able to do on the main layer to this point. However, the argument could also be made that even with more buyers, sellers, and NFT transactions in August versus April, AVAX holders haven’t benefited from the increase in NFT-market headcount.

Valuation

One of the other things that I considered back in my June article was chain valuation. While I’ll concede that all of these networks have egregious P/S valuations if we’re comparing them to traditional equities, the “crypto P/S” valuation story on Avalanche had been improving earlier this summer. That is no longer the case.

Avalanche P/S Ratio (Token Terminal)

There are two different ways to measure the price-to-sales ratio of a smart contract blockchain network. We can look at the P/S ratio vs. the fully diluted coin supply or vs. the circulating coin supply. For the sake of simplicity, I’ve put both of those ratios in the chart above. Each of them have been gradually increasing over the last 4 months. The monthly average fully diluted P/S ratio was 483 in May. The monthly average circulating P/S ratio was 224. As of the article submission, those figures are currently 1,169 and 573 for the month of September. For a comparison, Ethereum trades at a fully diluted P/S ratio of 144 while Polygon (MATIC-USD) trades at 474.

Development

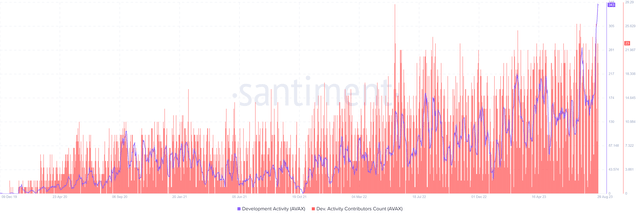

It isn’t all terrible news for Avalanche, however. Over the last several years, Avalanche has seen steady growth in development activity.

Avalanche Development (Santiment)

Santiment’s contributor count shows growth from a weekly average of 23 in August 2021 to 35 last August. That average grew slightly to 37 in August 2023. But the overall trend in both raw contributors and development activity is positive.

Risks

Aside from the decline in broad network usage and the valuation problems, there are other risks to consider as well. Avalanche has seen an absolutely enormous 95% decline in TVL from $11.6 billion in late 2021 to under $500 million currently:

Avalanche TVL (DeFiLlama)

The market capitalization of stablecoins on the network has also fallen from a high of $4.5 billion down to $1.2 billion. This is by no means a problem that is exclusive to just Avalanche but as I see it the decline in DeFi footprint on Avalanche is having an impact on the demand for AVAX. As interest rates rise, the incentive to buy bonds directly rather than playing in the DeFi markets becomes more apparent.

AVAX Holder Concentration (IntoTheBlock)

Furthermore, the retail holder base of AVAX is small compared to other smart contract blockchains like Ethereum or Cardano (ADA-USD). The IntoTheBlock chart above shows 47% of AVAX is held by whales and 31% is held by what IntoTheBlock considers to be investors. That means retail holds just 22%. I think it could be reasonably argued that AVAX is functioning more as a pure speculative asset than as a utility coin used to pay gas for network activity.

Summary

While I’m downgrading AVAX today from a “buy” to a “hold,” I haven’t thrown in the towel on this network entirely. I still think there are interesting opportunities in the crypto market and Avalanche as a network continues to be one of those ideas. It’s a fast chain that has integrations with many of the top protocols in the DeFi ecosystem. It serves a market that Ethereum requires secondary layers to serve at this current time. I’m not out of AVAX entirely, but I have trimmed my position on this adoption weakness and will reassess the idea again in the months to come.